We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

FIREside Chats

Comments

-

I'm avoiding the life style options - and going 100% equities currently as I don't trust bonds - and I'm lucky enough to have 2 DB pensions and so will have a predictable base. I think @SouthCoast if you have 4 pension pots I'd be tempted to have a different strategy for different ones or as others have said perhaps combine them to reduce fees and then decide what level of bonds you are comfortable with. I think what stands out to me on bonds is they are a debt instrument and as such there is always a risk that the person/organisation/nation goes bust and defaults...Achieve FIRE/Mortgage Neutrality in 2030

1) MFW Nov 21 £202K now £166.7K Equity 38.23% 12/7/26

2) £1.8K Net savings after CCs 14/7/26 (but owed £450) so £2.2K

3) Mortgage neutral by 06/30 (AVC £44.2K + Lump Sums DB £4.6K + (25% of SIPP 1.7K) = 50.5K of £127.5K target 39.6% July 26 (If took bigger lump sum = 72.4K or 56.8%)

4) FI Age 60 income target min £17.1/30K 57% (may need more) If bigger lump sum £15.8/30K 52.67%

5) SIPP £5.7K updated 29/5/261 -

OK, yes I see why that makes sense 👍 May just use it to spend more those years though, as I'm hoping to still be sprightly at 60 😀hugheskevi said:Wouldn't you continue the pension withdrawals up to the tax-free amount (£16,760 p/a if using UFPLS with standard tax coding) and put the money into an ISA rather than pausing withdrawals once the LISA is accessible? That would enable greater extraction at a favourable tax rate.

Please can someone explain how the £16,760 figure works? I've heard this suggested before and one minute I think I understand it, then the next minute I'm not sure I do! I thought you could only have the tax benefit once, ie on the lump sum, or 25% of each withdrawal? SL, you seem to be suggesting your husband took a 25% lump, then 25% of each further withdrawal was also tax-free?

NI is on track, I have 3 incomplete years but they date back to when I was at Uni (2002-2006), so too long ago to do anything about. I need another 11 years including this one, which will take me to 52 and is my target date. I'd like to ideally spend the last few years doing something part-time and easy rather than what I do now, but not on course for that at the moment. That may change though, if market conditions are favourable for the next few years!

I've never really seen the appeal of combining the pensions, unless I am missing something? In my head, I've always thought keeping them separate would give me flexibility if I wanted to use them in different ways, as I don't think you can "part-do" something with one big pot? I'll double-check the fees I'm paying, but from memory I think they're OK. Also, if I leave some segregated and doing their lifestyling thing rather than fiddling, that should at least give some protection from me b*ggering it up, as Ed has (much more eloquently!) suggested.

None of this helps with the fact the money will be accessible at least 5 years too late though, which is why I always mentally favour ISA over pension/LISA 🤔Mortgage start: £65,495 (March 2016)

Cleared 🧚♀️🧚♀️🧚♀️!!! In 5 years, 1 month and 29 days

Total amount repaid: £72,307.03. £1.10 repaid for every £1.00 borrowed

Finally earning interest instead of paying it!!!3 -

You can choose how you want to take the lump sum (subject to your scheme(s) offering all options). You can either take the full 25% up-front, and then all of future withdrawals are taxable. Or, you can take 25% tax free as part of each individual withdrawal.South_coast said:Please can someone explain how the £16,760 figure works? I've heard this suggested before and one minute I think I understand it, then the next minute I'm not sure I do! I thought you could only have the tax benefit once, ie on the lump sum, or 25% of each withdrawal? SL, you seem to be suggesting your husband took a 25% lump, then 25% of each further withdrawal was also tax-free?

The Personal Allowance is £12,570 and £12,570 / 0.75 = £16,760. If you withdraw £16,760 each year with 25% tax free then the remaining taxable 75% fully uses Personal Allowance. So a couple could draw £33,520 completely tax free.

If you can engineer debt to fund age 52-57, with pensions in place to repay the debt that can be very tax efficient. Typically that would involve a mortgage.South_coast said:None of this helps with the fact the money will be accessible at least 5 years too late though, which is why I always mentally favour ISA over pension/LISA 🤔

4 -

OK, I still can't get the maths to add up, but I think I at least grasp the concept now 😅*

I did have a slightly mad idea the other day of doing my 52-57 spending on 0% cards, then repaying via the pension. Can foresee a number of pitfalls with that idea though! It does reinforce my thinking to just keep the pension to the minimum contributions, carry on with the LISA as it feels like a good deal (and is "only" £4k a year from me - and only for another 8 more years), but then put everything else into the ISA

* Edited to add: Ohhhhh, now I get it 🤦♀️! £12,570 is 75% of £16,760 - so I withdraw £16,760, of which £4,190 is the tax-free 25%, and £12,570 is taxable, but is the personal allowance so I don't pay tax on it. Got it! Brain was thinking along those lines, but I was working it out the other way round, hence why it wasn't adding up!Mortgage start: £65,495 (March 2016)

Cleared 🧚♀️🧚♀️🧚♀️!!! In 5 years, 1 month and 29 days

Total amount repaid: £72,307.03. £1.10 repaid for every £1.00 borrowed

Finally earning interest instead of paying it!!!6 -

The principle of spending on 0% cards is perfect, but the problem is that even at the point of retirement you couldn't guarantee being able to roll-over debt on the cards. I've been doing that for many years now, but you always have to assume that you will have to repay the card at the end of the debt, and that only changes once you have successfully transferred the balance.South_coast said:I did have a slightly mad idea the other day of doing my 52-57 spending on 0% cards, then repaying via the pension. Can foresee a number of pitfalls with that idea though! It does reinforce my thinking to just keep the pension to the minimum contributions, carry on with the LISA as it feels like a good deal (and is "only" £4k a year from me - and only for another 8 more years), but then put everything else into the ISA

For these reasons, I've only used 0% spending and 0%, fee-free balance transfers cards as a way to accelerate my financial plans, bringing forward investing whilst keeping enough in savings to meet repayments if necessary, and only releasing funds into investments once new 0% deals are in place. It is surprisingly lucrative when compounded over many years. I haven't kept records, but I suspect that over the years this has probably been worth getting on for about £100,000 to my wife and I.

In practice, the only borrowing you are likely to be able to keep in place for many years at a reasonable interest rate is a mortgage or perhaps a long-term personal loan.6 -

An update on our own position, following the last update I did on this thread back on 13th January.

My wife and I returned from 16 months of travel through the Americas in January, and are now back living in London in the house we lived in prior to travel and back at our old jobs. We are both aged 46. Our plan is to move to the north-west of England, Shrewsbury, or north-east Wales at some point over the next year and retire then or very soon afterwards.

I'm very pleased with the decision to come back and work for a while - after over 3 months back in our house I am only just getting around to listing all the things I want to do before selling the house as there has been a lot to organise after spending so long away traveling. I'm not doing anything major, so expect to be done by the end of the summer.

Plan A will be to market our house in February, which is the most popular time of the year in my area. However, I'm monitoring areas I would like to live and now have a good idea of the places we would like. Should an ideal property come onto the market I'd move to buy that immediately. There would be various options for that, and there are pros and cons attached to each one, so I don't have a clear preference and will judge which to use depending on the particular circumstances at the time.- Sell London house and move as part of a chain; or

- Purchase with offset mortgage, and separately sell London house and use proceeds to fully offset mortgage; or

- Move all ISAs into flexible ISAs and use that along with selling Premium Bonds to purchase property, separately selling London property to replenish ISAs and Premium Bonds (assuming completion happens with sufficient time to sell London house in the same tax year)

For the period from when we leave work (probably age 47) to age 55 we will rely on cash savings, Premium Bonds, cash ISAs, and finally investment ISAs. This could be supplemented or reduced by our house sale, depending on the value of our new property compared to our current property.

Our non-pension balance sheet is:- £540,000 House (no mortgage)

- £330,000 Investment ISA

- £145,000 cash/cash-like assets, net of all debts (mostly cash-ISAs and Premium Bonds)

- £57,500 gross annual income (£51,000 net if our only income) - DB from age 55 (protected minimum pension ages and taking account of actuarial reductions)

- £1,000 gross annual income - DB from age 57

- £23,000 gross annual income from State Pensions

- £270,000 DC pension (effectively replaces State Pension for period between age 55 and State Pension age)

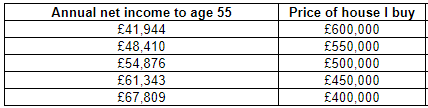

Having researched properties, I expect to buy somewhere costing between £400,000 to £600,000. Anything more expensive than that is just too big, and anything below £400,000 always has a few too many things I don't like. As at today, the trade-off between annual income prior to age 55 and the price of the house I buy is:

As an idea of the sort of property at each end of the scale, based on properties currently available, toward the upper end this property is what I would choose, whilst at the lower end this property would be a nice choice. We want to live semi-rurally, having lots of good options very close-by for taking dogs on long walks, but also living close enough to things like swimming pools and gyms and running clubs, and not too far from bigger towns/cities.

We are already in a place where I'd be happy to retire, even though our pre-55 income would be a bit lower than our post-55 income. We don't spend very much (our main interests being dogs, animals generally, running, and music, and we cycle to work so minimal commuting costs), I'd estimate around £35,000 - £40,000 p/a (I would know precisely, but as we have been away traveling I won't have a full year of data until April 2025). So by the time we have bought somewhere and moved and quit jobs it should all be very comfortable.

As an aside, I'd really encourage anyone to keep their own spreadsheets for retirement planning - you can do so much with nothing very complicated and just build them up over time. It is extremely reassuring to have comprehensive financial details to plan around, and has been so helpful to me over the years in balancing decisions about where to save, what to invest it, etc, to take best advantage of tax relief and other incentives.

8 -

Sorry for the confusion. DH did indeed take the full 25% TFLS in one go.South_coast said:

SL, you seem to be suggesting your husband took a 25% lump, then 25% of each further withdrawal was also tax-free?hugheskevi said:Wouldn't you continue the pension withdrawals up to the tax-free amount (£16,760 p/a if using UFPLS with standard tax coding) and put the money into an ISA rather than pausing withdrawals once the LISA is accessible? That would enable greater extraction at a favourable tax rate.

Then the drawdown of the funds over the four complete financial years between stopping work two months before he was 61 and the April before the tax year in which he reaches state pension age (2024 5 April as he will be 66 in November) were taken as 25% of the total in year 1, 33% of the remainder in year 2, half the remainder in year 3, and then the remainder in year 4.

Because his other income in that period was a DB pension that is lower than the PAYE taxable threshold, a proportion of the DC lump sums he drew down were each tax free, up to that limit. We avoided paying tax on all of the drawdown years because we waited until the tax year after he finished work, and finished before this year, in which he will get his state pension, all being well.Save £12k in 2026 #2 I have banked £9004.48 so far, against a £10k target The 2026 Save £12k in 2026 thread is here

OS Grocery Challenge in 2026 I am sticking with a £3000 annual budget for 2026 - currently £1111.79 and most of my May purchasing made

I also Reverse Meal Plan on that thread and grow much of our own premium price fruit and veg, joining in on the grow your own in 2026 discussion thread

My keep within our budget diary is here5 -

Circling back to say Hi to FIRE-siders with a brief updateTo recap, everything was on course for age 60 retirement but a few spanners in the works derailed that - USS pension changes, cost of living, job misery, DH made redundant. I'm closing in on 56 yo soon, changed jobs, we have relocated to a new house slightly closer to work (<1 hour commute) avoiding a new mortgage (so still happily mortgage free) and daughter starting third year of uni in September. No greenhouse here though :'(While much of the uncertainty of last year has settled, the FIRE plan is still hard to pin down. In past I have relished a good spreadsheet but, for some reason (maybe gloominess?), I cannot bring myself to get all the financial planning laid out in a new spreadsheet. It feels a bit too complicated? The complications...The new job is a huge improvement in many ways. It also needed a decision - continue adding to USS pension or join the TPS. The latter is all DB. I took the plunge and stopped the USS payments and became a new member for TPS, signing up for faster accrual rate which is additional voluntary contributions from salary before tax. Instead of going into the DC part of the USS pension, it adds to the DB of TPS. This seemed like a no brainer move, I hope I fathomed that all out correctly. It all made my head hurt. It's done now. There's three parts to the USS pension and that makes my head hurt too - some final salary, some on one set of rules and some on another. The years before penalties kick in for early retirement also seem to vary for each bit?! This is almost certainly part of why I find the prospect of pinning it all down into a spreadsheet an overwhelming task.I stopped paying into the VG lifestyle SIPP throughout all this upheaval. Now that we are settled in the new place, I maybe ought to have a rethink. I haven't paid anything into an ISA this year either. I fear I've run off the FIRE rails

There's lots to do in the new home too - we bought it as a project. Fantastic view of the nearby estuary and an iconic bridge. We'll need pennies for all the things we would like to do - currently fretting about our carpetright purchase of £7k. DH has been doing a fantastic job on house DIY improvements, saving us loads of money and making his being out of work a positive thing for now. He does need to get back into the workforce though. For wellbeing/MH, we must have a greenhouse, would like to have raised veggie plot beds too. I know that I should cost these and make a savings plan, but again, I have spreadsheet brain freeze.Does anyone have recommendations for a good book on setting priorities/planning/spreadsheeting approaches or sites that might inspire?ElmoR xx2

There's lots to do in the new home too - we bought it as a project. Fantastic view of the nearby estuary and an iconic bridge. We'll need pennies for all the things we would like to do - currently fretting about our carpetright purchase of £7k. DH has been doing a fantastic job on house DIY improvements, saving us loads of money and making his being out of work a positive thing for now. He does need to get back into the workforce though. For wellbeing/MH, we must have a greenhouse, would like to have raised veggie plot beds too. I know that I should cost these and make a savings plan, but again, I have spreadsheet brain freeze.Does anyone have recommendations for a good book on setting priorities/planning/spreadsheeting approaches or sites that might inspire?ElmoR xx2 -

Hi @ElmoR,

I saw your post and it resonated with me, I think we could be in a similar place. I too am in the USS and as I entered HE after an earlier career I have several different pensions, some DB and some DC. It took me a while, but I finally consolidated everything this year in the USS DC part. I have built many spreadsheets over the years but recently came across a free website guiide.co.uk. It helps you to model your pension income in retirement. I find it useful because it helps to simplify what is a very complex set of decisions and variables. I find the difficulty is fixing for example when I want to retire and then the desired income in retirement. But it has been useful because it kind of indicates what is realistic and so it has helped me to realise that for me the realistic target is probably 59 or 60. I hope you might find it useful.

Going on sabbatical August 31st 2026.4 -

Hi @ElmoR, I would just check if your USS pension is going to increase by an indexation rate now you have stopped paying in (and what that is) - then maybe check with the TPS whether all or any could be transferred in (used to be within a year but stuff changes) - worth checking which works better (of course reserved rights for USS might mean a lower scheme pension age, whereas TPS new entrants aligns with SPA, I believe)Save £12k in 2026 #2 I have banked £9004.48 so far, against a £10k target The 2026 Save £12k in 2026 thread is here

OS Grocery Challenge in 2026 I am sticking with a £3000 annual budget for 2026 - currently £1111.79 and most of my May purchasing made

I also Reverse Meal Plan on that thread and grow much of our own premium price fruit and veg, joining in on the grow your own in 2026 discussion thread

My keep within our budget diary is here2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards