We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Mortgage broker - ask me anything

Comments

-

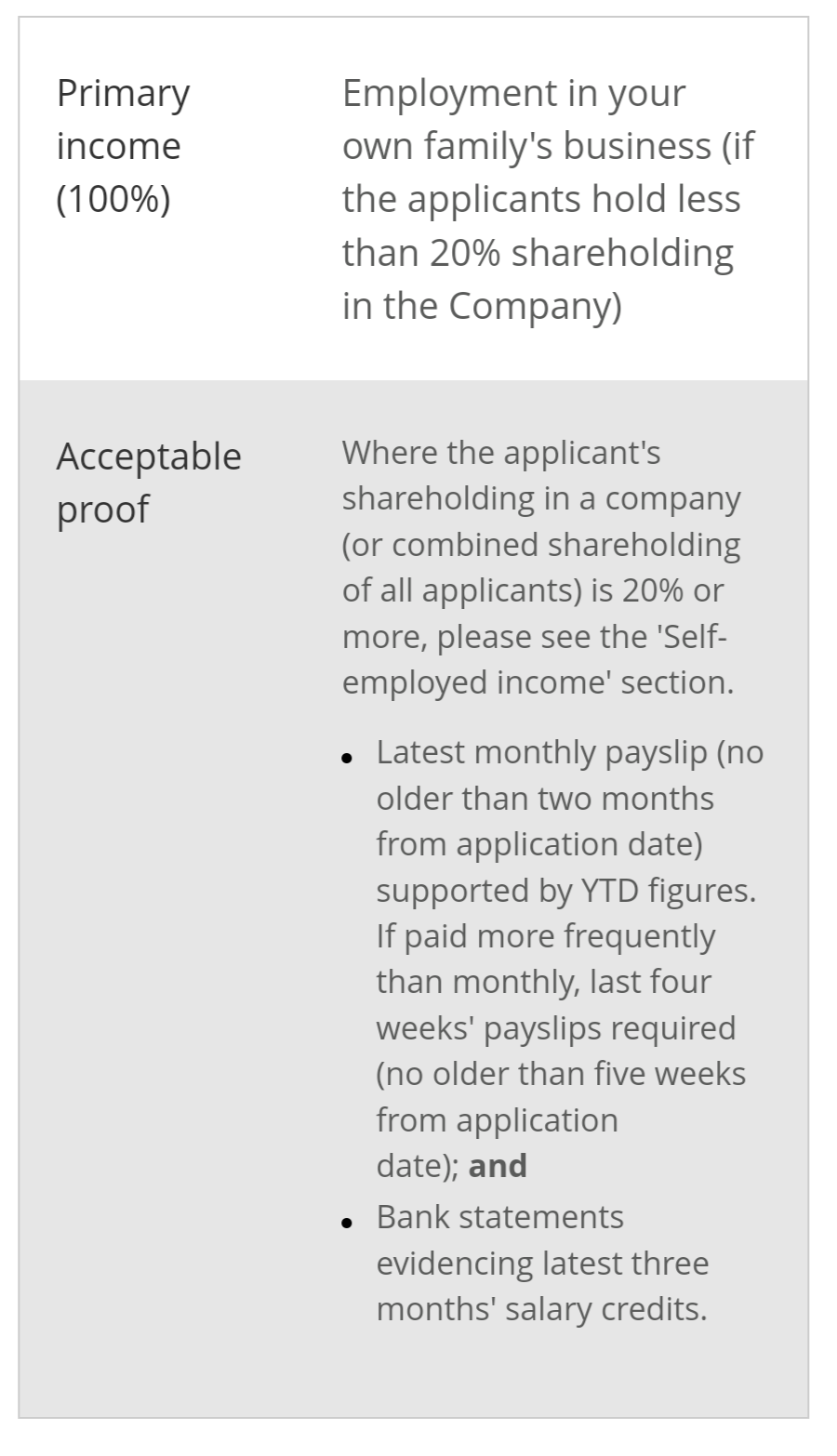

@Vp0007 PAYE income from family business - this is the published evidence requirement for SantanderVp0007 said:Hey! What documents do lenders usually ask for if I am employed by a family business? (no shareholding, just PAYE employee but the business is owned by direct family). Application is with Santander. Thanks

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

Hi there, I imagine this is a pretty naive question but I am currently a partner at an LLP firm and this will be the first year I pay tax through self assessment. However, my salary is set (plus a variable bonus). The only reason I'm classified as a Partner is because I have significant influence over decision making. So my question is, when applying for a mortgage would I say I am self-employed even though my salary is set?0

-

@zarathustra01 Are you a PAYE employee of the LLP? Is all of your income (salary+bonus) from the LLP paid through PAYE? Do you have monthly payslips that show the gross pay, tax & NI deductions, etc.?Zarathustra01 said:Hi there, I imagine this is a pretty naive question but I am currently a partner at an LLP firm and this will be the first year I pay tax through self assessment. However, my salary is set (plus a variable bonus). The only reason I'm classified as a Partner is because I have significant influence over decision making. So my question is, when applying for a mortgage would I say I am self-employed even though my salary is set?

If the answer to all of the above questions is Yes, then lenders may potentially consider you as employed for the purposes of the mortgage.

But given that you’ve said you pay taxes through SA and you’re doing your first SA, I’m guessing you aren’t paid through PAYE.I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

Hi, thanks for responding.K_S said:

@zarathustra01 Are you a PAYE employee of the LLP? Is all of your income (salary+bonus) from the LLP paid through PAYE? Do you have monthly payslips that show the gross pay, tax & NI deductions, etc.?Zarathustra01 said:Hi there, I imagine this is a pretty naive question but I am currently a partner at an LLP firm and this will be the first year I pay tax through self assessment. However, my salary is set (plus a variable bonus). The only reason I'm classified as a Partner is because I have significant influence over decision making. So my question is, when applying for a mortgage would I say I am self-employed even though my salary is set?

If the answer to all of the above questions is Yes, then lenders may potentially consider you as employed for the purposes of the mortgage.

But given that you’ve said you pay taxes through SA and you’re doing your first SA, I’m guessing you aren’t paid through PAYE.

The answer is no to all of them, my PAYE stopped in October when I became a Partner. So it looks like I will have to apply as self employed.

What I'm trying to get at is, given my salary is set, will a broker offer me similar terms to an employed person. Or will they just say "you're self employed so we can't offer you as big a mortgage"?0 -

@Zarathustra01Zarathustra01 said:

Hi, thanks for responding.K_S said:

@zarathustra01 Are you a PAYE employee of the LLP? Is all of your income (salary+bonus) from the LLP paid through PAYE? Do you have monthly payslips that show the gross pay, tax & NI deductions, etc.?Zarathustra01 said:Hi there, I imagine this is a pretty naive question but I am currently a partner at an LLP firm and this will be the first year I pay tax through self assessment. However, my salary is set (plus a variable bonus). The only reason I'm classified as a Partner is because I have significant influence over decision making. So my question is, when applying for a mortgage would I say I am self-employed even though my salary is set?

If the answer to all of the above questions is Yes, then lenders may potentially consider you as employed for the purposes of the mortgage.

But given that you’ve said you pay taxes through SA and you’re doing your first SA, I’m guessing you aren’t paid through PAYE.

The answer is no to all of them, my PAYE stopped in October when I became a Partner. So it looks like I will have to apply as self employed.

What I'm trying to get at is, given my salary is set, will a broker offer me similar terms to an employed person. Or will they just say "you're self employed so we can't offer you as big a mortgage"?

It depends on the specific lender and the specifics of your case.

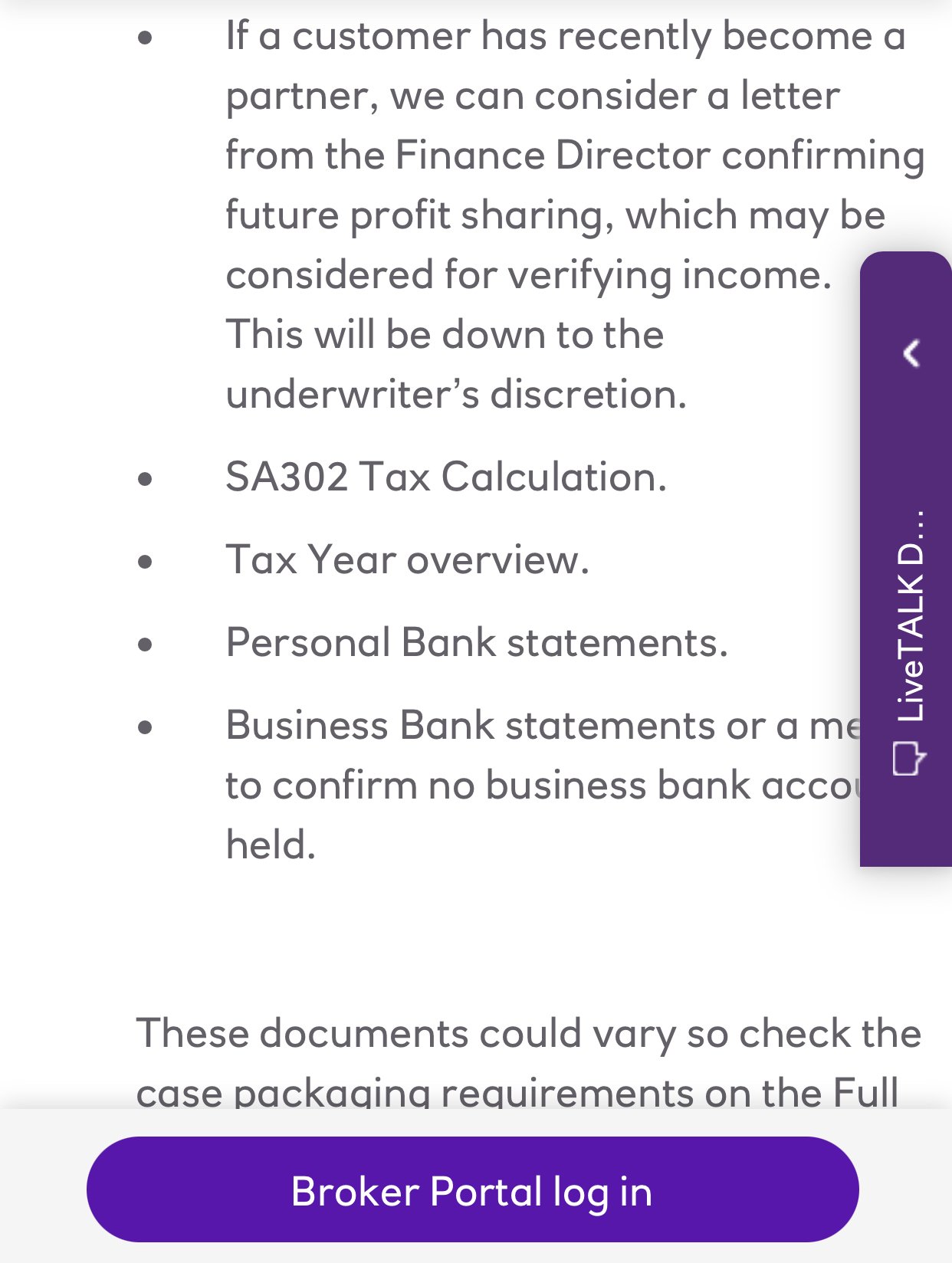

Generally speaking for a partner in an LLP, for the widest spectrum of mainstream lenders, you will need 2 years of tax-returns.

A smaller subset of mainstream lenders will consider 1 full year of tax returns.

However, some lenders may be willing to consider the case without needing a full year’s tax return subject to underwriter discretion. For example like NatWest says in its criteria here It’s a myth that self-employed people can’t borrow as much as an employed person could simply because they’re self employed. I would suggest getting a recommendation for an experienced broker from your friends/family/colleagues/LLP-partners and speaking to them. All the best!

It’s a myth that self-employed people can’t borrow as much as an employed person could simply because they’re self employed. I would suggest getting a recommendation for an experienced broker from your friends/family/colleagues/LLP-partners and speaking to them. All the best!I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

0

-

Thanks for your reply!K_S said:

@Vp0007 PAYE income from family business - this is the published evidence requirement for SantanderVp0007 said:Hey! What documents do lenders usually ask for if I am employed by a family business? (no shareholding, just PAYE employee but the business is owned by direct family). Application is with Santander. Thanks

My timeline is the following:13/03 - application submitted

13/03 - hard check carried out

15/03 - additional payslips requested and sent

20/03 - second hard check done

22/03 - valuation took place

26/03 - valuation report came back

Broker called Santander this morning and my case is due to be assessed by their underwriters tomorrow. What does this mean? Is it likely they will be asking for more docs during this state?

Thanks for your help!

") 0

0 -

@vp0007 I couldn't say tbh as it depends on the specifics of the application.Vp0007 said:

Thanks for your reply!K_S said:

@Vp0007 PAYE income from family business - this is the published evidence requirement for SantanderVp0007 said:Hey! What documents do lenders usually ask for if I am employed by a family business? (no shareholding, just PAYE employee but the business is owned by direct family). Application is with Santander. Thanks

My timeline is the following:13/03 - application submitted

13/03 - hard check carried out

15/03 - additional payslips requested and sent

20/03 - second hard check done

22/03 - valuation took place

26/03 - valuation report came back

Broker called Santander this morning and my case is due to be assessed by their underwriters tomorrow. What does this mean? Is it likely they will be asking for more docs during this state?

Thanks for your help!

Cutting out all the fluff, with family business employment what the underwriter is looking for is plausibility and a reasonable level of confirmation that the income isn't contrived and/or temporarily inflated just to qualify for a mortgage or to boost borrowing.

To make a crude comparison - an applicant working part-time in a Tesco store until 3 months ago and now on a 50k salary in the family's owned sole petrol station would trigger more scrutiny that if the applicant has been working for 3 years as a manager on 50k for a family-owned Mcdonald's franchise with 5 restaurants in/around Manchester. These are both examples of employment in a family business, but the threshold for confirmation would be very different. I hope that makes sense!I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

Thanks, that makes sense! In this case, as the valuation has already been done, would this step (assessed by the underwriters) be the last step before the mortgage offer?K_S said:

@vp0007 I couldn't say tbh as it depends on the specifics of the application.Vp0007 said:

Thanks for your reply!K_S said:

@Vp0007 PAYE income from family business - this is the published evidence requirement for SantanderVp0007 said:Hey! What documents do lenders usually ask for if I am employed by a family business? (no shareholding, just PAYE employee but the business is owned by direct family). Application is with Santander. Thanks

My timeline is the following:13/03 - application submitted

13/03 - hard check carried out

15/03 - additional payslips requested and sent

20/03 - second hard check done

22/03 - valuation took place

26/03 - valuation report came back

Broker called Santander this morning and my case is due to be assessed by their underwriters tomorrow. What does this mean? Is it likely they will be asking for more docs during this state?

Thanks for your help!

Cutting out all the fluff, with family business employment what the underwriter is looking for is plausibility and a reasonable level of confirmation that the income isn't contrived and/or temporarily inflated just to qualify for a mortgage or to boost borrowing.

To make a crude comparison - an applicant working part-time in a Tesco store until 3 months ago and now on a 50k salary in the family's owned sole petrol station would trigger more scrutiny that if the applicant has been working for 3 years as a manager on 50k for a family-owned Mcdonald's franchise with 5 restaurants in/around Manchester. These are both examples of employment in a family business, but the threshold for confirmation would be very different. I hope that makes sense!0 -

Hello, I've been told by a broker that mortgage lenders are moving away from using Experian because they're getting "too big for their boots" but are any lenders still using solely Experian?0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards