We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

COPE reduction issue from SP

Comments

-

I think that has come up before when the starting amount is above the max and can be improved, sends the computer into a wobble.

You have commented on this in an earlier thread - https://forums.moneysavingexpert.com/discussion/comment/78367101/#Comment_78367101

0 -

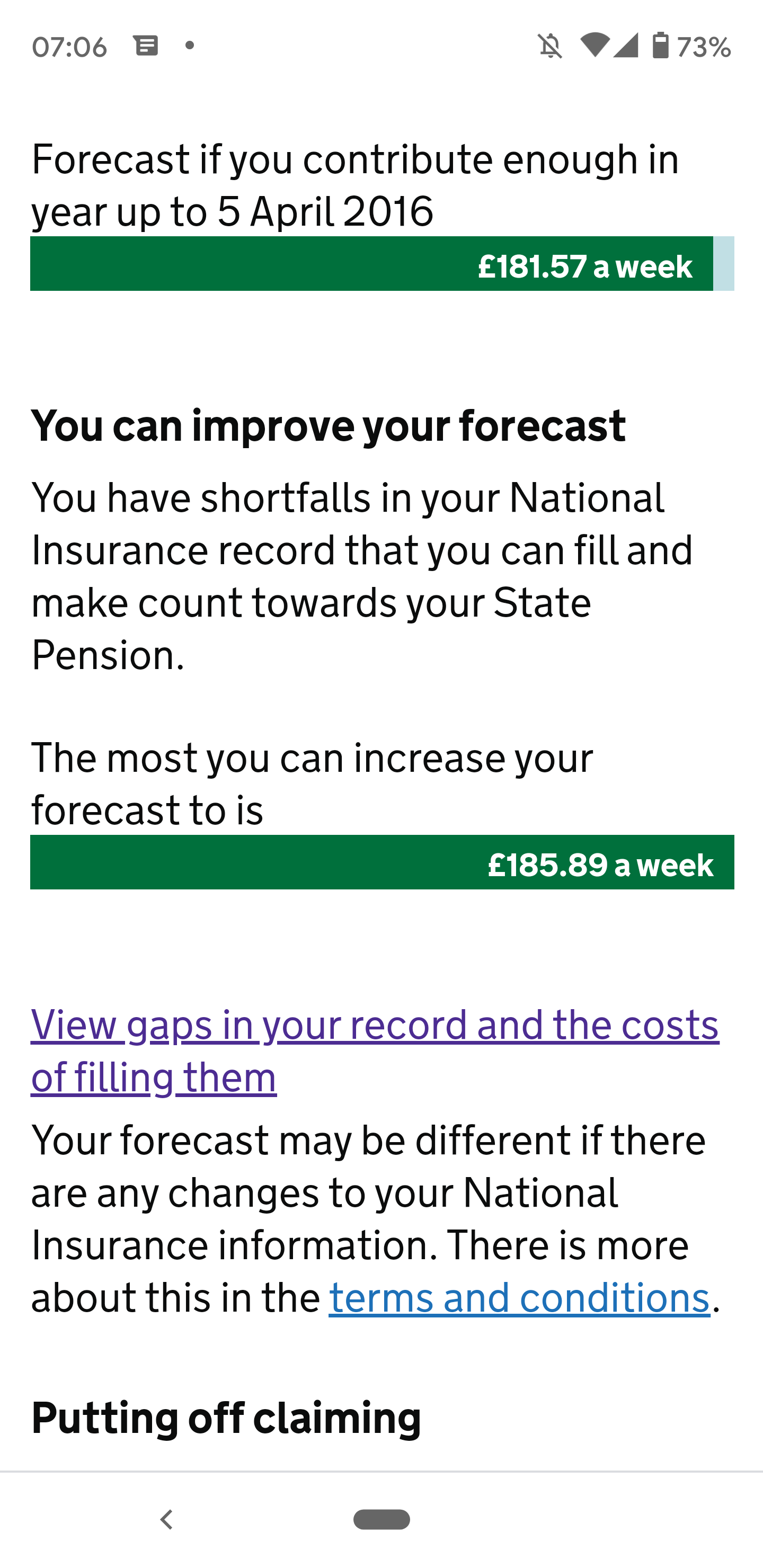

I have no idea why it mentions 2016, especially as it talks as though it's in the future. When I called them about that about three years ago, they couldn't explain it either.p00hsticks said:eastcorkram said:There is no mention of cope figure anywhere on state pension forecast.

I can improve it by buying one year . Why is it telling you what your forecast is up to 2016 ? It should be quoting up to your State Pension Age ?And why is it saying that you can improve your forecast when the estimate given until April 2021 is already over the new State Pension maximum amount ? The only way I can think of is if you have gaps in your record that you could make full......

Why is it telling you what your forecast is up to 2016 ? It should be quoting up to your State Pension Age ?And why is it saying that you can improve your forecast when the estimate given until April 2021 is already over the new State Pension maximum amount ? The only way I can think of is if you have gaps in your record that you could make full......

Yes, there are gaps. 16 years . Worked out of the UK. The last one of these was well over six years ago. Normally you can only go back six years. For some reason it's saying I can make up one year, and that I have until 2023 to do it.0 -

Well, there isn't much else.molerat said:Why is it telling you what your forecast is up to 2016 ? It should be quoting up to your State Pension Age ?Would be interesting seeing the rest, not just the top few lines.

Below that is just the bit about deferral . There is a link to view NI record. That shows me every year since 1976/77. If I click on view details, it shows how much NI was paid in each year. 0

Below that is just the bit about deferral . There is a link to view NI record. That shows me every year since 1976/77. If I click on view details, it shows how much NI was paid in each year. 0 -

If you "View the gaps in your record and the costs of filling them"........what does it say?Hopefully it should detail their view of the years you can make up, and tell you how much you'd have to pay to get that extra £4.32pw (£224pa).......0

-

I have no idea why it mentions 2016,

Have you read this?

https://forums.moneysavingexpert.com/discussion/comment/78367256/#Comment_78367256

And this link referenced in the above (produced for 2016 when NSP introduced)?

https://www.dpf.org.uk/explorer/files/TOPPING-UP-YOUR-STATE-PENSION-GUIDE.pdf

And with regard to the above, if you look at note 4 (bottom of page 14) you will see that even for those with more than 30 years in 2016, if they had fewer than thirty five years, in certain cases their position could be altered by paying voluntary NI.

And I think that you should also take note of what is said in your forecast above under "View gaps in your record" concerning changes in your NI information.

It seems to me that you must clarify with WTW whether or not you have a GMP for the years when you were in the RTZ scheme - see my post

https://forums.moneysavingexpert.com/discussion/comment/78507196/#Comment_78507196

which references what WTW said concerning DB occupational schemes.

Have you spoken to the Future Pensions Centre?

0 -

In the post your linking to there, which you made in May, you say that by 2016, I had less than 30 years (true, as I've only just got to 30), and that I must have been contracted in a lot and gained extra pension.xylophone said:I have no idea why it mentions 2016,Have you read this?

https://forums.moneysavingexpert.com/discussion/comment/78367256/#Comment_78367256

And this link referenced in the above (produced for 2016 when NSP introduced)?

https://www.dpf.org.uk/explorer/files/TOPPING-UP-YOUR-STATE-PENSION-GUIDE.pdf

And with regard to the above, if you look at note 4 (bottom of page 14) you will see that even for those with more than 30 years in 2016, if they had fewer than thirty five years, in certain cases their position could be altered by paying voluntary NI.

And I think that you should also take note of what is said in your forecast above under "View gaps in your record" concerning changes in your NI information.

It seems to me that you must clarify with WTW whether or not you have a GMP for the years when you were in the RTZ scheme - see my post

https://forums.moneysavingexpert.com/discussion/comment/78507196/#Comment_78507196

which references what WTW said concerning DB occupational schemes.

Have you spoken to the Future Pensions Centre?

You are also saying though, due to the scheme I was in , that I was contracted out.

They can't both be right.

I could ask WTW the direct question . They've been helpful with the info supplied this time. But.....I'm not sure why I'd chase it up. Surely I'd just be chasing the government and telling them to pay me less state pension?

About three years ago, I spoke to the future pensions centre. The person I spoke to, was unable to explain why that forecast looks the way it does.

I understand, I think, why I am allowed to buy that one extra year. But.......if, as you seem to think, and I probably agree, that the forecast is wrong, why would I believe the part about paying £800 or whatever, and getting the extra pension. I'd probably end up paying it, and not gaining anything.

Re the DB scheme. I can't really see a reason not to take it now. Unless ......taking it effects the amount I can pay per year into my current DC scheme?

I currently pay, well the employer does via sal sac, about £8000 a year into a SIPP.

I did ask WTW that, but they just seemed ignore that question.0 -

Getting the contracted in / out situation sorted needs attention sooner rather than later as there have been cases on here where a no COPE forecast was changed at SPA when they dug into the records at the final reconciliation exercise, back then a lot of records were on bits of paper and there were a few hiccups transferring them to computer. You need to ask WTW the simple question of was the RTZ pension contracted out and the same of DWP / HMRC. Your paperwork shows the pension scheme tax reference.eastcorkram said:In the post your linking to there, which you made in May, you say that by 2016, I had less than 30 years (true, as I've only just got to 30), and that I must have been contracted in a lot and gained extra pension.

You are also saying though, due to the scheme I was in , that I was contracted out.

They can't both be right. Depends on where you were working, you could be contracted out for x years with one employer then move jobs then be contracted in. Was the whole of your pre 2016 work history with RTZ ?

I could ask WTW the direct question . They've been helpful with the info supplied this time. But.....I'm not sure why I'd chase it up. Surely I'd just be chasing the government and telling them to pay me less state pension? These things often come to light when you reach state retirement age as they do a check of your records and old errors are found out so better now than later.

About three years ago, I spoke to the future pensions centre. The person I spoke to, was unable to explain why that forecast looks the way it does. Yours is one of those rare situations that the computer can't cope with putting on paper.

I understand, I think, why I am allowed to buy that one extra year. But.......if, as you seem to think, and I probably agree, that the forecast is wrong, why would I believe the part about paying £800 or whatever, and getting the extra pension. I'd probably end up paying it, and not gaining anything. You can buy the year simply because you have less than 30 pre 2016 years, topping up to 30 cannot fail to add value whether contracted in or out. If the number of years are correct then buying that year will increase the amount you receive even if they find you were contracted out and reduce the final total - if contracted out the S2P amount on the old scheme calculation will be reduced.

Re the DB scheme. I can't really see a reason not to take it now. Unless ......taking it effects the amount I can pay per year into my current DC scheme?

I currently pay, well the employer does via sal sac, about £8000 a year into a SIPP.

I did ask WTW that, but they just seemed ignore that question.

1 -

They can't both be right.

Yes, they can.

In my post I said

I am guessing that pre 6/4/2016, although you did not have 30 years NI, you had been contracted in for much of your career and so had accrued a fair amount of SERPS/S2P.You said in a later post in that same thread

I was working out of UK from 1990 to 2006 ish, Was never contracted out,Presumably you returned to UK in 2006 and started a job here. Contracting Out was possible up to 2012 for DC Schemes and up to 2016 for DB Schemes.

When you were with RTZ, you were unable to join the scheme for your first two years.

Were you contracted in then?

You then joined the RTZ DB Scheme - was it a contracted out scheme?

If it was (and I'd be astonished if it wasn't since the RTZ documentation you have received refers to those who have a GMP) then you were contracted out - see WTW note on this point.

You appear to have worked for employers other than RTZ which were contracted in.

Remember that at 6/4/16 (introduction of NSP), your whole NI history (contracted in/out) for all the years up to that point was taken into account in calculating your "starting amount" for NSP.

It is perfectly possible for a person to have been contracted in for some periods of their working life and contracted out for other periods.

When you reach SPA and claim your SP, it is likely that your NI history will be reviewed and any mistake come to light.

I would have thought it would be better for you to clarify your situation now.

And incidentally, if you were actually contracted out in the RTZ scheme, then this affects the way that your pension increases in deferment ( see your post here) are calculated

https://forums.moneysavingexpert.com/discussion/comment/78508302/#Comment_78508302

See https://www.barnett-waddingham.co.uk/comment-insight/blog/revaluation-for-early-leavers/

concerning revaluation of GMP/Excess for early leavers.

In addition to this, if you were contracted out, then once your RTZ pension comes into payment, after you have reached age 65 (GMP age which used to align with SPA but no longer does), then the scheme has no obligation to pay any increases on the part of your pension that relates to the GMP.

In your position, I would be clarifying the situation.

0 -

And you may find this worth a read

https://www.which.co.uk/news/2018/07/tens-of-thousands-could-see-cuts-to-their-state-pension/

0 -

eastcorkram said:Yes, there are gaps. 16 years . Worked out of the UK. The last one of these was well over six years ago. Normally you can only go back six years. For some reason it's saying I can make up one year, and that I have until 2023 to do it.At present you can go back to 2006 - the timescale was extended temporarily when the new State Pension was introduced in 2016 to give people a chance to make up years (as the rules were changed so that you needed a minimum of ten years to claim any pension).Whether the purchase of additional years (and which ones) will improve your forecast will depend on the exact details of the forecast, but previous posts suggest than purchasing one pre-2016 year would increase your predicted amount.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.5K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards