We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Pension recovery performance 2020

Comments

-

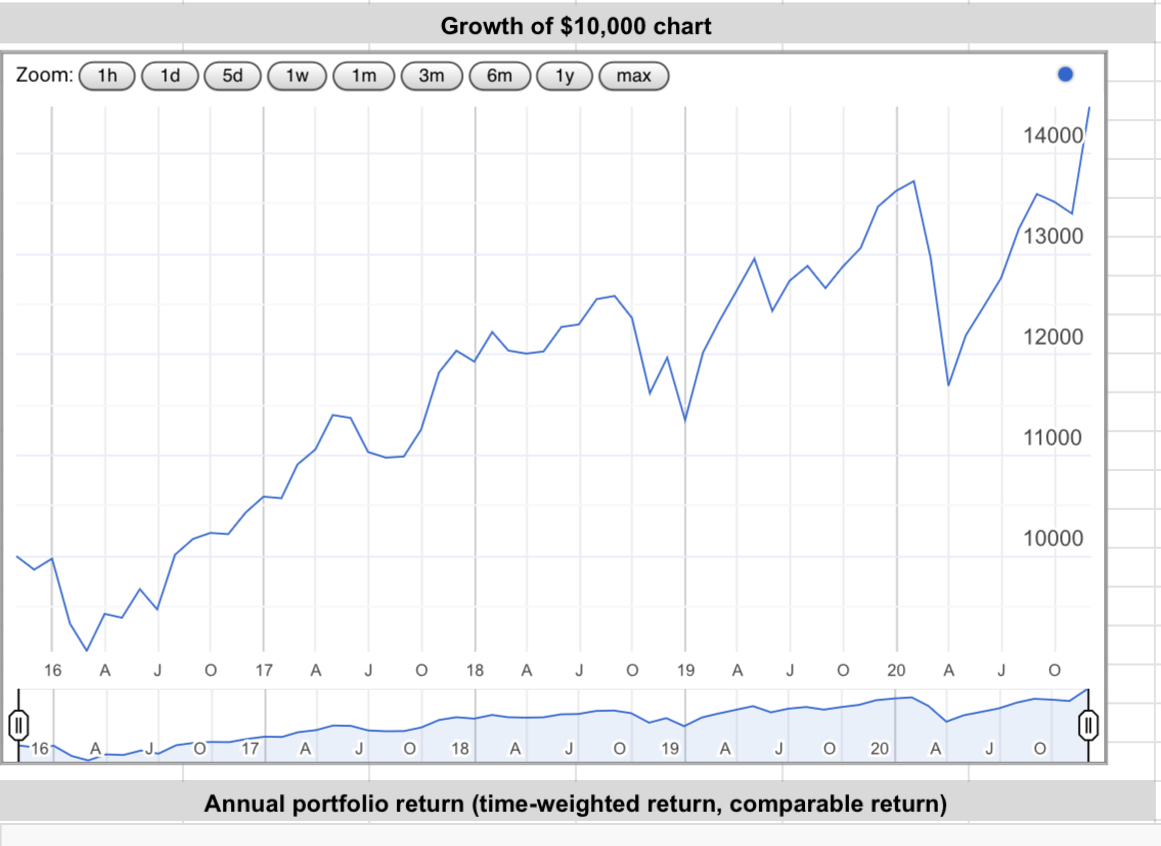

Time weighted returns for my 70% equity/30% fixed income portfolio over the last 5 years (in CAD; GBP dropped by 30% or so). FI changed from 20% to 30% early in 2020 as I am thinking about quitting my job and focusing on hobbies while trying to make them more profitable. Everything moved along my long term trend of ~7%/a above inflation. As you can see from the plot, if I were to pick 2 points in time, I can happily report a growth rate that is much higher than my normal trend.1

Time weighted returns for my 70% equity/30% fixed income portfolio over the last 5 years (in CAD; GBP dropped by 30% or so). FI changed from 20% to 30% early in 2020 as I am thinking about quitting my job and focusing on hobbies while trying to make them more profitable. Everything moved along my long term trend of ~7%/a above inflation. As you can see from the plot, if I were to pick 2 points in time, I can happily report a growth rate that is much higher than my normal trend.1 -

Our overall pots have increased by more than we've spent in the last year.

That's all we need.How's it going, AKA, Nutwatch? - 12 month spends to date = 3.24% of current retirement "pot" (as at end December 2025)2 -

Deleted_User said:

That’s true. If one wants to compare how portfolios perform then he/she should use time weighted returns over a reasonable period of time and a predefined set of dates. If one wants to advertise then he/she should pick a couple of dates that suit his purpose, carefully select what to report and then publish meaningless and unsustainable numbers to attract more punters.itwasntme001 said:Deleted_User said:1. reporting returns at arbitrary points in time is meaningless. Having said this, maximum drawdown from peak can be useful.2. Ditto for short periods of time. 10 or 20 year portfolio returns are a bit more interesting.3. Only time weighted returns can be compared meaningfully.4. Reporting returns without specifying your asset allocation is also meaningless.5. No confidence in most poster’s ability to calculate their returns. If you really want to know whether your investment vehicles performed as expected, compare against an appropriate benchmark.Agree with all of this except maybe point 3. Surely it depends on why we are comparing performance?Yes that's a fair point, I agree time-weighted method is the best way to compare performances. So yes all your points taken together I agree with 100%.1 -

Deleted_User said:1. reporting returns at arbitrary points in time is meaningless. Having said this, maximum drawdown from peak can be useful.2. Ditto for short periods of time. 10 or 20 year portfolio returns are a bit more interesting.3. Only time weighted returns can be compared meaningfully.4. Reporting returns without specifying your asset allocation is also meaningless.5. No confidence in most poster’s ability to calculate their returns. If you really want to know whether your investment vehicles performed as expected, compare against an appropriate benchmark.

Just want to reiterate that this comment should be appreciated by us all.

1 -

I read these with interest , I'm no investor and rely on a large corporate advisor at a cost of 0.25pc per year to advise on funds for my SW pension. nothing special at all but at the moment Jan -Nov 2020 I'm at plus 12% , certainly helped by the fact that little is UK based i suppose , its doing that well my early retirement plan is looking close each week i check it!0

-

dunstonh, an 18.69% gain for this year to end November is a very good return for a medium risk portfolio. If you care to share, I'd be interested to know the percentage of equities to bonds and the percentages of growth equity to value equity for your medium risk portfolio?dunstonh said:I just wondered what sort of performance people were experiencing with their pension investment during this tumultuous year.Apart from one month of falls which were quickly recovered, it has been a good year.

Is this typical, above or below what people are generally seeing?It depends on their risk profiles. Our worst performance, for YTD, is the lowest risk at 4.62% and best performance is the highest risk at 33.85% with medium risk coming out at 18.69%.

1 -

How comfortable is everyone with Tesla joining the S&P 500 at an insane valuation?

0 -

Ambivalent. I already own Tesla through VTI (total US market). Frontrunning is cool; it provides more liquidity to the market.0

-

This is more than S&P 500 YTD, much more than FTSE100 or the world market YTD and more than Buffett’s long term return. And then there was his “aggressive” return which is much higher. If true, this is something fairly concentrated in US tech and not “medium risk”. Also, unsustainable. If anyone within the financial industry could consistently deliver this kind of outperformance over a meaningful period of time, they would be multi-billionnairs. We often see claims like this from the vendors of financial services.Audaxer said:

dunstonh, an 18.69% gain for this year to end November is a very good return for a medium risk portfolio. If you care to share, I'd be interested to know the percentage of equities to bonds and the percentages of growth equity to value equity for your medium risk portfolio?dunstonh said:I just wondered what sort of performance people were experiencing with their pension investment during this tumultuous year.Apart from one month of falls which were quickly recovered, it has been a good year.

Is this typical, above or below what people are generally seeing?It depends on their risk profiles. Our worst performance, for YTD, is the lowest risk at 4.62% and best performance is the highest risk at 33.85% with medium risk coming out at 18.69%.

1 -

i don't think dunstonh would lie. If those rates stated were achieved then I have no reason to doubt him (or her!).Deleted_User said:

This is more than S&P 500 YTD, much more than FTSE100 or the world market YTD and more than Buffett’s long term return. And then there was his “aggressive” return which is much higher. If true, this is something fairly concentrated in US tech and not “medium risk”. Also, unsustainable. If anyone within the financial industry could consistently deliver this kind of outperformance over a meaningful period of time, they would be multi-billionnairs. We often see claims like this from the vendors of financial services.Audaxer said:

dunstonh, an 18.69% gain for this year to end November is a very good return for a medium risk portfolio. If you care to share, I'd be interested to know the percentage of equities to bonds and the percentages of growth equity to value equity for your medium risk portfolio?dunstonh said:I just wondered what sort of performance people were experiencing with their pension investment during this tumultuous year.Apart from one month of falls which were quickly recovered, it has been a good year.

Is this typical, above or below what people are generally seeing?It depends on their risk profiles. Our worst performance, for YTD, is the lowest risk at 4.62% and best performance is the highest risk at 33.85% with medium risk coming out at 18.69%.

1

![[Deleted User]](https://us-noi.v-cdn.net/6031891/uploads/defaultavatar/nFA7H6UNOO0N5.jpg)

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards