We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Business interruption insurance

Unclemeat

Posts: 2 Newbie

I purchased business interruption September 2019, I rung the company about claiming when the lockdown in March started as I had to close my shop. I was told my policy didn’t cover me for COVID as it wasn’t on the list. Can I now claim after the high court ruling ?

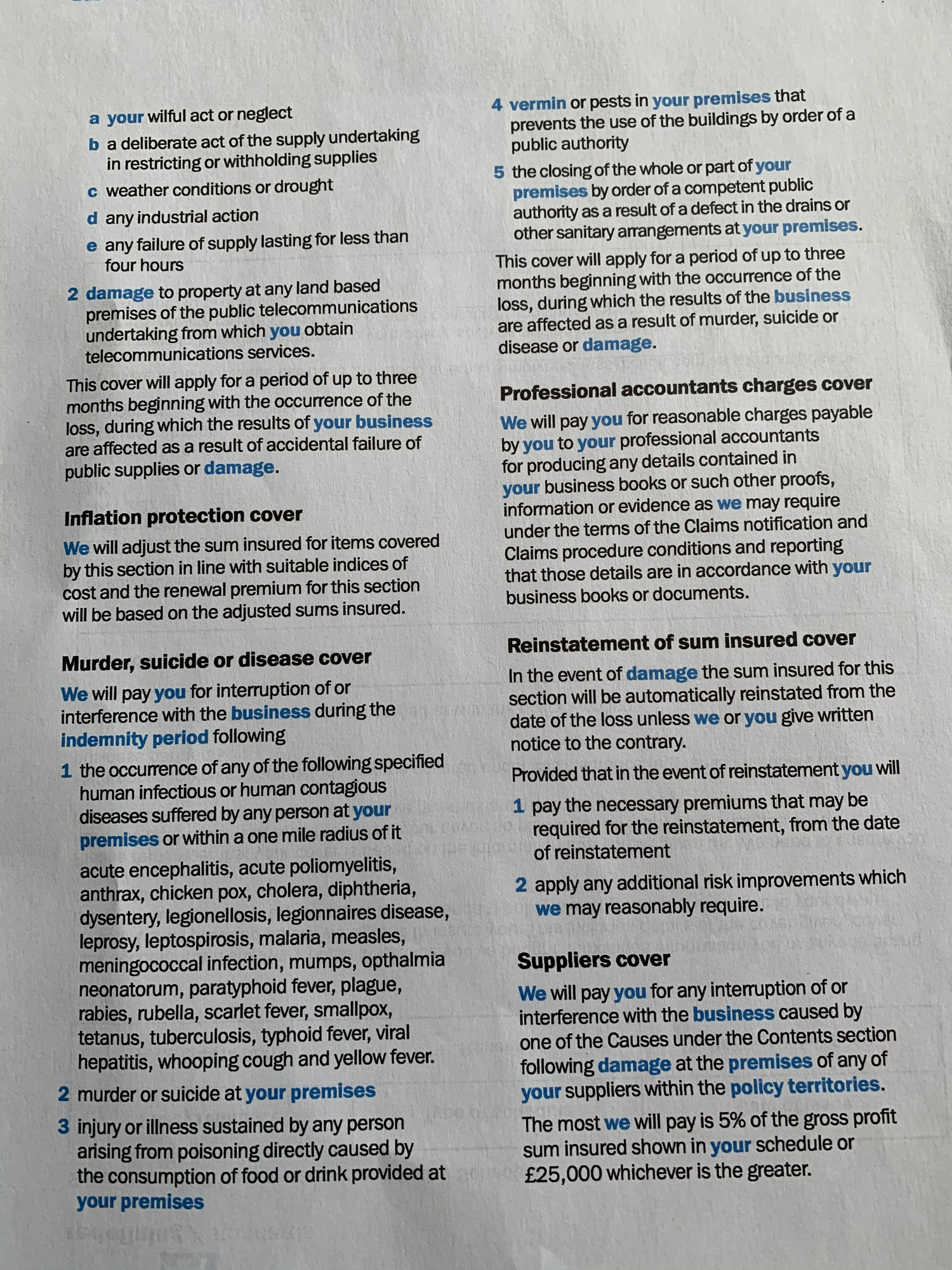

Here is part of my policy

0

Comments

-

The supreme court decision is addressed at https://www.fca.org.uk/news/press-releases/supreme-court-judgment-business-interruption-insurance-test-case

If you look at the judgment, the sort of clause they were considering was:

“We shall indemnify You in respect of interruption or interference with the Business during the Indemnity Period following:

a. any

i. occurrence of a Notifiable Disease (as defined below) at the Premises or attributable to food or drink supplied from the Premises;

ii. discovery of an organism at the Premises likely to result in the occurrence of a Notifiable Disease;

iii. occurrence of a Notifiable Disease within a radius of 25 miles of the Premises;

..."

Your policy specifically lists the diseases covered by the policy, and coronavirus is not listed. The supreme court case was addressing policies covering notifiable diseases, and coronavirus became a notifiable disease. Therefore the supreme court decision does not help you.0 -

It does not look like it as your policy covers inclusion of things which are covered (for example some policies stated "transmissible diseases" rather than a specific list), rather than exclusion of things which are not and there does not appear to be a blanket business interruption clause in the policy. I have not read the new judgement in it's entirety, you can always contract your insurer again and say "In light of the ruling..." and see what they say, for the time taken to make one phone call you have nothing to lose.0

-

Thanks will give it a go0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.5K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.6K Work, Benefits & Business

- 603K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards