We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Retirement planning

flopsy1973

Posts: 764 Forumite

Hi

Me and OH are looking to retire at 60 I am 48 now and I have assets of about 1 million. We will both get full state pension at 68. We were looking at funding the gap between 60 till 68 with our savings to give us joint income of about 30k to give us comftarble living according to research? . Then when our state pension kicks in we can just top up the pension with our savings to give us that approx income of 30k. Are there any problems with this simple idea is it achieveble ? I did try find some pension calculator to see if this would work but no luck. Any feedback or suggestions

Me and OH are looking to retire at 60 I am 48 now and I have assets of about 1 million. We will both get full state pension at 68. We were looking at funding the gap between 60 till 68 with our savings to give us joint income of about 30k to give us comftarble living according to research? . Then when our state pension kicks in we can just top up the pension with our savings to give us that approx income of 30k. Are there any problems with this simple idea is it achieveble ? I did try find some pension calculator to see if this would work but no luck. Any feedback or suggestions

0

Comments

-

Are your current assets of about a million invested and readily realisable as cash, or is a large slug of that figure the property you live in?flopsy1973 said:Hi

Me and OH are looking to retire at 60 I am 48 now and I have assets of about 1 million. We will both get full state pension at 68. We were looking at funding the gap between 60 till 68 with our savings to give us joint income of about 30k to give us comftarble living according to research? . Then when our state pension kicks in we can just top up the pension with our savings to give us that approx income of 30k. Are there any problems with this simple idea is it achieveble ? I did try find some pension calculator to see if this would work but no luck. Any feedback or suggestions

What non-state pension provision do you both have? Your question suggests you don't have any, given you refer to 'savings' - but possibly the terms covers pension savings as well as other investments?Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!1 -

Entirely possible. Three thoughts spring to mind:

1. What does 'assets' mean. If it's 100% cash, it will gradually be eroded by inflation. To sustain a 30yr retirement you will need some of it invested in something. Also, you can't count the house you live in. Maybe half of it as you can do equity release, but not the whole value.

2. Do you have sufficient liquid assets to fund you from 60 to 68. Some people have big pensions, but it's not advantageous to access them early. If you have ISA's or cash of 1/4 mil or more, you should be okay.

3. If the money is coming from pensions, or properties (other than your home), there will be some tax to pay, so you will be drawing down more than 30k to get to 30k spending money.

If you have investments of 1 mil, sufficient liquidity to get to 68, not too much tax to pay, and 2 state pensions, you should be able to draw more than 30k without any worries. Almost everyone will accept that using 3% per year of your investments isn't going to lead to running out, and you are only proposing to do that for 8 yrs, then drop to 1%.

You might well leave an inheritance which is more money than most people ever see.1 -

Something around £40,000 to £65,000 should be fine with two state pensions and a million in savings and investments depending on retirement age and income flexibility level. However, I noticed that you wrote about you having a million, not a million between you. Does your partner also have invested assets, meaning something other than the home you live in?

A useful general approach is to deduct state pension times the number of years until it can start from your initial capital. That removes 2 * £9,500 * 8 = £152,000 to deduct leaving £880k.

Next is considering what sort of safe withdrawal rate is possible. There are many "rules" (guidance not law) available which have been back tested and found to be safe for any historic starting point in the last 120 or so years. That's not a guarantee but it's high probability and if you do live through something worse you'll have to do some cutting.

The oldest and best known is "constant inflation-adjusted income", colloquially called the "4% rule" because that's it's number for Americans. The UK one for 30 years is 0.3 lower, so 3.7% before costs. The effect of costs is a reduction by a third of them, so say take another 0.2 off for 0.6% total costs, taking it down to 3.5%. With this rule you'd start at 3.5% of your capital and increase with uncapped inflation every year for a 30 year plan. The average of all US starting periods was 7% so this rule being based on the worst case is very cautious and its originator in the US is using 5% himself.At 60 with this rule you might take 3.5% of £880k, £30,800, and add the two state pensions or their substitute for a total annual income of £49,800 from age 60. Assumes between 50% and 75% equity investments.

One alternative set of rules is Guyton-Klinger. These start at 5.5% in the UK before costs, so cut to 5.2%. This is for a 40 year plan, not 30. These rules usually increase with uncapped inflation but in bad years that is skipped. After particularly bad years or a bad sequence there may be an additional cut of up to 10% once a year. In better times, a similar increase. This flexibility is what allows the higher income at the start, closer to average. With these you'd start at 0.052 * £880,000 + 2 * £9,500 = £64,760 variable. This assumes 65% equities.

Say you want to consider retiring at 50 and assuming you have enough money outside pensions to draw on. In this case you'd need 2 * £9,500 * 18 = £342,000 to cover the pre-state pension years. Deducting from a million leaves £658,000.

4% rule at 50 has to have about 0.2 more deducted to make a 40 year plan, taking it down to 3.3%. That results in an income of £19,000 + 0.033 * £658,000 = £40,174 a year.

GK already is for 40 years so that one is £19,000 + 0.052 * £658,000 = £53,215.

Maybe you want to retire at 50 or even 48? That seems doable with an income at least a third higher than your indicated £30,000 need.

If more is needed it's also reasonable to make plans assuming equity release to further boost bad case income levels, knowing that in the average case it probably won't be needed, though this depends on property value just how much extra income is planned for.

4 -

jamesd said:Something around £40,000 to £65,000 should be fine with two state pensions and a million in savings and investments depending on retirement age and income flexibility level. However, I noticed that you wrote about you having a million, not a million between you. Does your partner also have invested assets, meaning something other than the home you live in?

A useful general approach is to deduct state pension times the number of years until it can start from your initial capital. That removes 2 * £9,500 * 8 = £152,000 to deduct leaving £880k.

Next is considering what sort of safe withdrawal rate is possible. There are many "rules" (guidance not law) available which have been back tested and found to be safe for any historic starting point in the last 120 or so years. That's not a guarantee but it's high probability and if you do live through something worse you'll have to do some cutting.

The oldest and best known is "constant inflation-adjusted income", colloquially called the "4% rule" because that's it's number for Americans. The UK one for 30 years is 0.3 lower, so 3.7% before costs. The effect of costs is a reduction by a third of them, so say take another 0.2 off for 0.6% total costs, taking it down to 3.5%. With this rule you'd start at 3.5% of your capital and increase with uncapped inflation every year for a 30 year plan. The average of all US starting periods was 7% so this rule being based on the worst case is very cautious and its originator in the US is using 5% himself.At 60 with this rule you might take 3.5% of £880k, £30,800, and add the two state pensions or their substitute for a total annual income of £49,800 from age 60. Assumes between 50% and 75% equity investments.

One alternative set of rules is Guyton-Klinger. These start at 5.5% in the UK before costs, so cut to 5.2%. This is for a 40 year plan, not 30. These rules usually increase with uncapped inflation but in bad years that is skipped. After particularly bad years or a bad sequence there may be an additional cut of up to 10% once a year. In better times, a similar increase. This flexibility is what allows the higher income at the start, closer to average. With these you'd start at 0.052 * £880,000 + 2 * £9,500 = £64,760 variable. This assumes 65% equities.

Say you want to consider retiring at 50 and assuming you have enough money outside pensions to draw on. In this case you'd need 2 * £9,500 * 18 = £342,000 to cover the pre-state pension years. Deducting from a million leaves £658,000.

4% rule at 50 has to have about 0.2 more deducted to make a 40 year plan, taking it down to 3.3%. That results in an income of £19,000 + 0.033 * £658,000 = £40,174 a year.

GK already is for 40 years so that one is £19,000 + 0.052 * £658,000 = £53,215.

Maybe you want to retire at 50 or even 48? That seems doable with an income at least a third higher than your indicated £30,000 need.

If more is needed it's also reasonable to make plans assuming equity release to further boost bad case income levels, knowing that in the average case it probably won't be needed, though this depends on property value just how much extra income is planned for.

"The UK one for 30 years is 0.3 lower, so 3.7% before costs"

Some studies show ~3.4%

https://finalytiq.co.uk/withdrawal-rates-in-retirement-portfolios-is-the-4-rule-safe-for-uk-clients/

"The effect of costs is a reduction by a third of them, so say take another 0.2 off for 0.6% total costs"

I see it as closer to 0.5%

https://finalytiq.co.uk/impact-of-adviser-fees-on-withdrawal-rates-in-retirement-portfolio/

You've then got to bear in mind typical investor underperformance

https://www.morningstar.com/articles/1056151/why-fund-returns-are-lower-than-you-might-think

2 -

Using published research to determine your income needs in requirement is a seriously bad idea. One person’s “comfortable” could be seen as luxury or penury by someone else. It would be better to determine how much you are spending now, reduce it by the items that won’t apply in retirement and use that as the starting point. You may then wish to include one-offs such as extra holidays, car replacement etc.flopsy1973 said:Hi

Me and OH are looking to retire at 60 I am 48 now and I have assets of about 1 million. We will both get full state pension at 68. We were looking at funding the gap between 60 till 68 with our savings to give us joint income of about 30k to give us comftarble living according to research? . Then when our state pension kicks in we can just top up the pension with our savings to give us that approx income of 30k. Are there any problems with this simple idea is it achieveble ? I did try find some pension calculator to see if this would work but no luck. Any feedback or suggestions4 -

It may not be wise to use it as a definitive figure but it can be used as a guide. Yes, certain costs will go but, on the other hand, certain non one-off costs could increase. Looking at what other retirees have spent more money on can assist in deciding what a working person might spend more on once retired.Linton said:

Using published research to determine your income needs in requirement is a seriously bad idea. One person’s “comfortable” could be seen as luxury or penury by someone else. It would be better to determine how much you are spending now, reduce it by the items that won’t apply in retirement and use that as the starting point. You may then wish to include one-offs such as extra holidays, car replacement etc.flopsy1973 said:Hi

Me and OH are looking to retire at 60 I am 48 now and I have assets of about 1 million. We will both get full state pension at 68. We were looking at funding the gap between 60 till 68 with our savings to give us joint income of about 30k to give us comftarble living according to research? . Then when our state pension kicks in we can just top up the pension with our savings to give us that approx income of 30k. Are there any problems with this simple idea is it achieveble ? I did try find some pension calculator to see if this would work but no luck. Any feedback or suggestions1 -

You can see from some of the posts that considering you are talking about large sums of money and decades long plans , the amount of info you have supplied is rather inadequate . Especially this rather vague statement that you have assets of One Million Pounds ( cash? pension, property?)flopsy1973 said:Hi

Me and OH are looking to retire at 60 I am 48 now and I have assets of about 1 million. We will both get full state pension at 68. We were looking at funding the gap between 60 till 68 with our savings to give us joint income of about 30k to give us comftarble living according to research? . Then when our state pension kicks in we can just top up the pension with our savings to give us that approx income of 30k. Are there any problems with this simple idea is it achieveble ? I did try find some pension calculator to see if this would work but no luck. Any feedback or suggestions

Also if you continue working for another 12 years , presume you will have more ? Or you and your partner ?0 -

Sounds like the route to madness to me 😜westv said:

It may not be wise to use it as a definitive figure but it can be used as a guide. Yes, certain costs will go but, on the other hand, certain non one-off costs could increase. Looking at what other retirees have spent more money on can assist in deciding what a working person might spend more on once retired.Linton said:

Using published research to determine your income needs in requirement is a seriously bad idea. One person’s “comfortable” could be seen as luxury or penury by someone else. It would be better to determine how much you are spending now, reduce it by the items that won’t apply in retirement and use that as the starting point. You may then wish to include one-offs such as extra holidays, car replacement etc.flopsy1973 said:Hi

Me and OH are looking to retire at 60 I am 48 now and I have assets of about 1 million. We will both get full state pension at 68. We were looking at funding the gap between 60 till 68 with our savings to give us joint income of about 30k to give us comftarble living according to research? . Then when our state pension kicks in we can just top up the pension with our savings to give us that approx income of 30k. Are there any problems with this simple idea is it achieveble ? I did try find some pension calculator to see if this would work but no luck. Any feedback or suggestions

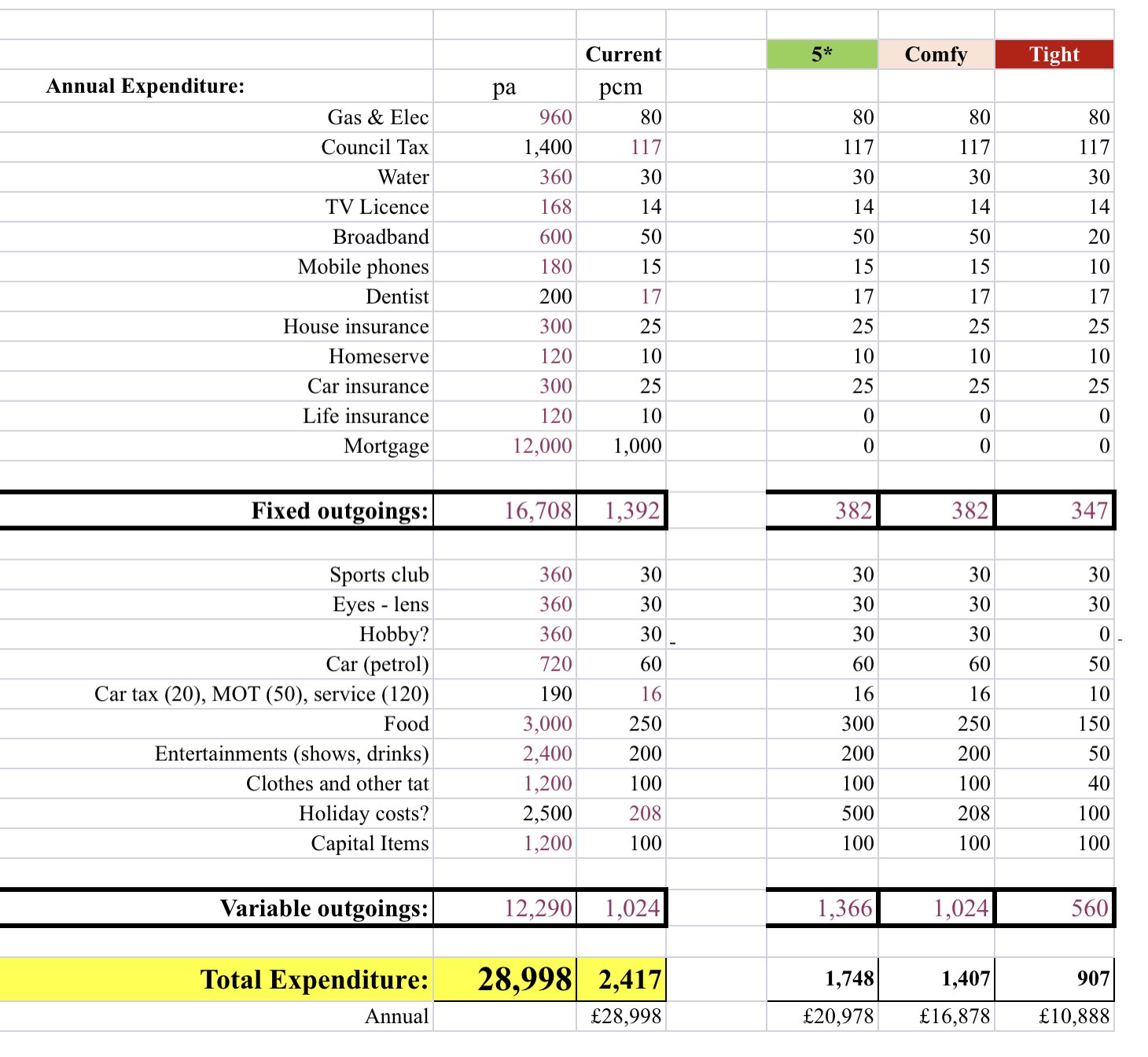

Everyone need to “DYOR” into what they spend. If you have no idea of that, you aren’t ready to retire, I would suggest.Start at The Number thread if you have never budgeted before.Figure out your essential spend items (monthly/quarterly/annual bills that are pretty non-negotiable), identify and add on the discretionary spend and figure out the desirable.

Something like this:

(These numbers are just generic ones, not ours….& you can see assumes the mortgage number shown has gone by retirement 😉)

I view the “comfy” as being “as things are now”.“Tight” would be drawing the belt in, perhaps markets drop and you don’t want to risk your savings pots, maybe for other reasons.“5*” is the retirement you would desire: more on holidays, entertainment perhaps.

Studis can certainly give their idea of a guide, but thinking they will match your lifestyle is a bit…..dangerous!Plan for tomorrow, enjoy today!5 -

I don't agree. You can know what you spend NOW but it won't necessarily help you to know what additional daily/weekly/monthly spending you might have when retired.cfw1994 said:

Sounds like the route to madness to me 😜westv said:

It may not be wise to use it as a definitive figure but it can be used as a guide. Yes, certain costs will go but, on the other hand, certain non one-off costs could increase. Looking at what other retirees have spent more money on can assist in deciding what a working person might spend more on once retired.Linton said:

Using published research to determine your income needs in requirement is a seriously bad idea. One person’s “comfortable” could be seen as luxury or penury by someone else. It would be better to determine how much you are spending now, reduce it by the items that won’t apply in retirement and use that as the starting point. You may then wish to include one-offs such as extra holidays, car replacement etc.flopsy1973 said:Hi

Me and OH are looking to retire at 60 I am 48 now and I have assets of about 1 million. We will both get full state pension at 68. We were looking at funding the gap between 60 till 68 with our savings to give us joint income of about 30k to give us comftarble living according to research? . Then when our state pension kicks in we can just top up the pension with our savings to give us that approx income of 30k. Are there any problems with this simple idea is it achieveble ? I did try find some pension calculator to see if this would work but no luck. Any feedback or suggestions

Everyone need to “DYOR” into what they spend. If you have no idea of that, you aren’t ready to retire, I would suggest.0 -

The Pfau study quoted in the finalytiq site uses bills (i.e. something close to cash) rather than bonds to get value of 3.4% for the UK, Pfau's earlier work (using bonds, https://www.advisorperspectives.com/articles/2014/03/04/does-international-diversification-improve-safe-withdrawal-rates) gave a UK safemax of 3.1% for a 50/50 portfolio. Estrada (Maximum Withdrawal rates: An empirical and Global Perspective, 2016) has, as far as I am aware, the most comprehensive published analysis of UK withdrawal rates (and the performance of many other countries too) with safe withdrawal rates (at 1% failure - values will be close enough to Safemax) ranging from 3.1% (portfolio 50/50 stocks/bonds) to 3.5% (at 80/20) - for portfolios with plenty of fixed income, using bills instead of bonds might raise these. According to the values presented by Estrada, the difference between UK and USA SWR is around 0.5% (the exact value depends on the asset allocation).BritishInvestor said:jamesd said:Something around £40,000 to £65,000 should be fine with two state pensions and a million in savings and investments depending on retirement age and income flexibility level. However, I noticed that you wrote about you having a million, not a million between you. Does your partner also have invested assets, meaning something other than the home you live in?

A useful general approach is to deduct state pension times the number of years until it can start from your initial capital. That removes 2 * £9,500 * 8 = £152,000 to deduct leaving £880k.

Next is considering what sort of safe withdrawal rate is possible. There are many "rules" (guidance not law) available which have been back tested and found to be safe for any historic starting point in the last 120 or so years. That's not a guarantee but it's high probability and if you do live through something worse you'll have to do some cutting.

The oldest and best known is "constant inflation-adjusted income", colloquially called the "4% rule" because that's it's number for Americans. The UK one for 30 years is 0.3 lower, so 3.7% before costs. The effect of costs is a reduction by a third of them, so say take another 0.2 off for 0.6% total costs, taking it down to 3.5%. With this rule you'd start at 3.5% of your capital and increase with uncapped inflation every year for a 30 year plan. The average of all US starting periods was 7% so this rule being based on the worst case is very cautious and its originator in the US is using 5% himself.At 60 with this rule you might take 3.5% of £880k, £30,800, and add the two state pensions or their substitute for a total annual income of £49,800 from age 60. Assumes between 50% and 75% equity investments.

One alternative set of rules is Guyton-Klinger. These start at 5.5% in the UK before costs, so cut to 5.2%. This is for a 40 year plan, not 30. These rules usually increase with uncapped inflation but in bad years that is skipped. After particularly bad years or a bad sequence there may be an additional cut of up to 10% once a year. In better times, a similar increase. This flexibility is what allows the higher income at the start, closer to average. With these you'd start at 0.052 * £880,000 + 2 * £9,500 = £64,760 variable. This assumes 65% equities.

Say you want to consider retiring at 50 and assuming you have enough money outside pensions to draw on. In this case you'd need 2 * £9,500 * 18 = £342,000 to cover the pre-state pension years. Deducting from a million leaves £658,000.

4% rule at 50 has to have about 0.2 more deducted to make a 40 year plan, taking it down to 3.3%. That results in an income of £19,000 + 0.033 * £658,000 = £40,174 a year.

GK already is for 40 years so that one is £19,000 + 0.052 * £658,000 = £53,215.

Maybe you want to retire at 50 or even 48? That seems doable with an income at least a third higher than your indicated £30,000 need.

If more is needed it's also reasonable to make plans assuming equity release to further boost bad case income levels, knowing that in the average case it probably won't be needed, though this depends on property value just how much extra income is planned for.

"The UK one for 30 years is 0.3 lower, so 3.7% before costs"

Some studies show ~3.4%

https://finalytiq.co.uk/withdrawal-rates-in-retirement-portfolios-is-the-4-rule-safe-for-uk-clients/

"The effect of costs is a reduction by a third of them, so say take another 0.2 off for 0.6% total costs"

I see it as closer to 0.5%

https://finalytiq.co.uk/impact-of-adviser-fees-on-withdrawal-rates-in-retirement-portfolio/

You've then got to bear in mind typical investor underperformance

https://www.morningstar.com/articles/1056151/why-fund-returns-are-lower-than-you-might-think

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.2K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.2K Work, Benefits & Business

- 603.9K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.4K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards