We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Using LifeStrategy 20 as a Bond Fund

Comments

-

aroominyork said:masonic said:I think the performance during the Covid crash gives a clue to the likely underperformance during a stockmarket downturn. It is, in effect, a lowish risk corporate bond fund. Only a quarter of the bonds are rated AAA-A vs over three quarters for the Vanguard fund, so considerably more credit risk is being taken on for those returns, which is fine while the companies can service their debts.Are you talking about the short duration fund? If you want AAA short duration bonds you are not going to get much in the way of returns; this fund's strategy is to pick from across the credit range to get its returns - although you did not mention that 48% of its holdings are BBB so the majority count as investment grade.'Investment grade is just a marketing gimmick, my point is that the credit ratings of the underlying assets are appreciably lower, so in a downturn default risk becomes significantly higher, which is exactly what you do not want in a defensive asset partnered with equities.

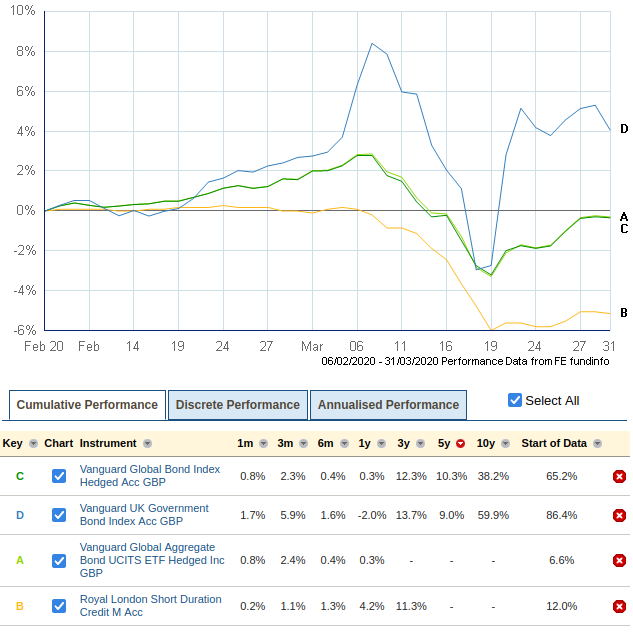

Things started to go awry before 6th March. You've zoomed in on the second half of an anomaly:aroominyork said:And re. underperformance during the Covid crash, it did no worse than Vanguard's global fund if you start the chart on the first day of the dip, 6 March 2020. See how the Vanguard funds rapidly go up about 2% before falling 6% in a couple of days, then there is a reversal almost back up to the starting level? Let's zoom in, and I'll also add the UK Gilt tracker which shows an even more pronounced effect...

See how the Vanguard funds rapidly go up about 2% before falling 6% in a couple of days, then there is a reversal almost back up to the starting level? Let's zoom in, and I'll also add the UK Gilt tracker which shows an even more pronounced effect... That initial flight to safety is important to include. It's pretty clear over those few weeks there is panic amongst investors and nobody knows what to do for the best. I suspect the currency hedging on the global fund also malfunctions here due to the volatility.The important point to note is from your original plot, the RL fund takes until November to catch back up to the government bond funds. In a more protracted crash that underperformance could last for years (as I personally experienced with some corporate bond funds in 2008).1

That initial flight to safety is important to include. It's pretty clear over those few weeks there is panic amongst investors and nobody knows what to do for the best. I suspect the currency hedging on the global fund also malfunctions here due to the volatility.The important point to note is from your original plot, the RL fund takes until November to catch back up to the government bond funds. In a more protracted crash that underperformance could last for years (as I personally experienced with some corporate bond funds in 2008).1 -

I thought the above warranted a bit more investigation. What is really needed is some backtesting that extends through previous crashes. For this, some alternative funds with an earlier inception need to be selected covering the same sectors as those above. The chart below compares (A) Short dated corporates vs (B) Gilts vs (C) Global government vs (D) IL Gilts with (E) Global equities to give a view of equities:

Some points to note are that all of the bond funds sailed through the dotcom crash relatively unscathed and all were broadly negatively correlated with equities. The global bond fund is not hedged (I couldn't find one in this era that was), a hedged equivalent would have performed better between 2003-2008 and worse from 2008 onwards due to exchange rate movements. What's more interesting is what happened during the gfc:

Some points to note are that all of the bond funds sailed through the dotcom crash relatively unscathed and all were broadly negatively correlated with equities. The global bond fund is not hedged (I couldn't find one in this era that was), a hedged equivalent would have performed better between 2003-2008 and worse from 2008 onwards due to exchange rate movements. What's more interesting is what happened during the gfc: First things first, the 40% rise in the global bonds fund would have been countered by a 30% devaluation in sterling by January 2009, so a hedged version would perform much more similarly to the UK gilts fund. This time, two funds were positively correlated with equities: index linked gilts (presumably due to disinflation and fears of deflation), and the corporate bond fund. The short dated corporate bond fund holds up a lot better than the longer duration sector average and falls sub-10% for a 20-30% fall in equities.Finally, as we have substituted that corporate bond fund, it would be useful to compare it with the original Royal London one since inception, and see that the latter has performed better in 2 out of 3 12 month periods, and is otherwise very similar in volatility and loss potential as measured by the Covid crash:

First things first, the 40% rise in the global bonds fund would have been countered by a 30% devaluation in sterling by January 2009, so a hedged version would perform much more similarly to the UK gilts fund. This time, two funds were positively correlated with equities: index linked gilts (presumably due to disinflation and fears of deflation), and the corporate bond fund. The short dated corporate bond fund holds up a lot better than the longer duration sector average and falls sub-10% for a 20-30% fall in equities.Finally, as we have substituted that corporate bond fund, it would be useful to compare it with the original Royal London one since inception, and see that the latter has performed better in 2 out of 3 12 month periods, and is otherwise very similar in volatility and loss potential as measured by the Covid crash: 4

4 -

Thanks. Always feels instructive, but I get no more confident in what to do. I was complaining about equities going nowhere for 15 years in 1930's. You've shown global equities going nowhere for 12 years (did I read that right?), presumably with dividends reinvested, and presumably that graph is nominal values. If so, and there was inflation where you lived holding global equities, it was even longer than 12 years to recover.

0 -

masonic said:aroominyork said:masonic said:I think the performance during the Covid crash gives a clue to the likely underperformance during a stockmarket downturn. It is, in effect, a lowish risk corporate bond fund. Only a quarter of the bonds are rated AAA-A vs over three quarters for the Vanguard fund, so considerably more credit risk is being taken on for those returns, which is fine while the companies can service their debts.Are you talking about the short duration fund? If you want AAA short duration bonds you are not going to get much in the way of returns; this fund's strategy is to pick from across the credit range to get its returns - although you did not mention that 48% of its holdings are BBB so the majority count as investment grade.'Investment grade is just a marketing gimmick, my point is that the credit ratings of the underlying assets are appreciably lower, so in a downturn default risk becomes significantly higher, which is exactly what you do not want in a defensive asset partnered with equities.Maybe short duration bonds of mixed credit ratings are a double edged sword in a downturn. On one side, the lower volatility of short duration is an advantage compared to other corporate bonds - you are more certain whether a bond maturing tomorrow will be repaid compared to a bond maturing in ten years. On the other side, a company struggling through a downturn has less time to turn things around - they may be able to repay in ten years but their cash flow won't let them repay tomorrow.Your points about gilts vs. bonds as defensive assets are well made. I guess it comes down to whether you want your fixed interest investments to be less volatile than equities while still providing some kind of meaningful income/growth, or to be purely defensive assets that correlate as little as possible with equities. Maybe that is why many novice investors struggle with fixed interest: we know our options with equities - chasing returns that match our approach to risk - but for FI there are very different paths to follow: high yield (equity proxy), middle-of-the-road strategic bond funds crammed with BBBs, investment grade, short duration, gilts...I want to bring this back to the OP's question of whether VLS20 is a sound approach to fixed interest. I chose VLS20 over Vanguard's global bond index because of better performance over a five year snapshot period. I have now looked at the difference between the FI assets in the two funds and, as with the equity component of VLS, it comes down to greater fixed interest exposure to the UK. So my question is whether, for fixed interest, there are reasons for having more exposure to the UK than the cap weighted 4-5%? I know the reasons for equities (home comforts; less forex exposure etc.) but how does this play out in fixed interest? Should I want more than 4-5% of my gilts to be issued by the UK rather than foreign governments?2

-

I think it's a different consideration with bonds, than equities. One country's equities can do badly compared with others', so you diversify. Government bond returns, excluding Greece, Argentina and their ilk, have similar yields I think, certainly nothing like the differences one country to another you can see with equities.If so, it's really just whether you think your country will default on you. It seems unlikely for the UK, but having some foreign bonds gives safety at not much cost (currency hedging). But you need your own governments linkers, not protection against someone else's inflation.0

-

Yup, because of the start of the century being such a poor time for equities it took around 18 years for the returns on equities to catch up with those on UK Gilts. I imagine that global bonds are still ahead of equities after 21 years.JohnWinder said:Thanks. Always feels instructive, but I get no more confident in what to do. I was complaining about equities going nowhere for 15 years in 1930's. You've shown global equities going nowhere for 12 years (did I read that right?), presumably with dividends reinvested, and presumably that graph is nominal values. If so, and there was inflation where you lived holding global equities, it was even longer than 12 years to recover.0 -

WW2 may have had an impact.JohnWinder said:I was complaining about equities going nowhere for 15 years in 1930's.") 1

1 -

aroominyork said:I want to bring this back to the OP's question of whether VLS20 is a sound approach to fixed interest. I chose VLS20 over Vanguard's global bond index because of better performance over a five year snapshot period. I have now looked at the difference between the FI assets in the two funds and, as with the equity component of VLS, it comes down to greater fixed interest exposure to the UK. So my question is whether, for fixed interest, there are reasons for having more exposure to the UK than the cap weighted 4-5%? I know the reasons for equities (home comforts; less forex exposure etc.) but how does this play out in fixed interest? Should I want more than 4-5% of my gilts to be issued by the UK rather than foreign governments?It would be good to come back to this, and to develop some of the points made while meandering around. We've discussed defensive multi asset funds like VLS 20, corporate bonds, global government bonds and UK Gilts (leaving index linking aside for the moment).The question on global vs UK bonds is a difficult one to answer. Popular commentators such as Lars Kroijer and Tim Hale advocate sticking to government bonds in your home currency providing they are of the highest credit quality, and there are logical arguments why this should be. Yet most of the multi-asset fund providers use global bonds and currency hedge them. At one time this seemed like a good option, due to the favourable situation with interest rates elsewhere in the world, and hence better yields on US Treasuries etc. However, this doesn't seem to have translated into higher effective yields/returns for UK investors. FeralHog rightly pointed out the drag on returns of the financial derivatives (both their cost and spread), and that this must, at least in part, counteract gains that could be made buying higher interest foreign bonds. I've found it quite difficult to disentangle the cost of hedging in the balance sheet of the annual report of one of the Vanguard hedged funds, but it appeared to me that a profit was made due to under-hedging during a period of weakening Sterling. That won't work when Sterling is strengthening and there is something to be gained from hedging. However, there does seem to be some advantage in terms of volatility reduction.The other aspect that has been mentioned is the concept of holding your nose and buying the highest quality government bonds vs lower quality bonds with a higher yield, so that you can hold fewer bonds and more equities. So, for example, if you take the oft-quoted 5% real return from equities (let's say 7.5% nominal at 2.5% inflation), current ~0.7% YTM from a UK Gilt fund, and ~2.7% effective yield from the corporate bond fund we have been discussing, could you construct something performing like the latter from the former two?Taking the global financial crisis performance, a 30% pulldown in equities resulted in a ~10% rise in the Gilt fund and a corresponding ~7% drop in the short-dated corporate bond fund. A combination of 60% Gilts and 40% global equities would have suffered a similar fall as the corporate bond fund. Assuming the holding period exceeds the bond duration, then the average returns from 60:40 Gilts/equities would be about 3.4%, vs about 2.7% from the corporates (there are some simplifications in here of course). That suggests if you were to hold Gilts instead of corporate bonds, you'd only need a little over half the quantity for a similar dampening effect, leaving you to invest more in equities at higher overall return. This is perhaps just fleshing out a point already made by JohnWinder with some numbers.I must say, I'm beginning to be swayed in favour of keeping things simple, with a small helping of Gilts in line with Hale/Kroijer's thinking.4

-

This thread has given me a better understanding of the purpose and nature of fixed interest investments. I have two conclusions: 1) Overweighting the UK feels right, especially if you want to minimise the number of funds and want some linkers in the mix. So I favour VLS20 over Vanguard Global Bond Index. The fixed interest in VLS seems have a bit more in gilts than in bonds and that suits me. However if someone knows a cheaper way (than VLS's 0.22% charge) to get a similar investment I would be glad to know it. 2) A strategic bond fund heavy in BBBs is perhaps a case of wanting to have your cake and eat it, and only in a downturn will it become clear that is not possible. I will therefore reduce my strategic fund holdings and increase VLS20 or similar.

0 -

I don't know about global bonds, but if you compare the FTSE 100 or All Share and the FTSE Actuaries UK Conventional Gilts All Stocks indices, this is still true.Prism said:

Yup, because of the start of the century being such a poor time for equities it took around 18 years for the returns on equities to catch up with those on UK Gilts. I imagine that global bonds are still ahead of equities after 21 years.JohnWinder said:Thanks. Always feels instructive, but I get no more confident in what to do. I was complaining about equities going nowhere for 15 years in 1930's. You've shown global equities going nowhere for 12 years (did I read that right?), presumably with dividends reinvested, and presumably that graph is nominal values. If so, and there was inflation where you lived holding global equities, it was even longer than 12 years to recover.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards