We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Retirement planning

Comments

-

FWIW I get 3.3% using 50/50 global equities and global agg bonds, so as you point out, underlying data can make a difference.OldScientist said:

The Pfau study quoted in the finalytiq site uses bills (i.e. something close to cash) rather than bonds to get value of 3.4% for the UK, Pfau's earlier work (using bonds, https://www.advisorperspectives.com/articles/2014/03/04/does-international-diversification-improve-safe-withdrawal-rates) gave a UK safemax of 3.1% for a 50/50 portfolio. Estrada (Maximum Withdrawal rates: An empirical and Global Perspective, 2016) has, as far as I am aware, the most comprehensive published analysis of UK withdrawal rates (and the performance of many other countries too) with safe withdrawal rates (at 1% failure - values will be close enough to Safemax) ranging from 3.1% (portfolio 50/50 stocks/bonds) to 3.5% (at 80/20) - for portfolios with plenty of fixed income, using bills instead of bonds might raise these. According to the values presented by Estrada, the difference between UK and USA SWR is around 0.5% (the exact value depends on the asset allocation).BritishInvestor said:jamesd said:Something around £40,000 to £65,000 should be fine with two state pensions and a million in savings and investments depending on retirement age and income flexibility level. However, I noticed that you wrote about you having a million, not a million between you. Does your partner also have invested assets, meaning something other than the home you live in?

A useful general approach is to deduct state pension times the number of years until it can start from your initial capital. That removes 2 * £9,500 * 8 = £152,000 to deduct leaving £880k.

Next is considering what sort of safe withdrawal rate is possible. There are many "rules" (guidance not law) available which have been back tested and found to be safe for any historic starting point in the last 120 or so years. That's not a guarantee but it's high probability and if you do live through something worse you'll have to do some cutting.

The oldest and best known is "constant inflation-adjusted income", colloquially called the "4% rule" because that's it's number for Americans. The UK one for 30 years is 0.3 lower, so 3.7% before costs. The effect of costs is a reduction by a third of them, so say take another 0.2 off for 0.6% total costs, taking it down to 3.5%. With this rule you'd start at 3.5% of your capital and increase with uncapped inflation every year for a 30 year plan. The average of all US starting periods was 7% so this rule being based on the worst case is very cautious and its originator in the US is using 5% himself.At 60 with this rule you might take 3.5% of £880k, £30,800, and add the two state pensions or their substitute for a total annual income of £49,800 from age 60. Assumes between 50% and 75% equity investments.

One alternative set of rules is Guyton-Klinger. These start at 5.5% in the UK before costs, so cut to 5.2%. This is for a 40 year plan, not 30. These rules usually increase with uncapped inflation but in bad years that is skipped. After particularly bad years or a bad sequence there may be an additional cut of up to 10% once a year. In better times, a similar increase. This flexibility is what allows the higher income at the start, closer to average. With these you'd start at 0.052 * £880,000 + 2 * £9,500 = £64,760 variable. This assumes 65% equities.

Say you want to consider retiring at 50 and assuming you have enough money outside pensions to draw on. In this case you'd need 2 * £9,500 * 18 = £342,000 to cover the pre-state pension years. Deducting from a million leaves £658,000.

4% rule at 50 has to have about 0.2 more deducted to make a 40 year plan, taking it down to 3.3%. That results in an income of £19,000 + 0.033 * £658,000 = £40,174 a year.

GK already is for 40 years so that one is £19,000 + 0.052 * £658,000 = £53,215.

Maybe you want to retire at 50 or even 48? That seems doable with an income at least a third higher than your indicated £30,000 need.

If more is needed it's also reasonable to make plans assuming equity release to further boost bad case income levels, knowing that in the average case it probably won't be needed, though this depends on property value just how much extra income is planned for.

"The UK one for 30 years is 0.3 lower, so 3.7% before costs"

Some studies show ~3.4%

https://finalytiq.co.uk/withdrawal-rates-in-retirement-portfolios-is-the-4-rule-safe-for-uk-clients/

"The effect of costs is a reduction by a third of them, so say take another 0.2 off for 0.6% total costs"

I see it as closer to 0.5%

https://finalytiq.co.uk/impact-of-adviser-fees-on-withdrawal-rates-in-retirement-portfolio/

You've then got to bear in mind typical investor underperformance

https://www.morningstar.com/articles/1056151/why-fund-returns-are-lower-than-you-might-think0 -

Thanks for comments. Reason for this is to check if we can do this without me going back to more highly paid job with unsociable hours?

My assets to help

115k my house which is rent

425k cash PB accounts currently looking at investing

350k Invested with HL

Pensions 182k

iWeb 20k

We are living in partners house and she has only about 5k in savings0 -

It seems to me that boosting your partner's situation is the way to go.

You both get an annual tax personal allowance and it doesn't look like they will use theirs so you will need to withdraw more taxable money.

Increase their pension and invest some of that massive cash sum is what I would do.

What about mortgages on theses properties?1 -

I wonder what it will look like in 12 years time if the OP and partner are still saving and paying into pension.flopsy1973 said:Thanks for comments. Reason for this is to check if we can do this without me going back to more highly paid job with unsociable hours?

My assets to help

115k my house which is rent

425k cash PB accounts currently looking at investing

350k Invested with HL

Pensions 182k

iWeb 20k

We are living in partners house and she has only about 5k in savings

Mr Straw described whiplash as "not so much an injury, more a profitable invention of the human imagination—undiagnosable except by third-rate doctors in the pay of the claims management companies or personal injury lawyers"0 -

We are living in partners house and she has only about 5k in savings

Does she have a job , with a pension ?

As suggested above adding more to a pension for her looks a good idea but how much depends on the above question.

425k cash PB accounts currently looking at investing

Presume there was a reason to build up a huge cash pile , rather than investing it . So what has changed ?

Switching large amounts from safe cash to investments in one go , is probably the logical move , but it is not for the faint hearted.

0 -

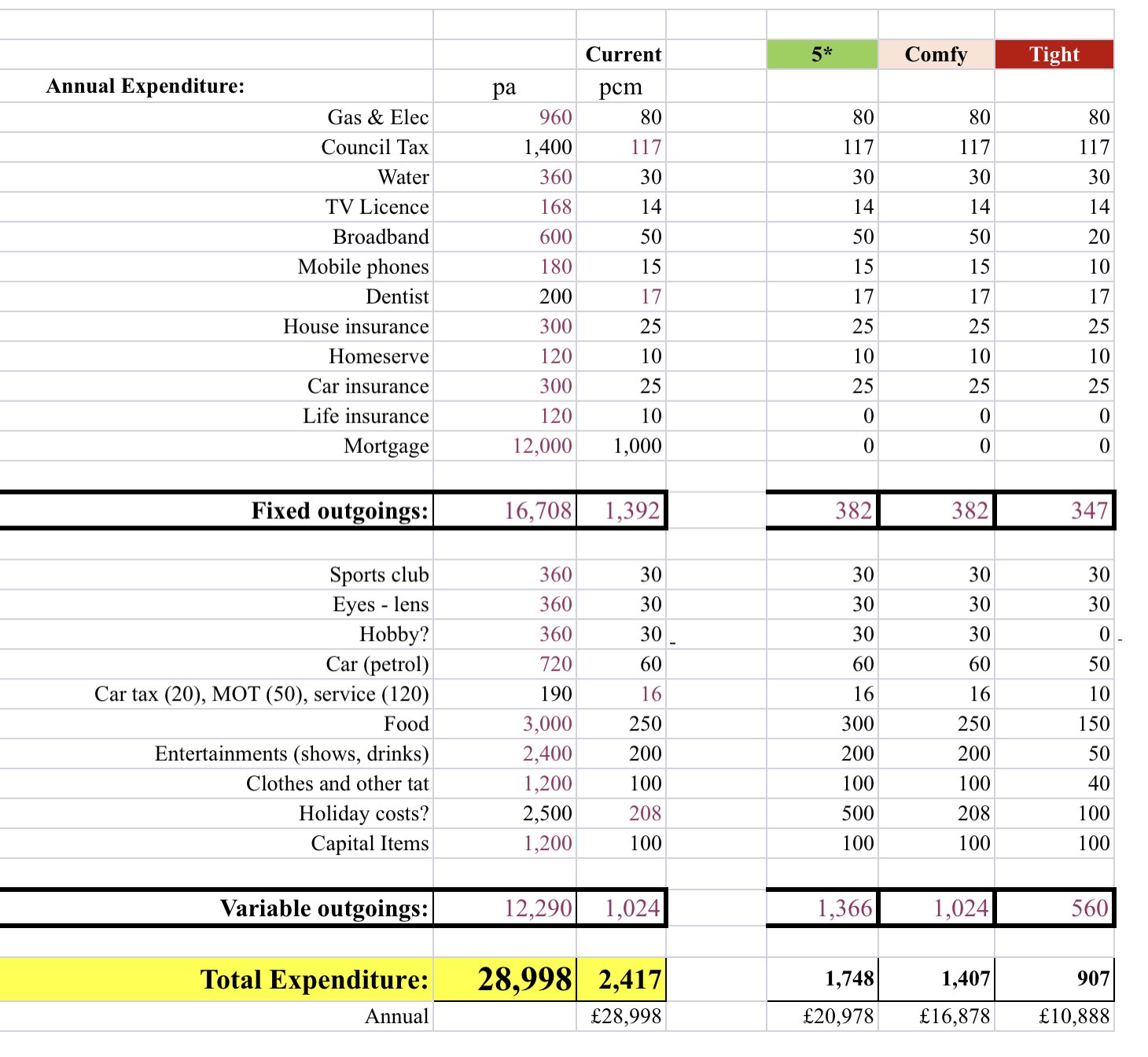

I'm not sure these figures are up-to-date as £20,978 certainly wouldn't give us, or I suspect most retired couples, a 5* retirement lifestyle. The Which website estimates £41k for a luxury retirement lifestyle for a couple, and I'm sure I saw a link from this forum to another site recently which had £47k for a luxury retirement lifestyle for a couple.cfw1994 said:

Sounds like the route to madness to me 😜westv said:

It may not be wise to use it as a definitive figure but it can be used as a guide. Yes, certain costs will go but, on the other hand, certain non one-off costs could increase. Looking at what other retirees have spent more money on can assist in deciding what a working person might spend more on once retired.Linton said:

Using published research to determine your income needs in requirement is a seriously bad idea. One person’s “comfortable” could be seen as luxury or penury by someone else. It would be better to determine how much you are spending now, reduce it by the items that won’t apply in retirement and use that as the starting point. You may then wish to include one-offs such as extra holidays, car replacement etc.flopsy1973 said:Hi

Me and OH are looking to retire at 60 I am 48 now and I have assets of about 1 million. We will both get full state pension at 68. We were looking at funding the gap between 60 till 68 with our savings to give us joint income of about 30k to give us comftarble living according to research? . Then when our state pension kicks in we can just top up the pension with our savings to give us that approx income of 30k. Are there any problems with this simple idea is it achieveble ? I did try find some pension calculator to see if this would work but no luck. Any feedback or suggestions

Everyone need to “DYOR” into what they spend. If you have no idea of that, you aren’t ready to retire, I would suggest.Start at The Number thread if you have never budgeted before.Figure out your essential spend items (monthly/quarterly/annual bills that are pretty non-negotiable), identify and add on the discretionary spend and figure out the desirable.

Something like this:

(These numbers are just generic ones, not ours….& you can see assumes the mortgage number shown has gone by retirement 😉)

I view the “comfy” as being “as things are now”.“Tight” would be drawing the belt in, perhaps markets drop and you don’t want to risk your savings pots, maybe for other reasons.“5*” is the retirement you would desire: more on holidays, entertainment perhaps.

Studis can certainly give their idea of a guide, but thinking they will match your lifestyle is a bit…..dangerous!0 -

I'll ponder that 3.4% result because what I already use is the result of several different sources. You linked to Araham Okuyana's Feb 2015 post and his Nov 2015 post says "More than 100 years of market data for a 60/40 portfolio puts the SWR for the UK at 3.7%" with a 60:40 portfolio. For the moment, given the inherent uncertainties, I remain comfortable with 0.3 lower in the UK for a range of 50-75% equities and 30 years as a decently reasonable one to use. However, I do read what you and others write and ponder whether I should adjust that or whether it's no longer sufficiently good to use just one number. I've been wondering also whether it's worth tying to put together a range of studies of this in one topic to try to consolidate them and provide a handy reference.BritishInvestor said:

"The UK one for 30 years is 0.3 lower, so 3.7% before costs"

Some studies show ~3.4%

https://finalytiq.co.uk/withdrawal-rates-in-retirement-portfolios-is-the-4-rule-safe-for-uk-clients/

"The effect of costs is a reduction by a third of them, so say take another 0.2 off for 0.6% total costs"

I see it as closer to 0.5%

https://finalytiq.co.uk/impact-of-adviser-fees-on-withdrawal-rates-in-retirement-portfolio/

You've then got to bear in mind typical investor underperformance

https://www.morningstar.com/articles/1056151/why-fund-returns-are-lower-than-you-might-think

I do not agree with the 50% effect of costs in Abraham Okusanya's Feb 2015 post because it seems to be clearly wrong. It used a start date of 1973 which is not the UK or US worst case. In the worst case the fees are lower because the amount of money on which the fees are charged is depleted faster. It's also somewhat sensitive to duration, being a higher deduction for longer periods, but not to a great enough extent to matter if adjustments of 0.1 or more are being used - which is about the precision limit for any sensible discussion given all of the uncertainties. For around a third or thirty percent I used Kitces analysis at SAFEMAX in the US for 30 years which did have the pot depletion effect. Abraham himself suggests 0.4% in a Guyton-Klinger context in his Jan 2016 comment here: "Because the SWR is the very worse case scenario, every 1% of fees tend to reduce SWR by 0.40%!"

Investors don't seem to be underperforming in that study. It seems to look at the accumulation phase and observe that the gains of early regular investing can be offset by later losses when the pot size is larger, which isn't an investor failure effect. In the decumulation phase it's interesting to consider whether an increase might be seen instead, as the pot size reduces and so will the effect of later decreases in value. However, since SWRs already take cash flows into account it doesn't seem to adjust the SWR value.

0 -

Wealth in retirement should not be very different to what you are used to.. If you want to take up an expensive hobby then explicitly account for it. Otherwise, the objective is too ensure you can maintain the same standard of living in retirement as you enjoyed whilst working. If you cant you may well be unhappy, if you have a lot more wealth in retirement than you are used to then you could have retired earlier and tthere is the possibility that you may not be able to usefully spend it.westv said:

I don't agree. You can know what you spend NOW but it won't necessarily help you to know what additional daily/weekly/monthly spending you might have when retired.cfw1994 said:

Sounds like the route to madness to me 😜westv said:

It may not be wise to use it as a definitive figure but it can be used as a guide. Yes, certain costs will go but, on the other hand, certain non one-off costs could increase. Looking at what other retirees have spent more money on can assist in deciding what a working person might spend more on once retired.Linton said:

Using published research to determine your income needs in requirement is a seriously bad idea. One person’s “comfortable” could be seen as luxury or penury by someone else. It would be better to determine how much you are spending now, reduce it by the items that won’t apply in retirement and use that as the starting point. You may then wish to include one-offs such as extra holidays, car replacement etc.flopsy1973 said:Hi

Me and OH are looking to retire at 60 I am 48 now and I have assets of about 1 million. We will both get full state pension at 68. We were looking at funding the gap between 60 till 68 with our savings to give us joint income of about 30k to give us comftarble living according to research? . Then when our state pension kicks in we can just top up the pension with our savings to give us that approx income of 30k. Are there any problems with this simple idea is it achieveble ? I did try find some pension calculator to see if this would work but no luck. Any feedback or suggestions

Everyone need to “DYOR” into what they spend. If you have no idea of that, you aren’t ready to retire, I would suggest.

I dont believe coming up with a total budget from a list of general categories is the best approach. The chances are you actually spend significant money on other things that make live worthwhile for you.1 -

What do you mean withdraw more taxable money?AlanP_2 said:It seems to me that boosting your partner's situation is the way to go.

You both get an annual tax personal allowance and it doesn't look like they will use theirs so you will need to withdraw more taxable money.

Increase their pension and invest some of that massive cash sum is what I would do.

What about mortgages on theses properties?

The mortgage on mine is 6k only keeping it cos of getting more cashback than I pay interest

Hers is around 30k and she has work nest pension with very little in it0 -

Looks as though it's OK to retire now if you both wanted to. You might want to work for another few years to get more discretionary spending and to allow for income to increase with earnings rather than inflation, which is about 1% higher a year. I'm assuming no mortgages.flopsy1973 said:Thanks for comments. Reason for this is to check if we can do this without me going back to more highly paid job with unsociable hours?

My assets to help

115k my house which is rent

425k cash PB accounts currently looking at investing

350k Invested with HL

Pensions 182k

iWeb 20k

We are living in partners house and she has only about 5k in savings

One thing that can make a difference is a bit of work, but not full time and not what you hate. In this way of thinking o things, retirement means no longer forced to work to live but doing what you think is more desirable and better matches what you fancy doing.

I'm assuming that 115k "which is rent" means you are renting it out and making money from it. Excluding that you have around a million and that's enough to retire if you want to.

You might want to read the safe withdrawal rate thread and what it links to as well as the discussion here of how safe withdrawal rates can vary with different assumptions but you still seem to have plenty of margin for a £30k a year target. Easy enough for you to experiment with the different values and rules.

We're still in a low interest rate, low inflation situation thought hat may change. US work showed that cash-equivalents beat bond-equivalents in this situation so don't be too keen to immediately switch to bonds. By bonds I don't mean term savings accounts like one or three years, but company or government debt, what the word normally means for investing.

Even for retiring now you seem to have too much outside pensions. In the near worst case if you get 20% tax relief and pay 20% tax on all but 25% on the way out you make a free 6.5% gain just on the pension tax relief. In practice for early retirement you'll often also be able to withdraw much of your income tax personal allowance free of any tax, though this depends on how rent is handled. You need to allow enough to live on before you reach pension access age of 55 (rising to 57 for many but not all pensions in 2028, details still unclear) but beyond that it'll pay you well to contribute as much as the law allows while still working. For both of you. Limits are 40k for combined personal and employer contributions, plus carry-forward of unused annual allowance from the previous three years, and for personal contributions your gross pay in the year of the pension contributions. Don't exceed either limit.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.2K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.2K Work, Benefits & Business

- 603.9K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.4K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards