We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Prevent Halifax regular saver renewal online - but how?

Comments

-

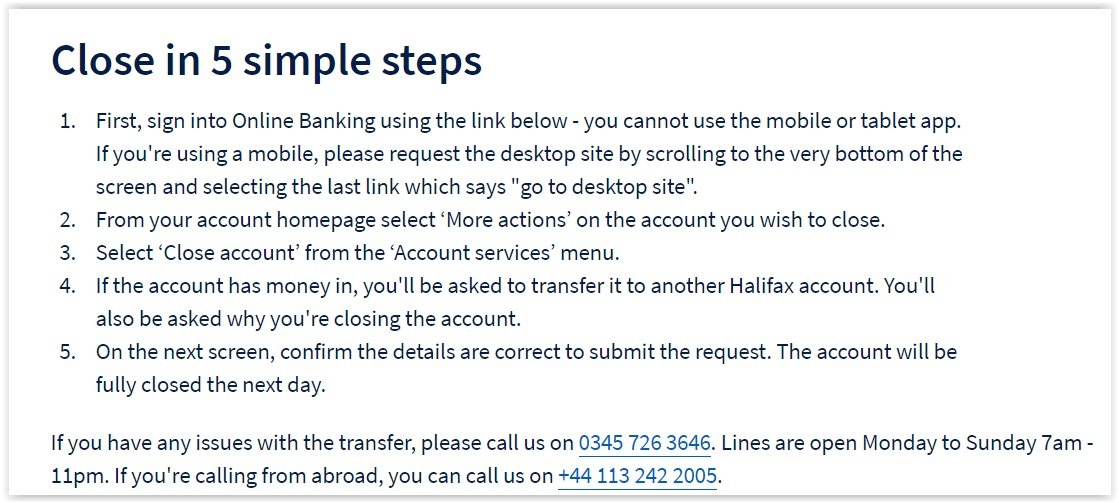

You will have to use online banking to do itsurreysaver said:

I cannot see how to close an account in the Halifax or BoS appMDMD said:You also need to close the everyday saver account they have opened. That way the old account will be converted into a new everyday saver rather than roll round into a new RS.

2 -

Cheers. Just done it on the laptop. Because next tax year I'll be earning over the personal savings allowance, I want to wait until the new tax year before renewing recently matured Regular Savers at 1% so they don't mature until the 2022/3 tax year. My Halifax and TSB mature shortly, and HSBC did last weekcolsten said:

You will have to use online banking to do itsurreysaver said:

I cannot see how to close an account in the Halifax or BoS appMDMD said:You also need to close the everyday saver account they have opened. That way the old account will be converted into a new everyday saver rather than roll round into a new RS.I consider myself to be a male feminist. Is that allowed?0 -

Just been looking at my accounts with Halifax and BOS, following the above info I can close my every day saver online but not my Halifax regular saver but I can close my monthly saver with BOS which is all on the same page.colsten said:

You will have to use online banking to do itsurreysaver said:

I cannot see how to close an account in the Halifax or BoS appMDMD said:You also need to close the everyday saver account they have opened. That way the old account will be converted into a new everyday saver rather than roll round into a new RS.

Is that not strange?I choose the rooms that I live in with care,

The windows are small and the walls almost bare,

There's only one bed and there's only one prayer;

I listen all night for your step on the stair.0 -

The BoS and Halifax Monthly/Regular Savers have different T&Cs. I believe you can close the BoS one early, but not the Halifaxtrickydicky14 said:

Just been looking at my accounts with Halifax and BOS, following the above info I can close my every day saver online but not my Halifax regular saver but I can close my monthly saver with BOS which is all on the same page.colsten said:

You will have to use online banking to do itsurreysaver said:

I cannot see how to close an account in the Halifax or BoS appMDMD said:You also need to close the everyday saver account they have opened. That way the old account will be converted into a new everyday saver rather than roll round into a new RS.

Is that not strange?

Edit - having just checked, you can withdraw money from the BoS one, but not the HalifaxI consider myself to be a male feminist. Is that allowed?1 -

You can close the Halifax Regular Saver early. I have done it. To close it online you need to "renew" it as an Easy Access Saver and then you can close that.surreysaver said:

The BoS and Halifax Monthly/Regular Savers have different T&Cs. I believe you can close the BoS one early, but not the Halifaxtrickydicky14 said:

Just been looking at my accounts with Halifax and BOS, following the above info I can close my every day saver online but not my Halifax regular saver but I can close my monthly saver with BOS which is all on the same page.colsten said:

You will have to use online banking to do itsurreysaver said:

I cannot see how to close an account in the Halifax or BoS appMDMD said:You also need to close the everyday saver account they have opened. That way the old account will be converted into a new everyday saver rather than roll round into a new RS.

Is that not strange?

Edit - having just checked, you can withdraw money from the BoS one, but not the Halifax

Retired 1st July 2021.

This is not investment advice.

Your money may go "down and up and down and up and down and up and down ... down and up and down and up and down and up and down ... I got all tricked up and came up to this thing, lookin' so fire hot, a twenty out of ten..."1 -

Whilst many will have valid reasons for closing a maturing Halifax Regular Saver, there are reasons to renew it. If you have maxed out any better rates (these are fast disappearing), 1% fixed is not bad, you do not need an associated current account, your first deposit can be £25 and you can miss monthly paying ins with no penalty and be ready to fund again if other rates fall further.

1 -

quirkydeptless said:

You can close the Halifax Regular Saver early. I have done it. To close it online you need to "renew" it as an Easy Access Saver and then you can close that.surreysaver said:

The BoS and Halifax Monthly/Regular Savers have different T&Cs. I believe you can close the BoS one early, but not the Halifaxtrickydicky14 said:

Just been looking at my accounts with Halifax and BOS, following the above info I can close my every day saver online but not my Halifax regular saver but I can close my monthly saver with BOS which is all on the same page.colsten said:

You will have to use online banking to do itsurreysaver said:

I cannot see how to close an account in the Halifax or BoS appMDMD said:You also need to close the everyday saver account they have opened. That way the old account will be converted into a new everyday saver rather than roll round into a new RS.

Is that not strange?

Edit - having just checked, you can withdraw money from the BoS one, but not the HalifaxOk, so I have a regular saver still paying the old rate of 2% due to mature soon.

Obviously, I want this to go full term to get the most back.

So, are you saying allow it to mature and get moved to an easy access saver but cancel the SO and then convert the new regular saver as you described to an easy access saver?

Then delete both easy access savers, this is getting complicated.

I choose the rooms that I live in with care,

The windows are small and the walls almost bare,

There's only one bed and there's only one prayer;

I listen all night for your step on the stair.0 -

To get the max benefit you need totrickydicky14 said:quirkydeptless said:

You can close the Halifax Regular Saver early. I have done it. To close it online you need to "renew" it as an Easy Access Saver and then you can close that.surreysaver said:

The BoS and Halifax Monthly/Regular Savers have different T&Cs. I believe you can close the BoS one early, but not the Halifaxtrickydicky14 said:

Just been looking at my accounts with Halifax and BOS, following the above info I can close my every day saver online but not my Halifax regular saver but I can close my monthly saver with BOS which is all on the same page.colsten said:

You will have to use online banking to do itsurreysaver said:

I cannot see how to close an account in the Halifax or BoS appMDMD said:You also need to close the everyday saver account they have opened. That way the old account will be converted into a new everyday saver rather than roll round into a new RS.

Is that not strange?

Edit - having just checked, you can withdraw money from the BoS one, but not the HalifaxOk, so I have a regular saver still paying the old rate of 2% due to mature soon.

Obviously, I want this to go full term to get the most back.

So, are you saying allow it to mature and get moved to an easy access saver but cancel the SO and then convert the new regular saver as you described to an easy access saver?

Then delete both easy access savers, this is getting complicated.

1. close the associated easy access saver before the old one matures. This is needed so you can time the payment in step 4.

2. let the RS run to term and convert to a new easy access everyday saver

3. withdraw all the funds and close the easy access account

4. Open a new RS online, with the first payment preferably as close to the end of the month as possible, and pay in a second and subsequent payments in on 1st of every month.Step 4 allows you to effectively make a £500 first payment (if payment one is on 28th Feb and payment two is on 1st March), although the benefits are lower at a rate of 1%. You can do the same with BOS.

the “renew RS into an easy access saver” thing is only relevant if you want to access the funds early - you can’t withdraw from the account but to close it online you have to have a balance of less than £5, but if you “renew” you get round that issue.1 -

Except you'd need the first payment in by 26th February, as 28th is a non working day. I always like to ensure I adhere to the T&Cs, which say 25th, that way they have no come back if something goes wrongMDMD said:

To get the max benefit you need totrickydicky14 said:quirkydeptless said:

You can close the Halifax Regular Saver early. I have done it. To close it online you need to "renew" it as an Easy Access Saver and then you can close that.surreysaver said:

The BoS and Halifax Monthly/Regular Savers have different T&Cs. I believe you can close the BoS one early, but not the Halifaxtrickydicky14 said:

Just been looking at my accounts with Halifax and BOS, following the above info I can close my every day saver online but not my Halifax regular saver but I can close my monthly saver with BOS which is all on the same page.colsten said:

You will have to use online banking to do itsurreysaver said:

I cannot see how to close an account in the Halifax or BoS appMDMD said:You also need to close the everyday saver account they have opened. That way the old account will be converted into a new everyday saver rather than roll round into a new RS.

Is that not strange?

Edit - having just checked, you can withdraw money from the BoS one, but not the HalifaxOk, so I have a regular saver still paying the old rate of 2% due to mature soon.

Obviously, I want this to go full term to get the most back.

So, are you saying allow it to mature and get moved to an easy access saver but cancel the SO and then convert the new regular saver as you described to an easy access saver?

Then delete both easy access savers, this is getting complicated.

1. close the associated easy access saver before the old one matures. This is needed so you can time the payment in step 4.

2. let the RS run to term and convert to a new easy access everyday saver

4. withdraw all the funds and close the easy access account

4. Open a new RS online, with the first payment preferably as close to the end of the month as possible, and pay in a second and subsequent payments in on 1st of every month.Step 4 allows you to effectively make a £500 first payment (if payment one is on 28th Feb and payment two is on 1st March), although the benefits are lower at a rate of 1%. You can do the same with BOS.

the “renew RS into an easy access saver” thing is only relevant if you want to access the funds early - you can’t withdraw from the account but to close it online you have to have a balance of less than £5, but if you “renew” you get round that issue.I consider myself to be a male feminist. Is that allowed?0 -

Good point, plus if you do it at the weekend it may be treated as being made on the 1stsurreysaver said:

Except you'd need the first payment in by 26th February, as 28th is a non working day. I always like to ensure I adhere to the T&Cs, which say 25th, that way they have no come back if something goes wrongMDMD said:

To get the max benefit you need totrickydicky14 said:quirkydeptless said:

You can close the Halifax Regular Saver early. I have done it. To close it online you need to "renew" it as an Easy Access Saver and then you can close that.surreysaver said:

The BoS and Halifax Monthly/Regular Savers have different T&Cs. I believe you can close the BoS one early, but not the Halifaxtrickydicky14 said:

Just been looking at my accounts with Halifax and BOS, following the above info I can close my every day saver online but not my Halifax regular saver but I can close my monthly saver with BOS which is all on the same page.colsten said:

You will have to use online banking to do itsurreysaver said:

I cannot see how to close an account in the Halifax or BoS appMDMD said:You also need to close the everyday saver account they have opened. That way the old account will be converted into a new everyday saver rather than roll round into a new RS.

Is that not strange?

Edit - having just checked, you can withdraw money from the BoS one, but not the HalifaxOk, so I have a regular saver still paying the old rate of 2% due to mature soon.

Obviously, I want this to go full term to get the most back.

So, are you saying allow it to mature and get moved to an easy access saver but cancel the SO and then convert the new regular saver as you described to an easy access saver?

Then delete both easy access savers, this is getting complicated.

1. close the associated easy access saver before the old one matures. This is needed so you can time the payment in step 4.

2. let the RS run to term and convert to a new easy access everyday saver

4. withdraw all the funds and close the easy access account

4. Open a new RS online, with the first payment preferably as close to the end of the month as possible, and pay in a second and subsequent payments in on 1st of every month.Step 4 allows you to effectively make a £500 first payment (if payment one is on 28th Feb and payment two is on 1st March), although the benefits are lower at a rate of 1%. You can do the same with BOS.

the “renew RS into an easy access saver” thing is only relevant if you want to access the funds early - you can’t withdraw from the account but to close it online you have to have a balance of less than £5, but if you “renew” you get round that issue.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards