We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Gilts Understanding

Comments

-

Yes that's right. Because there are generally a few providers vying for the best savings rate, you can usually spread money without losing out on much interest.SavingStudent1 said:

Oh yes, thank you! So, made up scenario: suppose I had 4 different banks that give me 2% interest on a 5-years fixed rate savings account, if I had £307,948.44 (= £76987.11 * 4), then could I now invest £76987.11 into 4 separate accounts so that at the end of the 5 years, I earn £85,000 from each of them?masonic said:

Yes, you understand correctly, keep the balance under the limit at all times. You can spread your money around (unconnected) savings providers to avoid going over the limit. It would be unusual for someone to need to hold that sort of money in cash over the long term (sometimes it is necessary to do so temporarily).SavingStudent1 said:

Thank you! So, for example, is that the money in the savings account or the amount you initially invested? For example, it seems like the compensation limit is £85,000.masonic said:

Check they have FSCS protection, if so your money is just as safe as if held anywhere else provided you stay below the compensation limit.SavingStudent1 said:Yes, I think you are right - I am just worried sometimes because most of the banks that offer the best deal are ones I have never heard off, like high-street banks as HSBC, NatWest, Santander etc.. and I am just worried about that. I don't really know much about reliability and banks in general, so I only deal with the well-known ones lol.

So, do I sort of need to ensure that I invest £85,000 or the maximum in my account at any time is £85,000 to ensure I get fully compensated?

So, for example, if the interest rate is 2% based on MSE website with JN Bank - it says on the website, 2.00% gross AERⱡ fixed, if I invested: £76987.11, then after 5 years, I'll have: £76987.11 * 1.02^5 = £85,000 and so at any time if it defaults, I should get fully compensated?

I assume this is what you meant by spreading your money around providers - obviously not necessarily going to the limit each time, but I just did so in my example.

0 -

There are plenty of experienced investors on this site , many with pensions/investments worth a lot .SavingStudent1 said:

Thanks, that really helps and makes sense. Cheers for the website too, just saw 2 gilts were issued today!Linton said:

You cannot buy a gilt on release at its face value except by chance as these days all gilts are auctioned. You as a small retail customer really are limited to the secondary market buying them through your investment platform from people who want to sell. https://www.dmo.gov.uk/data/pdfdatareport?reportCode=D2.1E ( a really clunky website) gives a list of all bonds issued. So far I have yet to find any issued over the past 3 months on HL's list of bonds available. I guess that many bonds are taken by the institutions and dont reach the market,SavingStudent1 said:

Thank you, I am a beginner so I don't know much of what all these things mean, but I am planning to read and learn on it allmasonic said:Aretnap has done the maths for you. The reason most people hold gilts is as a diversifier. For that purpose a fund is more convenient. The aim is have some inverse correlation with equities and to rebalance from one to the other so as to buy low and sell high in general. That was a good proposition when bonds returned ~ inflation + 1%, today not so much. Buying and holding gilts to maturity will be almost guaranteed to return less than a fixed term consumer savings account.") .

.

Yes, I just realised this to be honest when I understood the calculations thanks to Aretnap and done it on larger values.

So, can I ask: How do we know when a government releases a new gilt e.g. if they release it today at face value HM Treasury 1.5% Sept 2035, - made it up, but how would I know that it has been released? Do I just have to keep up with the news or follow a certain page? Because I assume then I can buy it at face value £100 and the savings would be a bit better I suppose?

But yes, with low moneys, a fixed term consumer savings account earns so much more!!

Sadly as far as I can see directly buying individual gilts to meet your needs is difficult and I believe the whole area is best left to the professionals. Bond index funds will hold many different bonds with a range of maturity dates which really does not make much sense to me unless you just want to hold bonds in general as padding for your risky equity investments.

Yes, I will probably look into bonds in the future then when I start to invest properly and want to diversify my portfolio, but now I am understanding what is best for my current situation and what is not, thanks to all of you!

Probably hardly any of them invest in individual gilts as far as I know . That probably tells you that you are going down the wrong track. New investors are best to look at simple things like multi asset funds or index trackers rather than individual shares/gilts/bonds.

Regarding the savings banks . You should not be scared to venture from the high st . It is possible the customer service of some of the very new banks with the very highest rates , might be a bit poor sometimes . However even some more familiar names like Coventry/Leeds/Skipton building society often have good rates on offer .

Also on this forum, often mentioned are Ford Money; Aldermore; Charter; Shawbrook; Paragon. All offer a reliable service.1 -

Thanks, that is great. By the way, I remember reading a thread where it is not so good to keep changing banks, but is it okay to: stick with your main bank e.g. for me Nationwide, and then opening several bank accounts like the above to take advantage of these best savings rate. This will not affect my credit score and future applications for mortgages etc. with banks right?masonic said:

Yes that's right. Because there are generally a few providers vying for the best savings rate, you can usually spread money without losing out on much interest.SavingStudent1 said:

Oh yes, thank you! So, made up scenario: suppose I had 4 different banks that give me 2% interest on a 5-years fixed rate savings account, if I had £307,948.44 (= £76987.11 * 4), then could I now invest £76987.11 into 4 separate accounts so that at the end of the 5 years, I earn £85,000 from each of them?masonic said:

Yes, you understand correctly, keep the balance under the limit at all times. You can spread your money around (unconnected) savings providers to avoid going over the limit. It would be unusual for someone to need to hold that sort of money in cash over the long term (sometimes it is necessary to do so temporarily).SavingStudent1 said:

Thank you! So, for example, is that the money in the savings account or the amount you initially invested? For example, it seems like the compensation limit is £85,000.masonic said:

Check they have FSCS protection, if so your money is just as safe as if held anywhere else provided you stay below the compensation limit.SavingStudent1 said:Yes, I think you are right - I am just worried sometimes because most of the banks that offer the best deal are ones I have never heard off, like high-street banks as HSBC, NatWest, Santander etc.. and I am just worried about that. I don't really know much about reliability and banks in general, so I only deal with the well-known ones lol.

So, do I sort of need to ensure that I invest £85,000 or the maximum in my account at any time is £85,000 to ensure I get fully compensated?

So, for example, if the interest rate is 2% based on MSE website with JN Bank - it says on the website, 2.00% gross AERⱡ fixed, if I invested: £76987.11, then after 5 years, I'll have: £76987.11 * 1.02^5 = £85,000 and so at any time if it defaults, I should get fully compensated?

I assume this is what you meant by spreading your money around providers - obviously not necessarily going to the limit each time, but I just did so in my example.0 -

Thanks, that is really useful! I haven't actually researched multi-asset funds or index trackers, so I will look into them :). There are so many products and services as investment tools lol, it really overwhelms me sometimes!Albermarle said:

There are plenty of experienced investors on this site , many with pensions/investments worth a lot .SavingStudent1 said:

Thanks, that really helps and makes sense. Cheers for the website too, just saw 2 gilts were issued today!Linton said:

You cannot buy a gilt on release at its face value except by chance as these days all gilts are auctioned. You as a small retail customer really are limited to the secondary market buying them through your investment platform from people who want to sell. https://www.dmo.gov.uk/data/pdfdatareport?reportCode=D2.1E ( a really clunky website) gives a list of all bonds issued. So far I have yet to find any issued over the past 3 months on HL's list of bonds available. I guess that many bonds are taken by the institutions and dont reach the market,SavingStudent1 said:

Thank you, I am a beginner so I don't know much of what all these things mean, but I am planning to read and learn on it allmasonic said:Aretnap has done the maths for you. The reason most people hold gilts is as a diversifier. For that purpose a fund is more convenient. The aim is have some inverse correlation with equities and to rebalance from one to the other so as to buy low and sell high in general. That was a good proposition when bonds returned ~ inflation + 1%, today not so much. Buying and holding gilts to maturity will be almost guaranteed to return less than a fixed term consumer savings account..

Yes, I just realised this to be honest when I understood the calculations thanks to Aretnap and done it on larger values.

So, can I ask: How do we know when a government releases a new gilt e.g. if they release it today at face value HM Treasury 1.5% Sept 2035, - made it up, but how would I know that it has been released? Do I just have to keep up with the news or follow a certain page? Because I assume then I can buy it at face value £100 and the savings would be a bit better I suppose?

But yes, with low moneys, a fixed term consumer savings account earns so much more!!

Sadly as far as I can see directly buying individual gilts to meet your needs is difficult and I believe the whole area is best left to the professionals. Bond index funds will hold many different bonds with a range of maturity dates which really does not make much sense to me unless you just want to hold bonds in general as padding for your risky equity investments.

Yes, I will probably look into bonds in the future then when I start to invest properly and want to diversify my portfolio, but now I am understanding what is best for my current situation and what is not, thanks to all of you!

Probably hardly any of them invest in individual gilts as far as I know . That probably tells you that you are going down the wrong track. New investors are best to look at simple things like multi asset funds or index trackers rather than individual shares/gilts/bonds.

Regarding the savings banks . You should not be scared to venture from the high st . It is possible the customer service of some of the very new banks with the very highest rates , might be a bit poor sometimes . However even some more familiar names like Coventry/Leeds/Skipton building society often have good rates on offer .

Also on this forum, often mentioned are Ford Money; Aldermore; Charter; Shawbrook; Paragon. All offer a reliable service.1 -

Passive investing Archives - Monevator

This is a good article and a good website generally.3 -

It is a good idea to have at least one long-term current account, even if you switch around for incentives and interest rates. Opening new savings accounts has zero impact on your credit file - they aren't even reported to credit reference agencies, and opening new current accounts (without an overdraft) has a minimal impact. It's loans and credit cards that will have a bigger impact, some lenders will refuse an application if you have any history of taking out payday loans, for example.SavingStudent1 said:

Thanks, that is great. By the way, I remember reading a thread where it is not so good to keep changing banks, but is it okay to: stick with your main bank e.g. for me Nationwide, and then opening several bank accounts like the above to take advantage of these best savings rate. This will not affect my credit score and future applications for mortgages etc. with banks right?masonic said:

Yes that's right. Because there are generally a few providers vying for the best savings rate, you can usually spread money without losing out on much interest.SavingStudent1 said:

Oh yes, thank you! So, made up scenario: suppose I had 4 different banks that give me 2% interest on a 5-years fixed rate savings account, if I had £307,948.44 (= £76987.11 * 4), then could I now invest £76987.11 into 4 separate accounts so that at the end of the 5 years, I earn £85,000 from each of them?masonic said:

Yes, you understand correctly, keep the balance under the limit at all times. You can spread your money around (unconnected) savings providers to avoid going over the limit. It would be unusual for someone to need to hold that sort of money in cash over the long term (sometimes it is necessary to do so temporarily).SavingStudent1 said:

Thank you! So, for example, is that the money in the savings account or the amount you initially invested? For example, it seems like the compensation limit is £85,000.masonic said:

Check they have FSCS protection, if so your money is just as safe as if held anywhere else provided you stay below the compensation limit.SavingStudent1 said:Yes, I think you are right - I am just worried sometimes because most of the banks that offer the best deal are ones I have never heard off, like high-street banks as HSBC, NatWest, Santander etc.. and I am just worried about that. I don't really know much about reliability and banks in general, so I only deal with the well-known ones lol.

So, do I sort of need to ensure that I invest £85,000 or the maximum in my account at any time is £85,000 to ensure I get fully compensated?

So, for example, if the interest rate is 2% based on MSE website with JN Bank - it says on the website, 2.00% gross AERⱡ fixed, if I invested: £76987.11, then after 5 years, I'll have: £76987.11 * 1.02^5 = £85,000 and so at any time if it defaults, I should get fully compensated?

I assume this is what you meant by spreading your money around providers - obviously not necessarily going to the limit each time, but I just did so in my example.

1 -

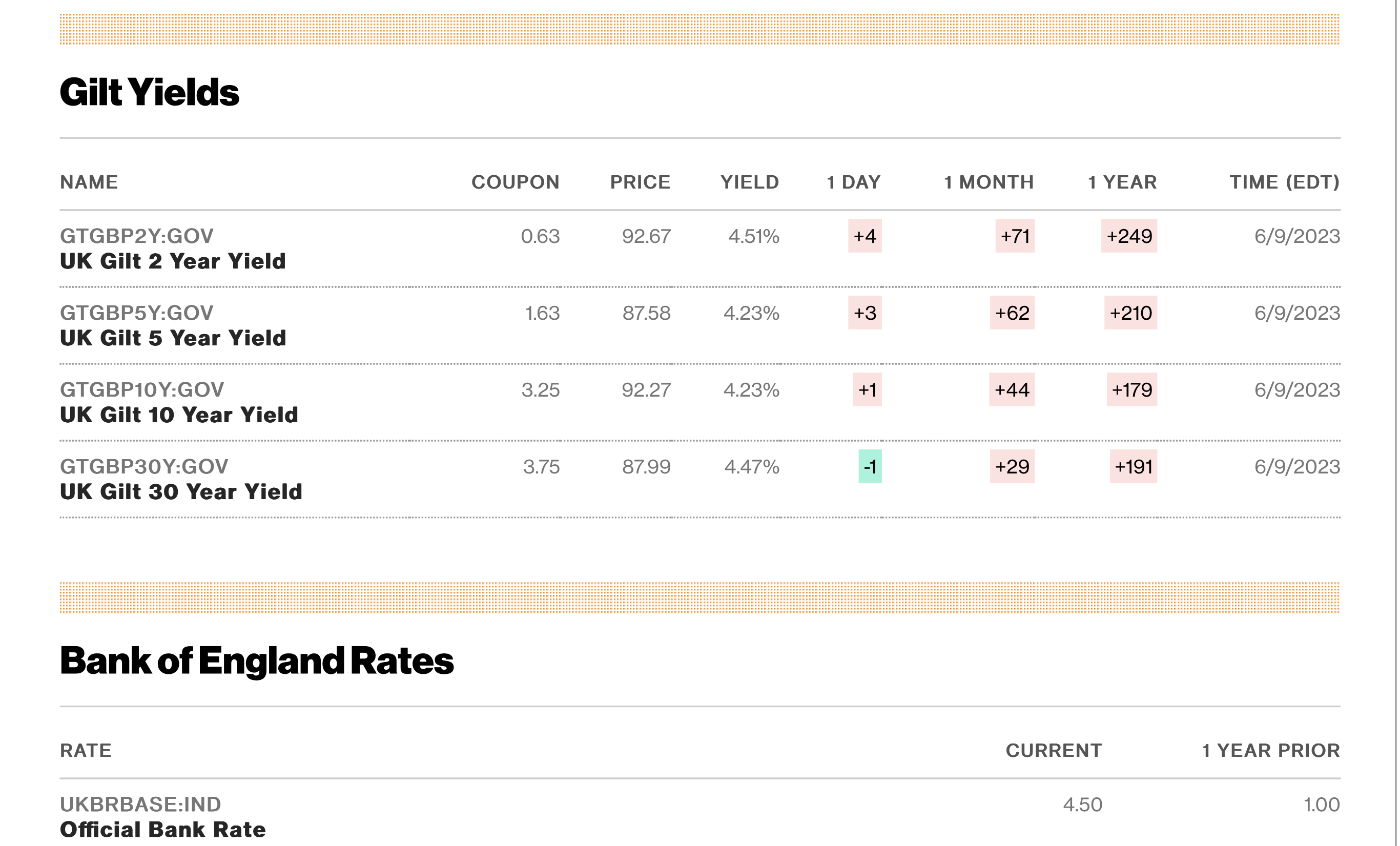

Very different world now. Gilt rates massively beat savings. UK retail investors can buy gilts via Computershare. Here are the fees:Aretnap said:

By contrast, if you put your money into the best available 5 year fixed rate savings account, you would get back a total of over £22000 over about the same time period. Why not do that instead?

So to buy £10k would cost £35 + £18.75 = £53.75. And to sell, eg £11k some time later would cost: £35 + £21 = £56. Total transaction cost = £109.75.

GB0002404191 is paying 6%. Top savings accounts (accepting unlimited amounts, no notice, FSCS protected) are paying ~3.5% tops. Savings charge zero fees, but gilts would still profit after < three months in this £10k example.

I knocked up a google sheet.

Not sure if gilt dividends are cumulative so I've included both calculations. At year five, gilts beat savings by £1,348 if cumulative and by £967 if not. But there's paperwork. Filling PDF forms is time-consuming and either emailing them to Computershare (identity security dodginess) or posting would be a pain. At least need to fill one to initially join the Approved Group, then at least one per buy and sell. Unclear whether need to fill interest form once, or every interest payment. Plus gilts are riskier than savings, price can fall. And gilts only pay interest bi-annually, not monthly like most savings accounts. Anyway, thoughts? Has anyone bought gilts through Computershare?

0 -

stone_circle said:Not sure if gilt dividends are cumulative so I've included both calculations. At year five, gilts beat savings by £1,348 if cumulative and by £967 if not. But there's paperwork. Filling PDF forms is time-consuming and either emailing them to Computershare (identity security dodginess) or posting would be a pain. Plus gilts are riskier than savings, price can fall. Anyway, thoughts?Gilt coupons are not accumulating. They will be paid into your trading account and you would need to do something with them in order to generate any compound return. Also, if held to maturity, which is advisable, there would be no cost to sell.

GB002404191, more commonly known as TR28, has a YTM of 4.29%, not the headline coupon of 6%. This is because you have to pay £108 per £100 face value. The price will trend towards £100 face value as it nears maturity, so a capital loss must be factored in. The trading costs you highlight are quite expensive when others charge a flat fee of £5-10. Doesn't look great compared to a 2 year fix of almost 5.5% available today risk free.Posting this in a thread from 2 years ago discussing a very different interest rate regime is a little disingenuous without mention of how much savings rates have improved, don't you think?4 -

"disingenuous" - I'm not following. Worth continuing existing thread for context IMO. I've said nothing disparaging of earlier posters.

Price of GB0002404191 is currently £108, I see. This changes the complexion, but still profitable after ~1 year vs savings.

"Gilt coupons are not accumulating." - This form I've just found allows reinvestment, but unclear whether the "Full Title of Stock to be purchased" box can be the gilt you own or if "Stock" means an equity instead (one already purchased thru Computershare?).

"others charge a flat fee of £5-10" - what others? I see HL allow purchasing gilts, but their annual fees prob add up to similar or more than Computershare. Any others you know of?

"held to maturity, which is advisable, there would be no cost to sell" - advisable to avoid transaction fee, or is there any other reason? Prob don't need to fill a sell PDF form too.0 -

Although their ex-coupon dates are referred to as ex-dividend dates, gilts pay interest. As Masonic writes, there are much better options than Computershare e.g., iWeb, AJ Bell, HL.

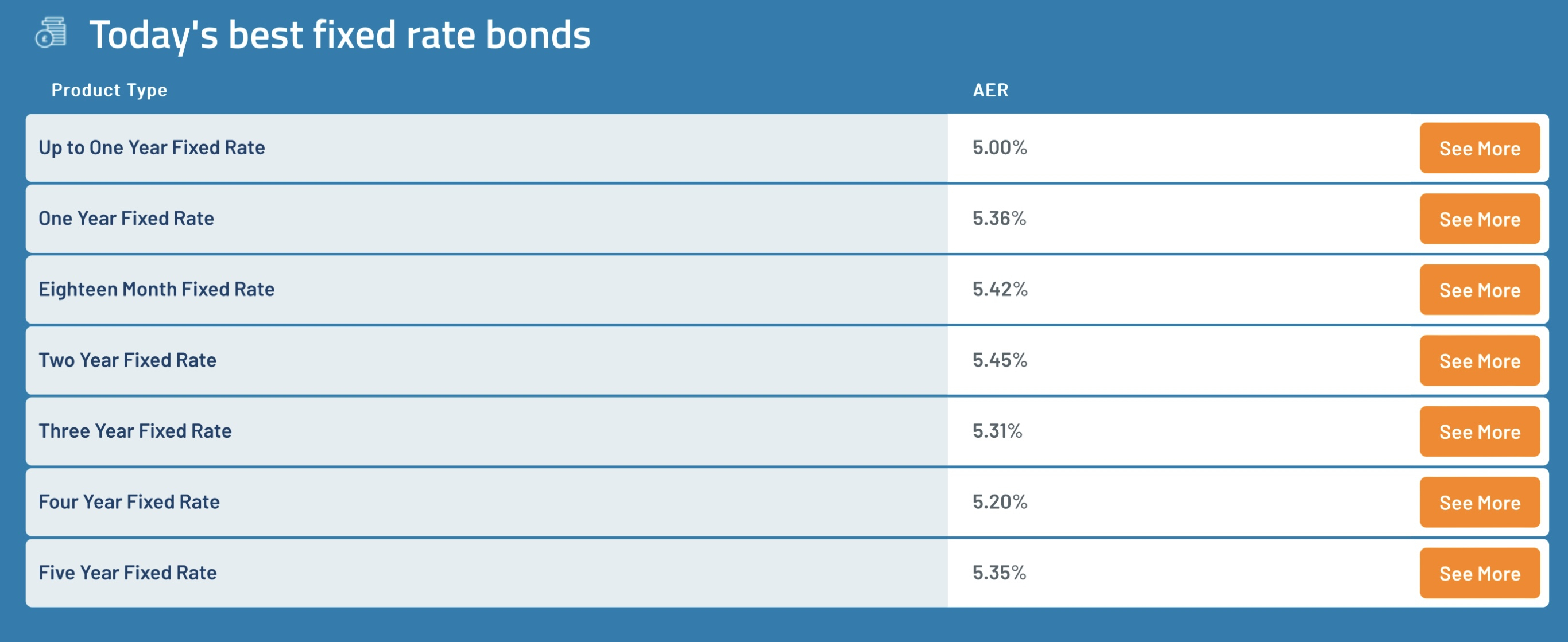

If your plan is to hold to maturity savings accounts are offering better rates, see below. It depends how much you're looking to deposit but you can find 5% to 6.25% instant access accounts e.g., Barclays Rainy Day Saver 5% on up to £5k plus various regular savers e.g., Lloyds Club £400pm 6.25%.

3

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards