We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Cheapest way to invest in ISA

investin1

Posts: 6 Forumite

Looking to start investing in an ISA again. Looking to put £10k and add £1k per month for pound cost averaging (if there is a recession it will help - but starting now as no one can time the market).

Who is it best to invest larger sums with for cost.

Not looking for exciting funds. Just a FTSE ETF and a vanguard S&P500.

Ps I used to use Cavendish Online to the fund a fidelity ISA. Cavendish would then refund the broker fees and this made it very effective. Is this still true?

Would a iWeb ISA or am I barking up the wrong tree?

Thanks in advance

Would a iWeb ISA or am I barking up the wrong tree?

Thanks in advance

Landlord - 100 Club

Serviced Accommodation Operator / Estate Agent / Parent of 5

Serviced Accommodation Operator / Estate Agent / Parent of 5

0

Comments

-

These will tell you the best platforms to go for with your level of investment.

http://www.comparefundplatforms.com/

https://moneytothemasses.com/saving-for-your-future/investing/compare-cheapest-best-investment-isa-platforms

The bigger the bargain, the better I feel.

I should mention that there's only one of me, don't confuse me with others of the same name.1 -

These seem to suggest that it’s very close between all of the companies. It the fact 12 Transactions and 15 almost reverses the list.It almost makes one have analysis paralysisLandlord - 100 Club

Serviced Accommodation Operator / Estate Agent / Parent of 50 -

It is a competitive market, so inevitably there are not major differences between providers. In fact it is largely a matter of horses for courses . Also it depends on whether you want a S&S ISA, a SIPP, or a SIPP in drawdown and the exact type of investments you want to hold.investin1 said:These seem to suggest that it’s very close between all of the companies. It the fact 12 Transactions and 15 almost reverses the list.It almost makes one have analysis paralysis

Although platform charges are important they pale into insignificance compare to investment performance . I would have a good look around a few providers websites and see which one you like.0 -

The biggest differentiator for me is the quality of software from the platform and their functionality. There is no point being with the cheapest if you hate the software they use or it lacks the functionality you are after.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.0 -

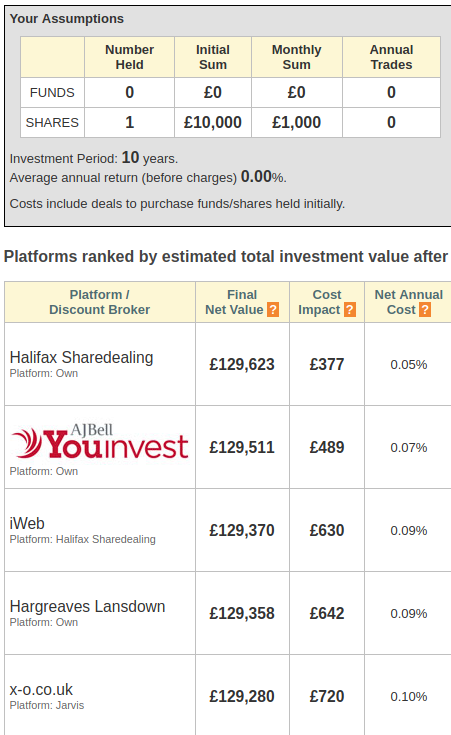

investin1 said:These seem to suggest that it’s very close between all of the companies. It the fact 12 Transactions and 15 almost reverses the list.It almost makes one have analysis paralysisSomething is very wrong with the comparefundsplatforms comparison site. See the example of putting £10k in a single ETF and then making monthly £1k buys with no other trades.iWeb: Actual cost = £25 opening fee + £5 x 12 months x 10 years = £605. Comparison says £919.Halifax Sharedealing: Actual cost = £12.50 initial purchase + £12.50 ISA admin x 10 years + £2 x 12 months x 10 years = £377.50. Comparison says £548.If the simple scenario is wrong, expanding it to two funds is no more likely to be correct.

1

1 -

It also says Fidelity do not have the facility to buy shares, which is a couple of years out of date and in fact in the scenario outlined above , they would be quite competitive.

£10 initial charge then (120 X £1.50 ) + ( 10 X £45) = £6400 -

masonic said:Something is very wrong with the comparefundsplatforms comparison site. See the example of putting £10k in a single ETF and then making monthly £1k buys with no other trades.iWeb: Actual cost = £25 opening fee + £5 x 12 months x 10 years = £605. Comparison says £919.Halifax Sharedealing: Actual cost = £12.50 initial purchase + £12.50 ISA admin x 10 years + £2 x 12 months x 10 years = £377.50. Comparison says £548.It is telling us the "Cost Impact", not the direct costs.This means ... You would be paying £377.50 to Halifax in charges. But now imagine Halifax charged nothing. How much more would the value of your final investment be? All that money not paid to Halifax (at various different dates over the 10 years of the investment) would be invested, at an assumed rate of return of 7% per annum. Hence the final value of your investment would be increased by more than £377.50, and in fact (apparently) the increase would be £548.I haven't attempted to check their calculation on that basis, but their figures look plausible to me.1

-

dont_look_now said:masonic said:Something is very wrong with the comparefundsplatforms comparison site. See the example of putting £10k in a single ETF and then making monthly £1k buys with no other trades.iWeb: Actual cost = £25 opening fee + £5 x 12 months x 10 years = £605. Comparison says £919.Halifax Sharedealing: Actual cost = £12.50 initial purchase + £12.50 ISA admin x 10 years + £2 x 12 months x 10 years = £377.50. Comparison says £548.It is telling us the "Cost Impact", not the direct costs.This means ... You would be paying £377.50 to Halifax in charges. But now imagine Halifax charged nothing. How much more would the value of your final investment be? All that money not paid to Halifax (at various different dates over the 10 years of the investment) would be invested, at an assumed rate of return of 7% per annum. Hence the final value of your investment would be increased by more than £377.50, and in fact (apparently) the increase would be £548.I haven't attempted to check their calculation on that basis, but their figures look plausible to me.Yes, it looks like that's what they are doing - adding on the opportunity cost of paying fees out of the portfolio, which can be avoided by setting growth to 0%:

Coming back to the OP's statements that "it’s very close between all of the companies" and "12 Transactions and 15 almost reverses the list" I'm not sure what numbers are being fed in to produce that result, but I see a very clear difference between providers that is maintained across small changes to number of shares / number of trades.0

Coming back to the OP's statements that "it’s very close between all of the companies" and "12 Transactions and 15 almost reverses the list" I'm not sure what numbers are being fed in to produce that result, but I see a very clear difference between providers that is maintained across small changes to number of shares / number of trades.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards