We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

COPE reduction issue from SP

Comments

-

What about the RTZ scheme that I was in? We've discussed this before on here. A DB scheme. My pension forecast has no cope figure , so they don't think I was contracted out.xylophone said:I was in a DB scheme in the early part of my career but I absolutely remember with clarity having an interview with the financial manager there who asked me to make a decision about opting out of SERPS and I categorically declined the opt out and signed to stay in despite it meaning my take home pay was lower as a result.I have never come across being able to opt out of contracting out if a member of a DB Scheme.

Are you saying that you refused membership of the scheme and have no entitlement to a pension from the scheme?

I clearly remember it being offered as a choice. I had no idea, or interest in it at the time (1980). But I was working with a guy in his fifties , and he advised me not to, even though I'd have paid a bit less NI. He didn't think it was a good idea. So I didn't opt out when I joined the scheme.0 -

I see it was discussed here

https://forums.moneysavingexpert.com/discussion/comment/78367626#Comment_78367626

Did you check with WTW on whether or not the Scheme was COSR?

And do you have your Statement of Deferred Benefits on leaving the Scheme?0 -

https://forums.moneysavingexpert.com/discussion/comment/78367626#Comment_78367626Right. I've received all the transfer paperwork.WTW have confirmed that you do have a GMP?

This does not give a figure of what I'd receive at 65, so presumably I need to assume the figures I gave at the start of the thread. It does give, pension at date of leaving. I left the fund in Nov 1990.

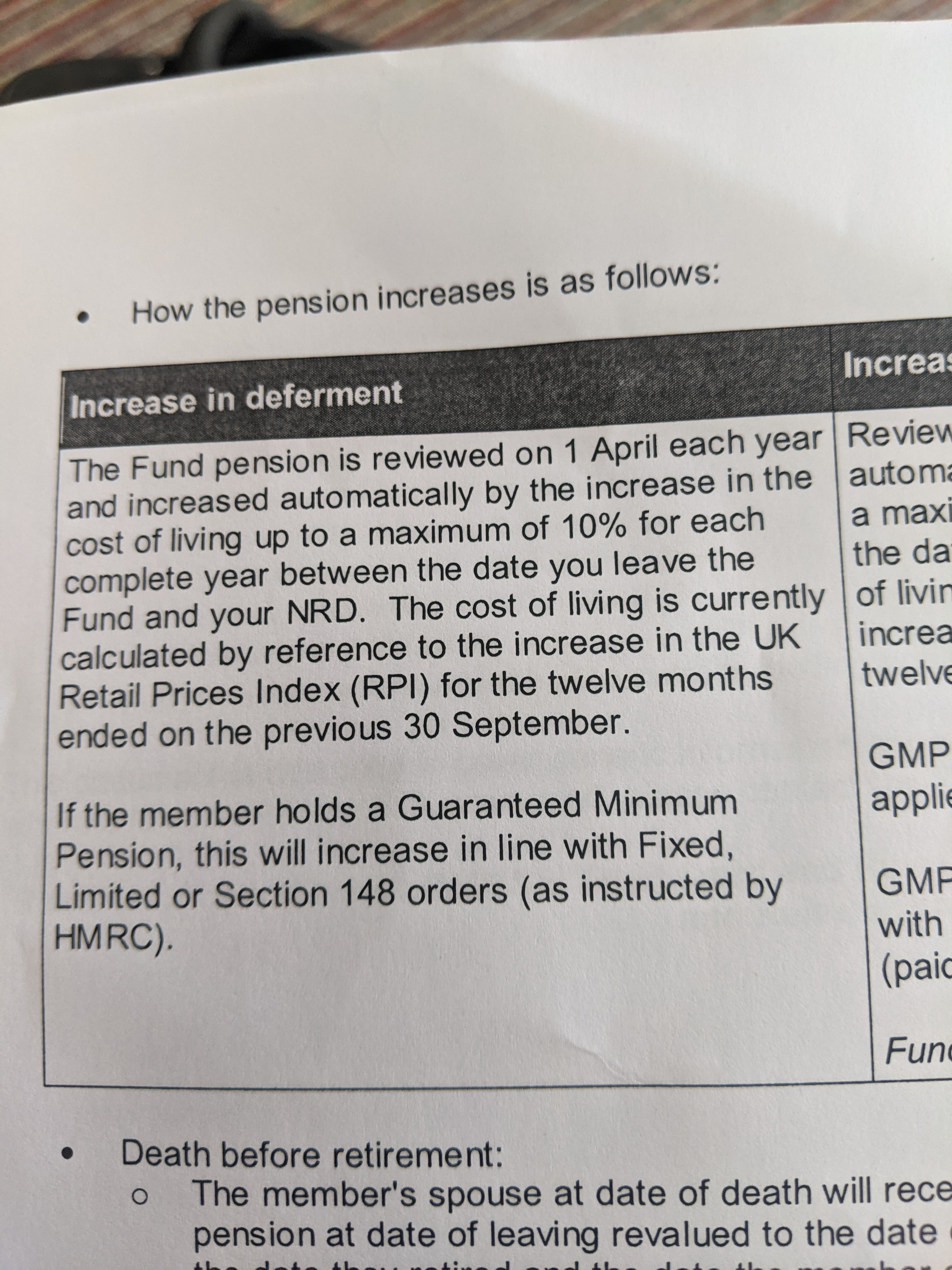

Fund pension built up before 6 April 1997 £979.34 a year.

Offset pension payable to age 65 £677.29 a year.

Guaranteed transfer value £70,025.00

GMP age is 65.

If so, you should have a COPE.

0 -

And come to think of it, why should the statement from WTW mention 6/4/97 unless the scheme had been contracted out?

https://www.willistowerswatson.com/en-GB/Insights/2019/02/questions-you-are-too-afraid-to-ask-about-gmp-equalisation

If a scheme was contracted out, some or all of a member’s pension accrued between 6 April 1978 and 5 April 1997 will be made up of GMP.

Have you checked the second page of your state pension statement for a COPE?0 -

Just home after a five hour drive. Will check latest info. I asked WTW, several questions. They've answered them some of them in an email, and some further info on its way in the post apparently. Will re read this, but don't think there's any mention of GMP.

Will check forecast again tomorrow, but pretty sure there is no cope.

Will get back .1 -

It will be interesting to know the answer - it would be very unusual for the occupational pension scheme of a firm like RTZ not to have contracted out - there was a saving to the company as well as to the employee.

And it was the scheme that was contracted out so that join the scheme and contracting out was automatic.

No doubt WTW can clear this up.

You will note in the WTW link cited above

For a defined benefit occupational pension scheme, it was not possible to contract out on a member-by-member basis. Schemes either needed to have all members contracted out or have all members “contracted in” – i.e. all members received the additional state pension as well as scheme benefits.

0 -

As this thread seems quiet , I may as well derail it further.

There is no mention of cope figure anywhere on state pension forecast.

I can improve it by buying one year .

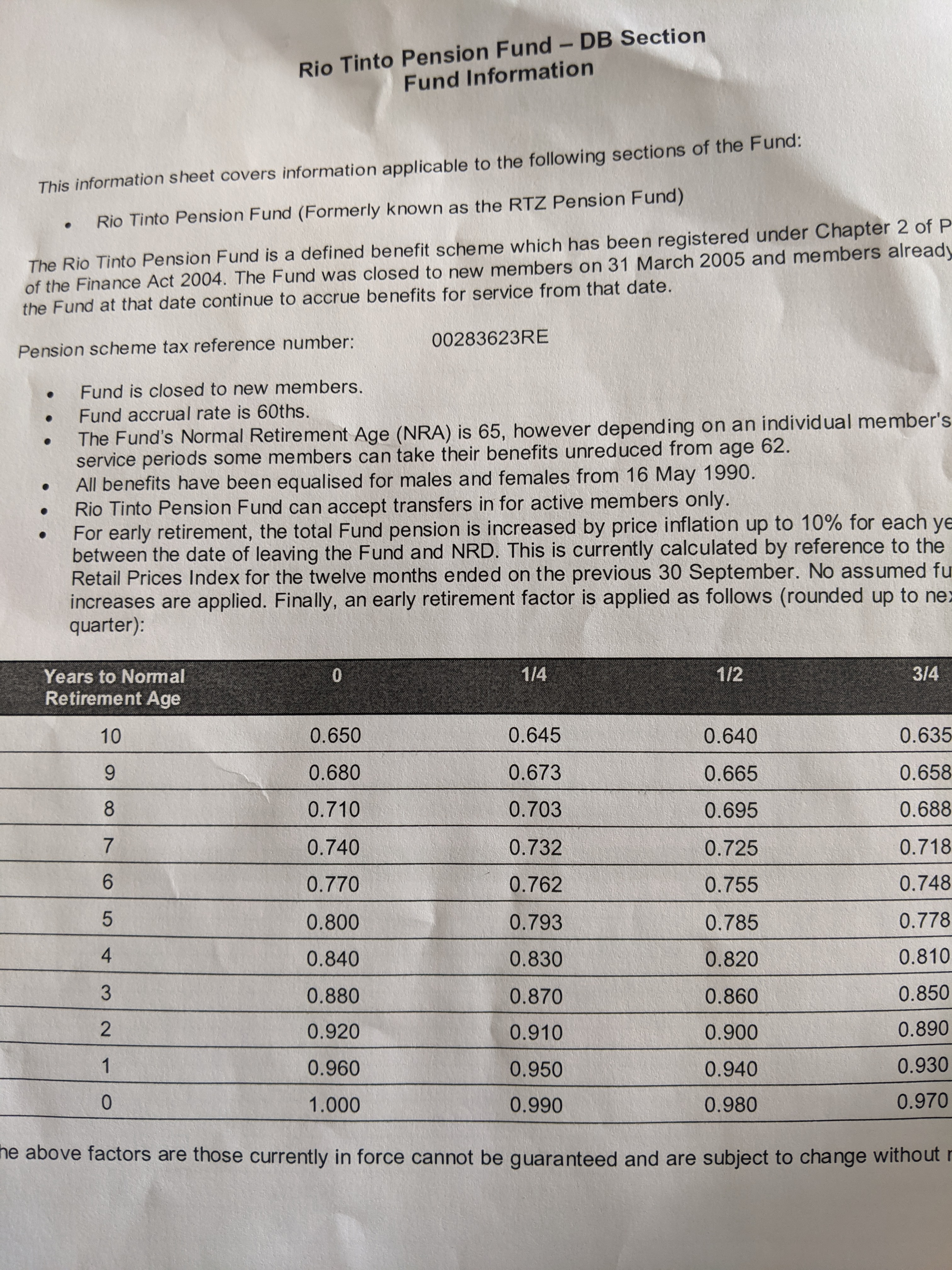

WTW sent me some info. It does mention GMP, but doesn't say if I have this.There is a letter still on its way . They sent figures for taking it early. Normal is 65. If I'm understanding it correctly, if I take it at 62, ( later this year), do I get 88% of the pension ?

0

0 -

Re your state pension forecast

This was discussed here

https://forums.moneysavingexpert.com/discussion/comment/78367256/#Comment_78367256

With regard to the lack of a COPE, this is very odd if you do indeed have a GMP - you will need to clarify with WTW and if you do have a GMP, you should contact DWP to discuss the absence of a COPE.

Presumably you are not in the position of a member who may draw an unreduced pension at age 62 - therefore the pension would be increased from date of leaving as indicated in your paperwork and then an actuarial reduction applied.

However, was there not also a mention of a bridging pension payable up to age 65?0 -

eastcorkram said:There is no mention of cope figure anywhere on state pension forecast.

I can improve it by buying one year .This forecast really doesn't make sense to me - I know in the past we've had a few examples of weird outlier conditions that have caused the forecast programming to go a bit skew.Why is it telling you what your forecast is up to 2016 ? It should be quoting up to your State Pension Age ?And why is it saying that you can improve your forecast when the estimate given until April 2021 is already over the new State Pension maximum amount ? The only way I can think of is if you have gaps in your record that you could make full......0 -

Why is it telling you what your forecast is up to 2016 ? It should be quoting up to your State Pension Age ?

I think that has come up before when the starting amount is above the max and can be improved, sends the computer into a wobble.

Would be interesting seeing the rest, not just the top few lines.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.5K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards