We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Scottish Widows to AJ Bell

Comments

-

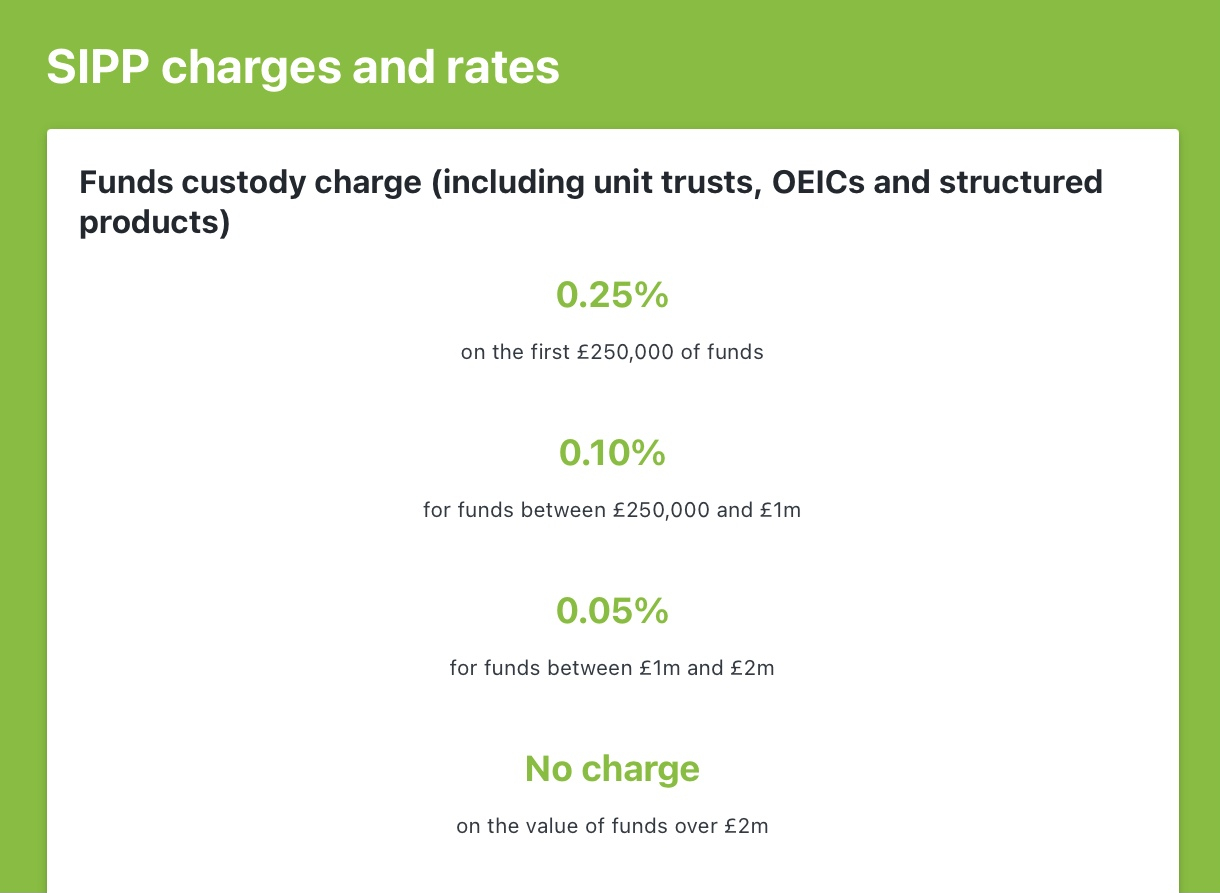

AJ Bell has a cap on funds of ...BuildTheWall said:

For tracker funds, aren’t you better off with Vanguard platform? Or even iWeb if it’s a one off investment. Not sure if AJ Bell has a cap.SteveC3 said:It's an occupational scheme with no extra tax free cash. What about funds selection with AJ Bell? I'm thinking of mainly equities in a tracker for say 50% to leave untouched for 5 to 10yrs and a 50/50 fund for the remainder from which I will draw from in the early years. Any recommendations on their funds?

£250,000 x 0.25% + £750,000 x 0.10% + £1,000,000 x 0.05% = £1,875.00

For comparison, Hargreaves Lansdown's cap is £4,000 - quite a difference.

0 -

I have an ISA with Vanguard and happy with it, but Vanguard don't have a drawdown system in place yetBuildTheWall said:

For tracker funds, aren’t you better off with Vanguard platform? Or even iWeb if it’s a one off investment. Not sure if AJ Bell has a cap.SteveC3 said:It's an occupational scheme with no extra tax free cash. What about funds selection with AJ Bell? I'm thinking of mainly equities in a tracker for say 50% to leave untouched for 5 to 10yrs and a 50/50 fund for the remainder from which I will draw from in the early years. Any recommendations on their funds?0 -

Also, I'm beginning to lean toward the Fundsmith Equity fund.SteveC3 said:

I have an ISA with Vanguard and happy with it, but Vanguard don't have a drawdown system in place yetBuildTheWall said:

For tracker funds, aren’t you better off with Vanguard platform? Or even iWeb if it’s a one off investment. Not sure if AJ Bell has a cap.SteveC3 said:It's an occupational scheme with no extra tax free cash. What about funds selection with AJ Bell? I'm thinking of mainly equities in a tracker for say 50% to leave untouched for 5 to 10yrs and a 50/50 fund for the remainder from which I will draw from in the early years. Any recommendations on their funds?0 -

In my opinion that's a very good choice, but of course you really should diversify well beyond one fund if you have £450K to invest.SteveC3 said:

Also, I'm beginning to lean toward the Fundsmith Equity fund.SteveC3 said:

I have an ISA with Vanguard and happy with it, but Vanguard don't have a drawdown system in place yetBuildTheWall said:

For tracker funds, aren’t you better off with Vanguard platform? Or even iWeb if it’s a one off investment. Not sure if AJ Bell has a cap.SteveC3 said:It's an occupational scheme with no extra tax free cash. What about funds selection with AJ Bell? I'm thinking of mainly equities in a tracker for say 50% to leave untouched for 5 to 10yrs and a 50/50 fund for the remainder from which I will draw from in the early years. Any recommendations on their funds?

Looking purely at actively managed global equities, also seriously consider Linsdell Train Global Equity and Scottish Mortgage. LTGE may not have done so well past 12 months, but that's mainly because it's more UK focused and fortunes have a habit of reversing. Looking to Asia, Bailie Gifford Shin Nippon may be worthy of a few percent, as could Baillie Gifford Pacific Horizons. My suggestions are not intended to be a balanced or diverse portfolio, just a few starting ideas to be going on with.

“Like a bunch of cod fishermen after all the cod’s been overfished, they don’t catch a lot of cod, but they keep on fishing in the same waters. That’s what’s happened to all these value investors. Maybe they should move to where the fish are.” Charlie Munger, vice chairman, Berkshire Hathaway0 -

I had no problem at all accessing my pension with Scottish Widows and there was no charge either unlike A J Bell that do charge. Why do you say accessing your pension would be 'painful?0

-

Fundsmith has a fairly low risk rating on Trustnet (for equities). Currently it's 74. That means it has been 26% less volatile than FTSE100.Steve182 said:

Fundsmith has a fairly low risk rating on Trustnet (for equities). Currently it's 74. That means it's supposed to be 26% less volatile than FTSE100,SteveC3 said:

I was actually looking at the Fundsmith Equity fund within AJ Bell!Steve182 said:

I must confess I don't use their funds, and most FA's would frown upon my own high risk/not so properly diversified asset allocation. I'm not personally a tracker fan. I have seen some successful active managers have added real value, well above the premium in fees charged. I'm a fan of SMT and Fundsmith. Others will disagree.SteveC3 said:It's an occupational scheme with no extra tax free cash. What about funds selection with AJ Bell? I'm thinking of mainly equities in a tracker for say 50% to leave untouched for 5 to 10yrs and a 50/50 fund for the remainder from which I will draw from in the early years. Any recommendations on their funds?

The risk rating is based on the past, not on the future.

0 -

At least half of all active funds will underperform an index, or probably a higher percentage once you include the extra fees. What makes you think you can pick one of the 75% of winners rather than the 75% of losers? Do you have some inside information that is not in the market?

I moved form SW to II as I reduced my total fees from .75% to <.2% and have a wiser choice of funds - so 0.55% of outperformance without having to try to guess which fund manager will be lucky next year.

I think....0 -

You are right. I am being a bit unfair and basing my comment on the current access to my plan. I haven't set up flexi access yet. I should take a look at the Scottish widows fund range in more detail.EdGasketTheSecond said:I had no problem at all accessing my pension with Scottish Widows and there was no charge either unlike A J Bell that do charge. Why do you say accessing your pension would be 'painful?0 -

Ah, the classic passive vs active debate.michaels said:At least half of all active funds will underperform an index, or probably a higher percentage once you include the extra fees. What makes you think you can pick one of the 75% of winners rather than the 75% of losers? Do you have some inside information that is not in the market?Performance of funds, their top 10 holdings, sector concentration, management track record - a lot of information is available. If you want to choose to not look at it, it’s your choice.Spreading investments among 4 or 5 active funds in the top 10 of your category based on past performance is not a terrible idea.The argument that active investors will be investing in all active funds and therefore destined to fail, is incorrect at best.0 -

If I stay with SW I have access to the Baillie Gifford Managed, which seems a popular choice at 0.5%. Too much choice, I'm getting confused. I need to see some sample drawdown portfolios for asset allocation. I'm still leaning towards high percentage equities as I'm in it until I pop my clogs, which hopefully, won't be too soon!0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.9K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 246.9K Work, Benefits & Business

- 603.5K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards