We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

PLEASE READ BEFORE POSTING: Hello Forumites! In order to help keep the Forum a useful, safe and friendly place for our users, discussions around non-MoneySaving matters are not permitted per the Forum rules. While we understand that mentioning house prices may sometimes be relevant to a user's specific MoneySaving situation, we ask that you please avoid veering into broad, general debates about the market, the economy and politics, as these can unfortunately lead to abusive or hateful behaviour. Threads that are found to have derailed into wider discussions may be removed. Users who repeatedly disregard this may have their Forum account banned. Please also avoid posting personally identifiable information, including links to your own online property listing which may reveal your address. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Cant sell my flat due to being under 30sqm

Comments

-

Thank you for this. After writting this i actually called my bank for advise as they were the ones who gave me the morgage in the first place.LAD917 said:Can you or your agent speak to a mortgage broker, understand what lenders will loan on the property, and then proactively steer buyers to those lenders? When I've sold properties with "issues" (not this issue in particular), I've worked with agents to provide buyers with solutions / steer them to the path of least resistance.

They said they would still give me a morgage. They advised exactly what you have just said.

So before a buyer puts in an offer they need to check this out.

Its going to make it harder to sell but at least i dont keep getting people put in offers only to find a month later they cant get a morgage1 -

Unfortunately land is at a premium in the uk. Its a small island which is overcroweded.Wanderingpomm said:

It’s not a silly rule. Accommodation is getting smaller and smaller. People should respect the minimum space requirements. Bedsits used to have a separate kitchen. Sleeping next to where you cook is a recent thing driven by people trying to make as much money as possibleLeeannero1 said:

Yes its still mortgageable with limited lenders ive been told. However my buyer has pulled out as she thinks she won't be able to sell it on in the future, and she is most probably right.deannagone said:You managed to get a mortgage on it in 2019 so it was clearly mortageable then. It may be with more limited lenders now, it may not. But no one could foresee that at the time.., especially as you did get a mortgage yourself.

Its just 2 buyers have now pulled out and it makes selling my home even more difficult. I really hope someone who wants to buy can get a lender. it just seems such a silly rule.

0 -

This has crossed my mind actually. It could be an option.Armorica said:OP - speak to the estate agent selling your neighbours flat - find out if they've had much interest, and try to explore if you might both have more luck if you join forces to find a cash buyer to buy both flats. I assume it's an older building that used to be a single property and so there might be interest is having two close together, or reconverting back into a single thing. (Subject to complex navigation of planning rules!)0 -

No its been great, i have fields hills and woods around me.GDB2222 said:It's a bit small to spend lockdown, if there's no outside space.2 -

You guessed it: upsizing lolTitus_Wadd said:OP, just being curious, why are you selling?1 -

I think this is one case of a general principle: Things beyond your control could make your property worth a lot less. It was always a risk, sometimes bigger than others.To be honest I think any flat owner nowadays should count themselves lucky if they're not affected by the fire safety scandals.Yours will sell, just probably not for the money you were hoping for. If you're in negative equity selling will be a problem though.1

-

No, not really.Leeannero1 said:

Unfortunately land is at a premium in the uk. Its a small island which is overcroweded.Wanderingpomm said:

It’s not a silly rule. Accommodation is getting smaller and smaller. People should respect the minimum space requirements. Bedsits used to have a separate kitchen. Sleeping next to where you cook is a recent thing driven by people trying to make as much money as possibleLeeannero1 said:

Yes its still mortgageable with limited lenders ive been told. However my buyer has pulled out as she thinks she won't be able to sell it on in the future, and she is most probably right.deannagone said:You managed to get a mortgage on it in 2019 so it was clearly mortageable then. It may be with more limited lenders now, it may not. But no one could foresee that at the time.., especially as you did get a mortgage yourself.

Its just 2 buyers have now pulled out and it makes selling my home even more difficult. I really hope someone who wants to buy can get a lender. it just seems such a silly rule.

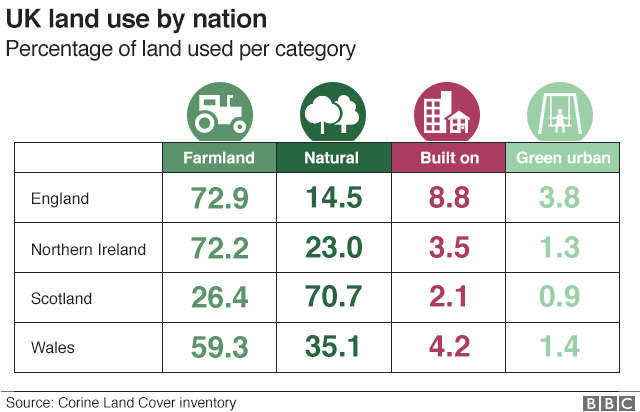

0.1% of the UK is "continuous urban fabric", where 80-100% of the land is built on.

5.3% of the UK is "discontinuous urban fabric", where 50-80% of the land is built on.

Just 1.4% of the UK is covered by buildings, 2% in England. More land sits between the low and high tide lines around the coast and along tidal rivers.

11% of the country is peat bog...

We just think it's a lot higher, because so many of us actively WANT to live in the corner that's most built-on. The South East...

Put your postcode into this to find the split in your local authority area...

https://www.bbc.co.uk/news/uk-41901294

8 -

That’s great that you have been able to get out. Can I ask whether you worked from home during lockdown?Leeannero1 said:

No its been great, i have fields hills and woods around me.GDB2222 said:It's a bit small to spend lockdown, if there's no outside space.

I think it’s worth thinking about, because a lot of people got quite a jolt when lockdown started, and they were spending 23 hours out of 24 in the same place.My niece and her husband have abandoned their small central London flat and moved in with her parents, out in the suburbs. They were getting on top of each other working from home in the flat.No reliance should be placed on the above! Absolutely none, do you hear?0 -

My flats been reasonable priced and has had an offer of the asking price and not far off the asking price, so i dont think that will be the problem for me.A_Lert said:I think this is one case of a general principle: Things beyond your control could make your property worth a lot less. It was always a risk, sometimes bigger than others.To be honest I think any flat owner nowadays should count themselves lucky if they're not affected by the fire safety scandals.Yours will sell, just probably not for the money you were hoping for. If you're in negative equity selling will be a problem though.0 -

What part do you find confusing? I said it’s harder in the US than in the UK where mortgages are regulated. Additionally I said, more regulation that tie it in with planning approved and building control approval which guarantee a mortgage as long as the property is in a fit state won’t result in this problem OP faces.Billy_B_North said:

Rubbish.Alan2020 said:

Residential mortgages are a regulated product and banks themselves are regulated. They cannot do as they please. Ultimately the property has zero value because someone said you cannot rent and the banks decided not to offer a mortgage. Both are wrong.Billy_B_North said:

That’s ludicrous.

Banks can choose who they lend to, and at what rate. It is their shareholder’s capital at risk, and no-one is going to force them to lend against poor security?

You forget that banks are not a utility, they are not a public service, they are businesses who exist to make a profit.You do realise I am talking of the UK here, which is for all intents and purposes a socialist country. We both cannot just open a bank or start a lottery or even sell shares to the public or even evict people for not paying rent. Banks have to toe the socialist line, tax is collected and social security paid to the needy and the not so needy. A visit to the US will quickly enlighten you about how certain businesses are expected to behave in the UK.

No-one’s going to force a bank to lend against a property that they don’t want to, and having worked in banking in both the US and the UK I have to wonder where you are getting this from.

I don’t think that this is the thread for you to post your uninformed flights of fancy.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards