We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

AJBell fund advice

Comments

-

Not sure March 2020 qualifies as a “slight market turbulence”. I thought it was eye opening. Sure, we had a sharp drop and a V shape recovery. And it was short. But the drop was really, really fast. It was awe-inspiring how governments shut down economies across the world. And then promptly acted to flood the markets with liquidity. Didn’t have to recover like that. Other scenarios were plausible. And the damage has been much deeper than the stock market shows. Particularly among smaller, non-publicly traded companies. And the winners were completely random. And the next round could be similar with a different outcome.BritishInvestor said:

"Well, if you have straightforward needs (want £X,000 for Y years, then £Z for the rest of your life), and a pot of £A,000....that complex planning you hint at is not that complex really."cfw1994 said:

In order:BritishInvestor said:

It might be useful to differentiate investing (which, these days, can, and should be, straightforward) and retirement planning, which isn't necessarily always that straightforward.cfw1994 said:

Glad you like it: I thought it did illustrate things fairly easilyScallypud said:

Love this. Simple but informativecfw1994 said:Curious.

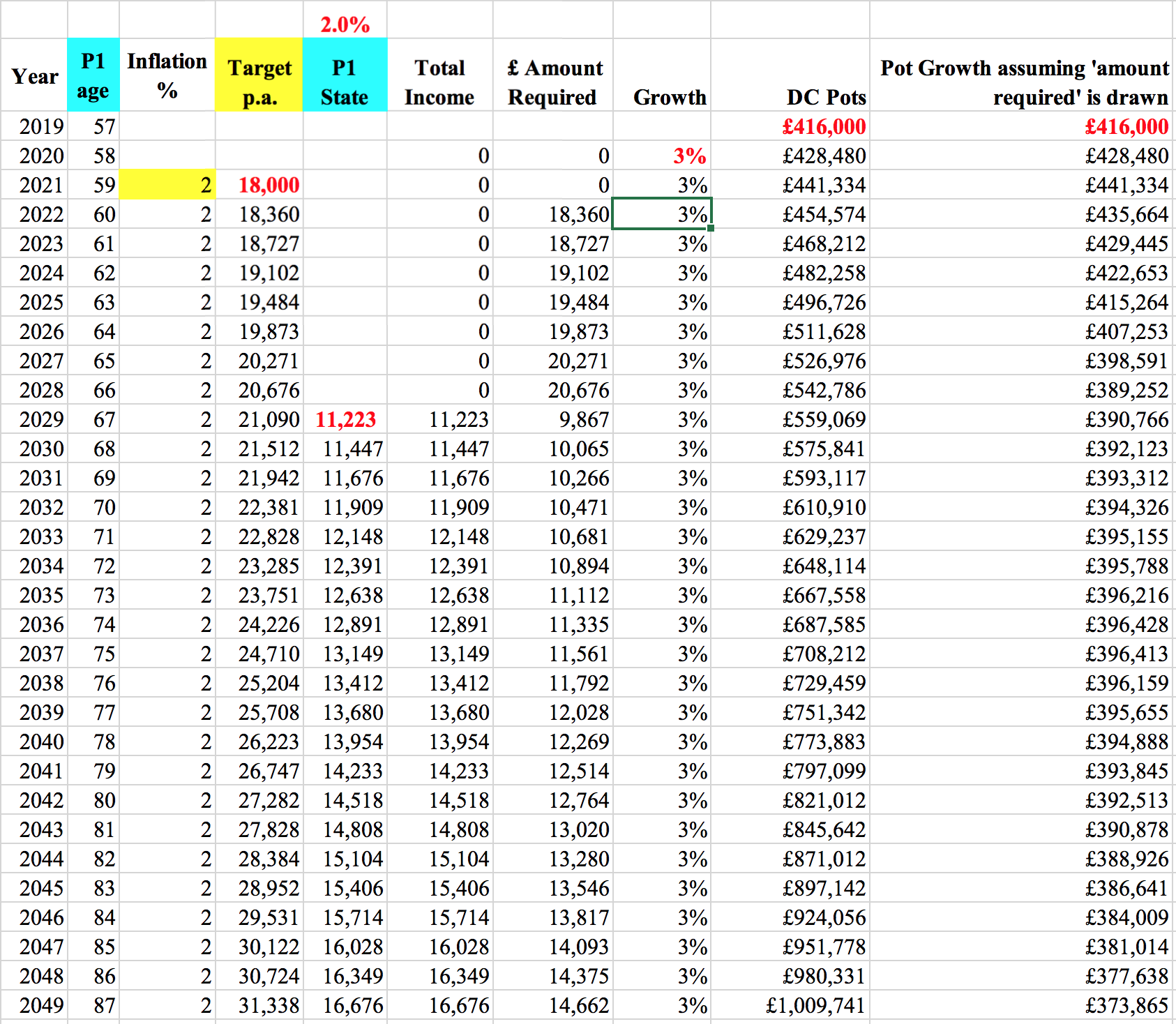

My magic spreaddie suggest that you should be fine, even if you only average 2% to last until you are 100.

Maybe I have misread the numbers. If so, let me know!

Sample below - assuming you want 18k at todays money, rising at 2% (3rd column - note it says 'inflation, but today inflation is under 1% !!).

If you would like a copy to play with numbers, let me know - it is pretty basic really.

If you get 3%, happy days, all good: the last column shows how much the two pots you describe end up each year, after taking the income in the "£ Amount Required" column:

If I have misunderstood some of the numbers, let me know.

I have put the State pension as if it gets a 2% rise each year - slightly lower than how things stand today - remember, as things stand, there is a "triple lock" protection that guarantees the state pension would increase by the greatest of the following three measures:- Average earnings

- Prices, as measured by the Consumer Prices Index (CPI)

- 2.5 per cent

Of course the "Growth" column will vary from year to year, perhaps wildly, so it is wise to play with it and drop some negative years in, particularly early on, but if you can keep some cash funds (ours are in Premium Bonds), and have the ability to "pause" the drawdown, then you can help mitigate downturns.

In terms of "advising you where to invest" - you will NOT get that here: advice comes with the need for regulations and training, and although there are one or two such advisors here, they would not give you a simple answer given the little information we all read here - plus, that would rather take away the mystery of finance")

If I were unsure of things, I would probably pop it all in a Vanguard LifeStrategy 80, or perhaps LS60, to capture the essence of "invest in the world".

YES, there is a lot more information , as dunstonh & others outlined, that would be needed to get to the bottom of what the best thing for YOU is, but who knows what tomorrow can bring!

But that is just my personal suggestion, just an invisible individual on the internet!")

In answer to @BritishInvestor, where I said "plus, that would rather take away the mystery of finance": well, reading up the thread, I saw requests for a range of things:- What drawdown strategy are you following?

- Total return or yield?

- Will you be segmenting your portfolio for different time periods?

- Will you operate a cash account within the pension or outside of the pension?

- What sort of volatility level are you aiming for?

All things I would expect an IFA to ask, and of course charge a % to assess and give advice.....& they might then construct a portfolio of 10-20 funds, as we often see in this forum....but I would ask if that is often needed?

The very building of those complex things, in my mine, often helps maintain the "mystery of finance". Makes the "average person" feel they are incapable of doing it, so maybe they should pay someone else to do it for themselves.

Of course, some people have complex lives, & absolutely warrant that work.....but I feel many do not: maybe a simpler option will be more than sufficient - and with some simple guidance, they might feel more able to control things themselves.

Each to their own, of course, & as I pointed out, nothing anyone gives here is "advice".

As Mordko suggested, getting a simple multi-asset fund (or my suggestion - look at Vanguard LS60 or LS80) could likely cover things perfectly well.

My spreadsheet was used to illustrate how the money *could* play out over the years ahead.

Care to comment?

"and of course charge a % "

It's hopefully going to be a fee these days.

"and with some simple guidance, they might feel more able to control things themselves."

In theory, I don't necessarily disagree, but what is often the case on forums is people tend to jump to "solution" mode, when the "real" objective hasn't really been uncovered.

One could argue that anyone that comes on here asking for guidance and is currently paying an adviser should consider why they are paying an adviser in the first place. Seems a waste of money to me.

Investment v Retirement Planning. Well, if you have straightforward needs (want £X,000 for Y years, then £Z for the rest of your life), and a pot of £A,000....that complex planning you hint at is not that complex really.

Clearly you might want to 'stress test' things - hence the simple spreadsheet approach, allowing you to drop in a -20% year (or two, or three, or -30%, or -40% - how much planning do you want to plan for, & how much would the FA/IFA do?)

A fee versus a % to manage? That would be refreshing, but what I read suggests the vast majority still charge a % under management - you think not?

Forums are never going to dig into the "real" objective - they are a way to ask a question and get an answer, not know the subtle nuances of the OPs life!

I suspect there are plenty here who use a financial advisor but come on here for either confirmation, or to figure things out (& perhaps 'go solo' later). Always ways to waste money!

I think some people (even those that have worked in the area professionally in a full-time capacity for many years - both academics and practitioners) see it as a challenging task even for something that appears on the surface a simple question, but I guess you are a lot further down the road than most.

Some potential challenges/issues I've observed:

1. Lack of understanding of how bad things can get (based on historical data) and the impact on their chosen portfolio.

2. Taking far more risk than they need to.

3. Altering their spending plans at the slight market turbulence (Covid)

4. Conversely not knowing when an adjustment might need to be made

5. Little understanding of "rules of thumbs" such as the 4% rule and the impact of real-world factors such as inflation, asset allocation, fees, longevity etc.

6. Stress testing without really understanding what it is that stresses a retirement portfolio - inflation spikes are often ignored.

7. Use of more complex withdrawal strategies such as Guyton Klinger without understanding the potential downsides.

8. No understanding of the trades off between level of withdrawals, success rate and potential adjustments.

9. Not understanding the impact of various approaches (e.g. bucketing) on likely portfolio success.

With all that said, I'm not sure your typical IFA is really going to help with the above.

"the vast majority still charge a % under management - you think not?"

I guess so, but I'm some exist out there that will charge something closer to a flat fee.1 -

Just pay someone a flat fee for life coaching, you don;t need anything else.0

-

"What constructive thoughts do you have for the OP?cfw1994 said:So....throw our arms in the air in despair, & work until we drop?

Certainly one approach!

or....accept that life can and does throw curveballs, figure out what you want to live on, take a stab when you get there (hint: it looks to me like the OP is pretty well there!) & plan ahead.

People post this kind of question for some guidance, ideas, something to help them.What constructive thoughts do you have for the OP?

Violent disagreement with my suggestions?

Alternative ideas?

Violent disagreement with my suggestions?

Alternative ideas?"

I think the best (and maybe only) approach is self-education.

Read, absorb, and read again, as widely as possible.

Minimise unknown, unknowns (through education)

Ask questions on here, but I think you'd get a lot more value after having done some reading first

I really understand the good intentions with sharing sheets, but the emphasis really has to go on understanding the drivers behind it first, IMO.

When I undertook a house refurbishment a few years ago I knew absolutely nothing about the subject but spent a lot of time (too much") ) reading around the topic and getting to a position where I could at least start to ask the right questions of the PM and why he might be making the decisions that he was. Without doing this I would never have had the same outcome. 0

) reading around the topic and getting to a position where I could at least start to ask the right questions of the PM and why he might be making the decisions that he was. Without doing this I would never have had the same outcome. 0 -

"Other scenarios were plausible."Deleted_User said:

Not sure March 2020 qualifies as a “slight market turbulence”. I thought it was eye opening. Sure, we had a sharp drop and a V shape recovery. And it was short. But the drop was really, really fast. It was awe-inspiring how governments shut down economies across the world. And then promptly acted to flood the markets with liquidity. Didn’t have to recover like that. Other scenarios were plausible. And the damage has been much deeper than the stock market shows. Particularly among smaller, non-publicly traded companies. And the winners were completely random. And the next round could be similar with a different outcome.BritishInvestor said:

"Well, if you have straightforward needs (want £X,000 for Y years, then £Z for the rest of your life), and a pot of £A,000....that complex planning you hint at is not that complex really."cfw1994 said:

In order:BritishInvestor said:

It might be useful to differentiate investing (which, these days, can, and should be, straightforward) and retirement planning, which isn't necessarily always that straightforward.cfw1994 said:

Glad you like it: I thought it did illustrate things fairly easilyScallypud said:

Love this. Simple but informativecfw1994 said:Curious.

My magic spreaddie suggest that you should be fine, even if you only average 2% to last until you are 100.

Maybe I have misread the numbers. If so, let me know!

Sample below - assuming you want 18k at todays money, rising at 2% (3rd column - note it says 'inflation, but today inflation is under 1% !!).

If you would like a copy to play with numbers, let me know - it is pretty basic really.

If you get 3%, happy days, all good: the last column shows how much the two pots you describe end up each year, after taking the income in the "£ Amount Required" column:

If I have misunderstood some of the numbers, let me know.

I have put the State pension as if it gets a 2% rise each year - slightly lower than how things stand today - remember, as things stand, there is a "triple lock" protection that guarantees the state pension would increase by the greatest of the following three measures:- Average earnings

- Prices, as measured by the Consumer Prices Index (CPI)

- 2.5 per cent

Of course the "Growth" column will vary from year to year, perhaps wildly, so it is wise to play with it and drop some negative years in, particularly early on, but if you can keep some cash funds (ours are in Premium Bonds), and have the ability to "pause" the drawdown, then you can help mitigate downturns.

In terms of "advising you where to invest" - you will NOT get that here: advice comes with the need for regulations and training, and although there are one or two such advisors here, they would not give you a simple answer given the little information we all read here - plus, that would rather take away the mystery of finance

If I were unsure of things, I would probably pop it all in a Vanguard LifeStrategy 80, or perhaps LS60, to capture the essence of "invest in the world".

YES, there is a lot more information , as dunstonh & others outlined, that would be needed to get to the bottom of what the best thing for YOU is, but who knows what tomorrow can bring!

But that is just my personal suggestion, just an invisible individual on the internet!

In answer to @BritishInvestor, where I said "plus, that would rather take away the mystery of finance": well, reading up the thread, I saw requests for a range of things:- What drawdown strategy are you following?

- Total return or yield?

- Will you be segmenting your portfolio for different time periods?

- Will you operate a cash account within the pension or outside of the pension?

- What sort of volatility level are you aiming for?

All things I would expect an IFA to ask, and of course charge a % to assess and give advice.....& they might then construct a portfolio of 10-20 funds, as we often see in this forum....but I would ask if that is often needed?

The very building of those complex things, in my mine, often helps maintain the "mystery of finance". Makes the "average person" feel they are incapable of doing it, so maybe they should pay someone else to do it for themselves.

Of course, some people have complex lives, & absolutely warrant that work.....but I feel many do not: maybe a simpler option will be more than sufficient - and with some simple guidance, they might feel more able to control things themselves.

Each to their own, of course, & as I pointed out, nothing anyone gives here is "advice".

As Mordko suggested, getting a simple multi-asset fund (or my suggestion - look at Vanguard LS60 or LS80) could likely cover things perfectly well.

My spreadsheet was used to illustrate how the money *could* play out over the years ahead.

Care to comment?

"and of course charge a % "

It's hopefully going to be a fee these days.

"and with some simple guidance, they might feel more able to control things themselves."

In theory, I don't necessarily disagree, but what is often the case on forums is people tend to jump to "solution" mode, when the "real" objective hasn't really been uncovered.

One could argue that anyone that comes on here asking for guidance and is currently paying an adviser should consider why they are paying an adviser in the first place. Seems a waste of money to me.

Investment v Retirement Planning. Well, if you have straightforward needs (want £X,000 for Y years, then £Z for the rest of your life), and a pot of £A,000....that complex planning you hint at is not that complex really.

Clearly you might want to 'stress test' things - hence the simple spreadsheet approach, allowing you to drop in a -20% year (or two, or three, or -30%, or -40% - how much planning do you want to plan for, & how much would the FA/IFA do?)

A fee versus a % to manage? That would be refreshing, but what I read suggests the vast majority still charge a % under management - you think not?

Forums are never going to dig into the "real" objective - they are a way to ask a question and get an answer, not know the subtle nuances of the OPs life!

I suspect there are plenty here who use a financial advisor but come on here for either confirmation, or to figure things out (& perhaps 'go solo' later). Always ways to waste money!

I think some people (even those that have worked in the area professionally in a full-time capacity for many years - both academics and practitioners) see it as a challenging task even for something that appears on the surface a simple question, but I guess you are a lot further down the road than most.

Some potential challenges/issues I've observed:

1. Lack of understanding of how bad things can get (based on historical data) and the impact on their chosen portfolio.

2. Taking far more risk than they need to.

3. Altering their spending plans at the slight market turbulence (Covid)

4. Conversely not knowing when an adjustment might need to be made

5. Little understanding of "rules of thumbs" such as the 4% rule and the impact of real-world factors such as inflation, asset allocation, fees, longevity etc.

6. Stress testing without really understanding what it is that stresses a retirement portfolio - inflation spikes are often ignored.

7. Use of more complex withdrawal strategies such as Guyton Klinger without understanding the potential downsides.

8. No understanding of the trades off between level of withdrawals, success rate and potential adjustments.

9. Not understanding the impact of various approaches (e.g. bucketing) on likely portfolio success.

With all that said, I'm not sure your typical IFA is really going to help with the above.

"the vast majority still charge a % under management - you think not?"

I guess so, but I'm some exist out there that will charge something closer to a flat fee.

"And the next round could be similar with a different outcome."

I don't disagree, but history has been littered with outcomes that might have been different - all we can do is play what is in front of us, and (I think I have posted this before), given

1. The run up in asset prices prior to the slump.

2. High quality bonds holding up reasonably well.

3. Benign inflation

4. The sharp recovery

The impact on a typical retirement portfolio was limited (but accept I was over egging it with the "slight" comment) 0 -

Can you elaborate?NottinghamKnight said:Just pay someone a flat fee for life coaching, you don;t need anything else.0 -

Agree 100% with "self education"....& clearly you need to know what to ask before asking strangers on a forum....but getting views and ideas from a forum like this is absolutely invaluable. FWIW, we have had two extensions done over the past 15 years....both probably took us over a year in the planning, & that included getting comments/views from some helpful forum folk.BritishInvestor said:

"What constructive thoughts do you have for the OP?cfw1994 said:So....throw our arms in the air in despair, & work until we drop?

Certainly one approach!

or....accept that life can and does throw curveballs, figure out what you want to live on, take a stab when you get there (hint: it looks to me like the OP is pretty well there!) & plan ahead.

People post this kind of question for some guidance, ideas, something to help them.What constructive thoughts do you have for the OP?

Violent disagreement with my suggestions?

Alternative ideas?

Violent disagreement with my suggestions?

Alternative ideas?"

I think the best (and maybe only) approach is self-education.

Read, absorb, and read again, as widely as possible.

Minimise unknown, unknowns (through education)

Ask questions on here, but I think you'd get a lot more value after having done some reading first

I really understand the good intentions with sharing sheets, but the emphasis really has to go on understanding the drivers behind it first, IMO.

When I undertook a house refurbishment a few years ago I knew absolutely nothing about the subject but spent a lot of time (too much) reading around the topic and getting to a position where I could at least start to ask the right questions of the PM and why he might be making the decisions that he was. Without doing this I would never have had the same outcome.

No thoughts on the numbers I posted, other than seeing they had "good intentions" behind them?

Would that not help give some weight to the fact that things look reasonable for the OP?

"the emphasis really has to go on understanding the drivers behind it first" - ahh, so @NottinghamKnight is right - just get some life coaching and you'll be sorted

Plan for tomorrow, enjoy today!0 -

I have my SIPP and ISA’s on different platforms and both provide detailed breakdown statements of all charges applied once a year so it is clear in GBP terms.

Also, % is charged annually on the original value again and again and again. So the original Xk after a couple of decades will have lots of bites taken out of it. And any growth is charged too with the total charges typically escalating well ahead of inflation. While a property set up portfolio needs very little work, the adviser gets paid while he sleeps. Quoting % rather than GBP makes sense. For the adviser.

Do you think if people struggle to work out 0.5% of a portfolio they might need help?

Earlier in the thread you put the point very well that meeting your own goals rather than the potential to be a billionaire was the key. This point is often overlooked so if even after paying an IFA you can achieve your goals why not? As long as you know enough to ask the right questions.0 -

I think that committing to paying thousands of pounds annually for something that is unnecessary is the exact opposite of helping one to achieve financial goals.DT2001 said:

Earlier in the thread you put the point very well that meeting your own goals rather than the potential to be a billionaire was the key. This point is often overlooked so if even after paying an IFA you can achieve your goals why not? As long as you know enough to ask the right questions.

Also, % is charged annually on the original value again and again and again. So the original Xk after a couple of decades will have lots of bites taken out of it. And any growth is charged too with the total charges typically escalating well ahead of inflation. While a property set up portfolio needs very little work, the adviser gets paid while he sleeps. Quoting % rather than GBP makes sense. For the adviser.Keep in mind that an IFA won’t be interested if its a young investor with a beginner portfolio. And if its someone who already has a bit of experience under his belt and succeeded in building a bit of a nest then I struggle to understand why he would need to pay for expensive hand holding. A one off advice to set things up after a change might be warranted but the set up could and should be simple enough to self manage.

Given high asset prices and low expected returns, a 1% annual cost could wipe out most of your returns in real terms.And even if you experience losses under his management,IFA would still charge you thousands for the pleasure. How is that fair? In his early years Buffett only charged his clients a fee on a portion of return above treasury bond rate (around 5% at the time). That makes more sense to me. Why should anything at all be paid if you manage to return less than I can get by putting money into a zero risk asset?0 -

My extension planning took a couple of years from start to finish - who knew that accepting a larger radius on a sink would save so much cost, or that a hot water tap that produced water at 97 degrees rather than 100 was so much cheapercfw1994 said:

Agree 100% with "self education"....& clearly you need to know what to ask before asking strangers on a forum....but getting views and ideas from a forum like this is absolutely invaluable. FWIW, we have had two extensions done over the past 15 years....both probably took us over a year in the planning, & that included getting comments/views from some helpful forum folk.BritishInvestor said:

"What constructive thoughts do you have for the OP?cfw1994 said:So....throw our arms in the air in despair, & work until we drop?

Certainly one approach!

or....accept that life can and does throw curveballs, figure out what you want to live on, take a stab when you get there (hint: it looks to me like the OP is pretty well there!) & plan ahead.

People post this kind of question for some guidance, ideas, something to help them.What constructive thoughts do you have for the OP?

Violent disagreement with my suggestions?

Alternative ideas?

Violent disagreement with my suggestions?

Alternative ideas?"

I think the best (and maybe only) approach is self-education.

Read, absorb, and read again, as widely as possible.

Minimise unknown, unknowns (through education)

Ask questions on here, but I think you'd get a lot more value after having done some reading first

I really understand the good intentions with sharing sheets, but the emphasis really has to go on understanding the drivers behind it first, IMO.

When I undertook a house refurbishment a few years ago I knew absolutely nothing about the subject but spent a lot of time (too much) reading around the topic and getting to a position where I could at least start to ask the right questions of the PM and why he might be making the decisions that he was. Without doing this I would never have had the same outcome.

No thoughts on the numbers I posted, other than seeing they had "good intentions" behind them?

Would that not help give some weight to the fact that things look reasonable for the OP?

"the emphasis really has to go on understanding the drivers behind it first" - ahh, so @NottinghamKnight is right - just get some life coaching and you'll be sorted

Not really sure what the life coaching would involve!?

0 -

"Keep in mind that an IFA won’t be interested if its a young investor with a beginner portfolio."Deleted_User said:

I think that committing to paying thousands of pounds annually for something that is unnecessary is the exact opposite of helping one to achieve financial goals.DT2001 said:

Earlier in the thread you put the point very well that meeting your own goals rather than the potential to be a billionaire was the key. This point is often overlooked so if even after paying an IFA you can achieve your goals why not? As long as you know enough to ask the right questions.

Also, % is charged annually on the original value again and again and again. So the original Xk after a couple of decades will have lots of bites taken out of it. And any growth is charged too with the total charges typically escalating well ahead of inflation. While a property set up portfolio needs very little work, the adviser gets paid while he sleeps. Quoting % rather than GBP makes sense. For the adviser.Keep in mind that an IFA won’t be interested if its a young investor with a beginner portfolio. And if its someone who already has a bit of experience under his belt and succeeded in building a bit of a nest then I struggle to understand why he would need to pay for expensive hand holding. A one off advice to set things up after a change might be warranted but the set up could and should be simple enough to self manage.

Given high asset prices and low expected returns, a 1% annual cost could wipe out most of your returns in real terms.And even if you experience losses under his management,IFA would still charge you thousands for the pleasure. How is that fair? In his early years Buffett only charged his clients a fee on a portion of return above treasury bond rate (around 5% at the time). That makes more sense to me. Why should anything at all be paid if you manage to return less than I can get by putting money into a zero risk asset?

I think that's understandable, what value can they genuinely add to cover their costs?

"And if its someone who already has a bit of experience under his belt and succeeded in building a bit of a nest then I struggle to understand why he would need to pay for expensive hand holding."

A lack of confidence, knowledge, time or general lack of interest. For someone with a high paying job with long hours they might choose to outsource this part of their life given what they consider the hourly value of their time.

"That makes more sense to me."

I'm really not sure how, and it goes back to the point around investment management being commoditised, surely you don't want to hire someone that promises you great returns?

1. The chances of finding someone with an edge in the retail space is pretty low

2. The chances of you finding someone that tells you they have an edge is pretty high.

If I spoke to a product flogger and they showed me some great historical returns, that would be a big warning flag. I've seen some stinkers.

1

![[Deleted User]](https://us-noi.v-cdn.net/6031891/uploads/defaultavatar/nFA7H6UNOO0N5.jpg)

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.2K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.2K Work, Benefits & Business

- 603.8K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards