We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Mortgage broker - ask me anything

Comments

-

Thanks. I've just read that Natwest perform hard searches when using a broker. This is annoying because we were not told this during our meeting. If we went with an online broker like L&C would this be damaging to our credit file?K_S said:

@bigboss Ignore the score, just get a current copy of your Experian report and confirm that it's been corrected.BigBoss said:

Update:K_S said:

@bigboss Generally speaking, I don't think a notice of correction will help in this scenario.

Your broker may be able to guide you on what needs to be corrected but with mainstream lenders they are unlikely to be able to do anything to override errors on the report. I hope that makes sense.

- After FINALLY managing to login to Experian (drawn out complaints process etc), I see that my score with them is 999/999. This should change things massively right? I know the 'score' is generally irrelevant, but it can't be *that* irrelevant surely?

- Our prospective broker (no money down yet) searched for deals with only Transunion and Equifax reports - and got us an AIP with a high street lender (we're not happy with the amount). Could the inclusion of our Experian report change things? (my partner and I are both 999/999)

- We were also told that we should probably not submit any further searches, despite the fact that this was only supposed to be a soft search. Is this just an attempt to keep their business? Why would an AIP with a soft search stop us from submitting with another broker?

If it has, then let your broker know and share a copy of the report with them.

I'm considering using a different broker as I don't feel this one is attentive/responsive enough. We've also been mildly misled re soft/hard searches.0 -

@bigboss I don't know where you got that incorrect info about NatWest, it's outdated. NatWest broker DIPs changed from hard-checks to soft-checks at least a year ago.BigBoss said:

Thanks. I've just read that Natwest perform hard searches when using a broker. This is annoying because we were not told this during our meeting. If we went with an online broker like L&C would this be damaging to our credit file?K_S said:

@bigboss Ignore the score, just get a current copy of your Experian report and confirm that it's been corrected.BigBoss said:

Update:K_S said:

@bigboss Generally speaking, I don't think a notice of correction will help in this scenario.

Your broker may be able to guide you on what needs to be corrected but with mainstream lenders they are unlikely to be able to do anything to override errors on the report. I hope that makes sense.

- After FINALLY managing to login to Experian (drawn out complaints process etc), I see that my score with them is 999/999. This should change things massively right? I know the 'score' is generally irrelevant, but it can't be *that* irrelevant surely?

- Our prospective broker (no money down yet) searched for deals with only Transunion and Equifax reports - and got us an AIP with a high street lender (we're not happy with the amount). Could the inclusion of our Experian report change things? (my partner and I are both 999/999)

- We were also told that we should probably not submit any further searches, despite the fact that this was only supposed to be a soft search. Is this just an attempt to keep their business? Why would an AIP with a soft search stop us from submitting with another broker?

If it has, then let your broker know and share a copy of the report with them.I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

Got it from here, but they were from 2020, so you're correct!

https://forums.moneysavingexpert.com/discussion/6197839/aip-hard-search

https://forums.moneysavingexpert.com/discussion/6114876/mortgage-broker-hard-search

0 -

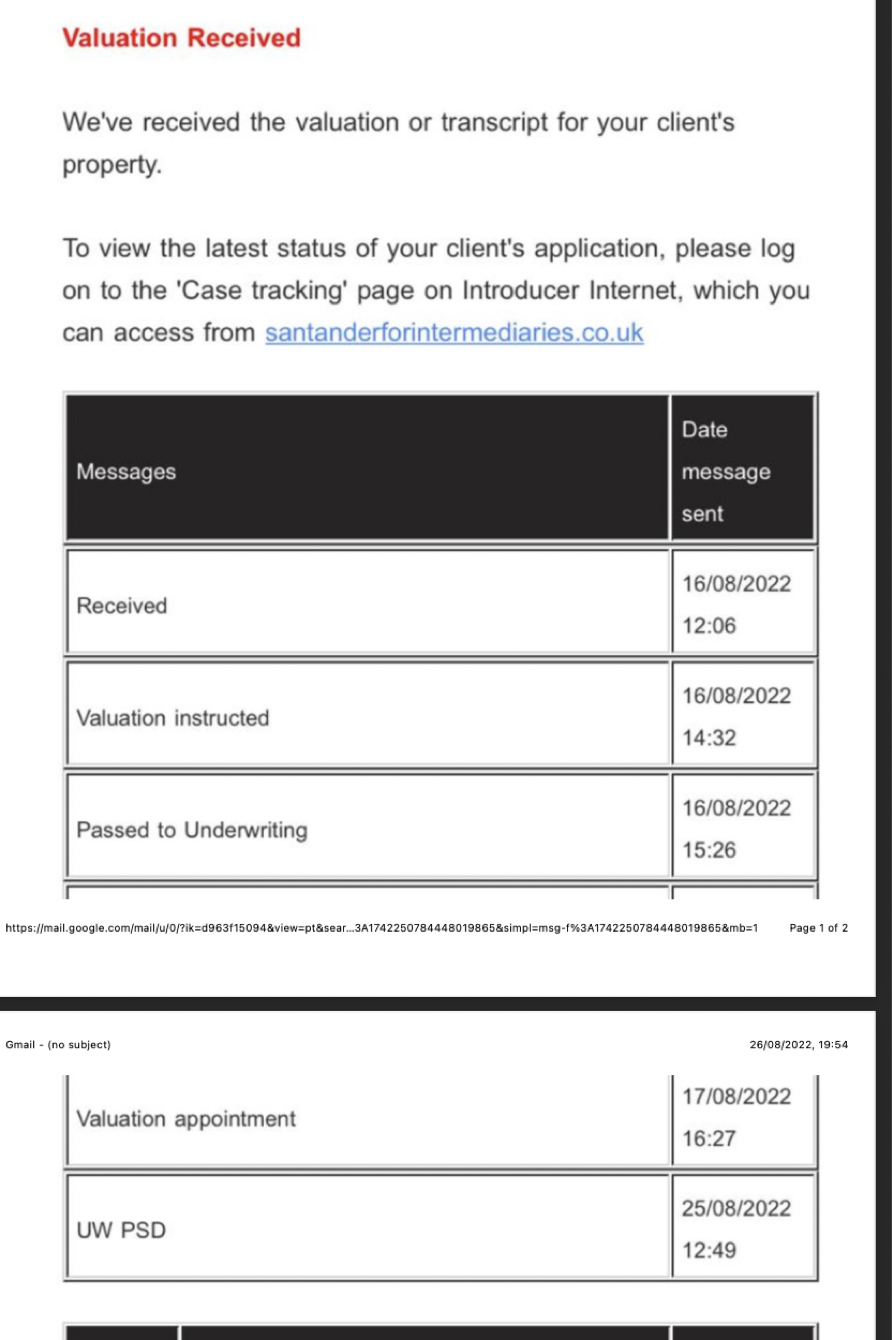

Hi

Can someone please give any insight as to what this might mean? My broker is not sure as no other information on the case.It is with Santander, but I do not know why there is no status on the valuation OR what UW PSD means?

Thanks 0

0 -

@kizzy1926 I can't recall having seen this Santander status before tbh. UW almost certainly stands for Underwriting, not sure what PSD stands for. It could just stand for 'passed', so 'Underwriting Passed' perhaps. That's just a guess.kizzy1926 said:Hi

Can someone please give any insight as to what this might mean? My broker is not sure as no other information on the case.It is with Santander, but I do not know why there is no status on the valuation OR what UW PSD means?

Thanks

It may be worth posting this query on the main forum as a separate thread as other brokers or applicants may have come across this and can answer your question.I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

We’ve had our mortgage offer and are going through conveyancing. Are we allowed to use our credit cards if we pay them off in full every month? I’m not talking about big purchases, but maybe £200 max. Thank you0

-

My parents are currently paying interest-only on their mortgage of around 180,000 (they are out of a fix so on the SVR). It is due to end in 9 years and they have no lump sum to pay off the balance. They are 67 and 62 and both are still working at the moment. Are there any re-mortgaging options available for them? I have heard some lenders will lend past retirement but can't seem to find much helpful stuff out there. It seems like such lending would only take into account their pensions so it is unlikely that they would qualify under affordability tests. They don't want to move and are considering equity release but I've heard bad things about it. Any advice on potential mortgaging options would be much appreciated. Thanks in advance.0

-

@tjjones123 A £200 spend is unlikely to be an issue unless you have completely maximised borrowing and even a tiny amount of debt will impact affordability.TJJones123 said:We’ve had our mortgage offer and are going through conveyancing. Are we allowed to use our credit cards if we pay them off in full every month? I’m not talking about big purchases, but maybe £200 max. Thank youI am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

@kimmer Unless they have a post-retirement source of income totalling up to around 40-45k+ that can be evidenced, a standard capital repayment mortgage is unlikely to be an option.kimmer said:My parents are currently paying interest-only on their mortgage of around 180,000 (they are out of a fix so on the SVR). It is due to end in 9 years and they have no lump sum to pay off the balance. They are 67 and 62 and both are still working at the moment. Are there any re-mortgaging options available for them? I have heard some lenders will lend past retirement but can't seem to find much helpful stuff out there. It seems like such lending would only take into account their pensions so it is unlikely that they would qualify under affordability tests. They don't want to move and are considering equity release but I've heard bad things about it. Any advice on potential mortgaging options would be much appreciated. Thanks in advance.

If you don't want to look at equity release, then RIO (Retirement Interest Only) mortgages might be an option. It would be worth your parents getting advice from a free later lending broker like Stepchange (it's a debt advice charity that also offers retirement mortgage advice).I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.7K Spending & Discounts

- 247.8K Work, Benefits & Business

- 604.8K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards