We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Vanguard Life Strategy Minimum Investment

Comments

-

That's interesting, thank you. I may take a look into Vanguard's Global Equity Fund.AnotherJoe said:Here's an argument why buying lifestrategy with their artificial 25% loading of "UK" companies may not be a good idea and you'd be better with a more global fund

0 -

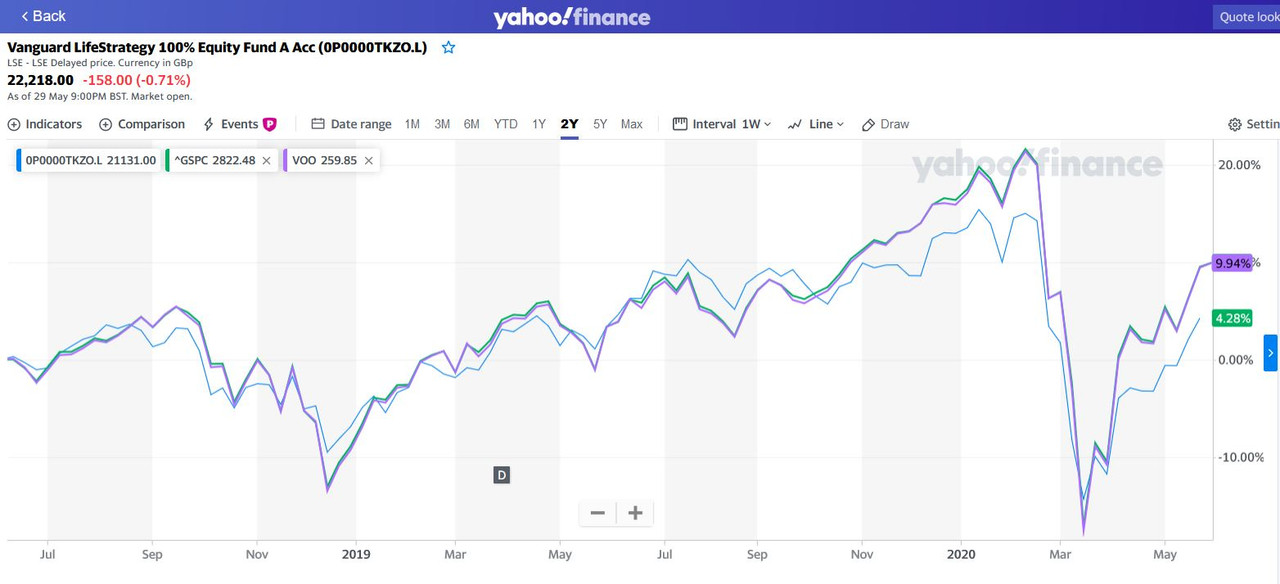

Vanguard Life Strategy 100% equity vs Vanguard S&P 500 ETF (VOO)OCF: For life strategy 100 Equity is 0.22% Vs Vanguard S&P 500 ETF (VOO) is just 0.07%PerformanceAccidentally I compare Vanguard S&P 500 ETF (VOO) with Vanguard Life Strategy 100% Equity by overlaying it on yahoo finance over the two years period it seems to me thatVanguard S&P 500 ETF (VOO) beats Vanguard Life strategy 100% most of the time.Vanguard Life strategy 100% seems very popular here in MSE, It makes me wonder, why people want to invest in Vanguard Life strategy 100% equity if they could do better and cheaper with Vanguard S&P 500 ETF (VOO) ?Is there any good reason to favour Vanguard Life strategy 100% over h Vanguard S&P 500 ETF (VOO) ?Any hint explanantion of this will be very much appreciated ....

0 -

You're comparing apples with oranges - VLS100 is a widely-diversified fund of funds including equities from around the world, with its composition explained at https://www.vanguardinvestor.co.uk/investments/vanguard-lifestrategy-100-equity-fund-accumulation-shares/portfolio-dataadindas said:Vanguard Life Strategy 100% equity vs Vanguard S&P 500 ETF (VOO)OCF: For life strategy 100 Equity is 0.22% Vs Vanguard S&P 500 ETF (VOO) is just 0.07%PerformanceAccidentally I compare Vanguard S&P 500 ETF (VOO) with Vanguard Life Strategy 100% Equity by overlaying it on yahoo finance over the two years period it seems to me thatVanguard S&P 500 ETF (VOO) beats Vanguard Life strategy 100% most of the time.Vanguard Life strategy 100% seems very popular here in MSE, It makes me wonder, why people want to invest in Vanguard Life strategy 100% equity if they could do better and cheaper with Vanguard S&P 500 ETF (VOO) ?Is there any good reason to favour Vanguard Life strategy 100% over h Vanguard S&P 500 ETF (VOO) ?Any hint explanantion of this will be very much appreciated ....

One of its constituents is a 13.9% stake in an S&P 500 tracker, which obviously only tracks that specific index.

Investors wanting global diversification would favour VLS100 (or comparable products), whereas those wanting to track one American index might choose the S&P 500 fund....4 -

eskbanker has already given a hint of an explanation.adindas said:Vanguard Life strategy 100% seems very popular here in MSE, It makes me wonder, why people want to invest in Vanguard Life strategy 100% equity if they could do better and cheaper with Vanguard S&P 500 ETF (VOO) ?Any hint explanantion of this will be very much appreciated ....

As a simple reason for the disparity, looking at figures for the five years to end of April (just using April because while LifeStrategy has updated their factsheet for May, the FTSE published factsheets for other indexes haven't been updated yet).

- if you look at the FTSE Developed Large Cap index (which allocates its money to the biggest listed companies in the developed world by their size and free float), it delivered a total return of 33.7% over the five years to the end of April (6% a year annualised);

- if you look at the FTSE Developed Large Cap Ex-US index (which does the same except excludes the US), it delivered a total return of only 1.5% (0.3% a year annualised)

- if you look at the FTSE US TM Large Cap index (which allocates its money to the biggest ~250 listed companies in the US, making up $21 trillion of the $24 trillion covered by the S&P500), total return was 59.7% (9.8% annualised).

If you invest in the S&P 500 you are only getting large US companies, and so you would have got a very good result. Whereas if you invested outside the US, using a tracker to weight your money to the biggest companies, you would have got a much lower result. As it happens, emerging markets also fared worse than developed ones in this particular period (Global large cap 30% vs the Developed large cap 33.7% mentioned above).

If you invest in a LifeStrategy fund-of-funds which spreads its money over all major markets of which US is just one (and is a product which, compared to a world tracker, under-weights the US and other countries to increase the UK weighting), then over the last five years you would clearly have had a worse result than just picking an index that tracks the US market, which was the market that happened to do the best.

If the returns were close to 0% a year outside the US market, almost 10% a year for the US market, and 6% a year if you put most of your money in the US market, then it seems like a great idea to put most of your money in the US market, and heck, why not just put all of it there - because it's the best? However, making investment decisions is not about what you would have got if you had a time machine and could go back and pick the winner. It's not true that the US 'gets' 10% a year. It's simply true that the US 'got' 10% a year, past tense. If you went back a decade or so, and then looked at a chart of the decade before that, it was not showing that the US is best. Lots of different markets will take their turn at being the best for a bit.

So instead of looking back, investing is about looking forward from now and buying an appropriate investment.

If US had delivered the 0 or negative result and other markets delivered the positive results, you would be looking at the chart and thinking why would someone invest in the S&P when they could just invest in a more balanced investment with a mix of companies from around the world. Someone would look at that bad result for the S&P and think, hmm I was really stupid to just put all my money into one stockmarket and ignore the rest. But as it happens, the S&P was best this time so people are looking at it and thinking, hmm, why didn't I put all my money into that one stockmarket and ignore the rest.

1 -

adindas said:Vanguard Life Strategy 100% equity vs Vanguard S&P 500 ETF (VOO)OCF: For life strategy 100 Equity is 0.22% Vs Vanguard S&P 500 ETF (VOO) is just 0.07%PerformanceAccidentally I compare Vanguard S&P 500 ETF (VOO) with Vanguard Life Strategy 100% Equity by overlaying it on yahoo finance over the two years period it seems to me thatVanguard S&P 500 ETF (VOO) beats Vanguard Life strategy 100% most of the time.Vanguard Life strategy 100% seems very popular here in MSE, It makes me wonder, why people want to invest in Vanguard Life strategy 100% equity if they could do better and cheaper with Vanguard S&P 500 ETF (VOO) ?Is there any good reason to favour Vanguard Life strategy 100% over h Vanguard S&P 500 ETF (VOO) ?Any hint explanantion of this will be very much appreciated ....You've made an unwarranted jump of logic in at least two respects.First, you've confused future and past tenses. The fact that over the last two years S&P500 happened to beat Global does not mean " .. beats most of the time" (which is you now making that historical performance a prediction of the future).It just means "it beat it in that 2 year historical period that's now over, we dont know what will happen next two years".Second, one could come up with 50 other indices that beat the S&P500 and Global over those two years. But thats cherry picking, looking backward. Indeed why indexes, why not companies if you have the luxury of a time machine?Why not just have bought Tesla, Apple or Netflix and ask "why does anyone buy S&P500 when Tesla/Apple/Netflix beats S&P500 most of the time?" .3

-

I understand the explanation here is that:

- Comparing Apple and Orange as they have different portfolio. Vanguard Life Strategy 100% Equity is a more globally diverse portfolio while S&P 500 is more US weighted. So Vanguard Life Strategy 100% Equity is likely carrying less risk.

- Past performance is not a good indicator for the future performance.

- Two years comparison is too short to be used as a good indicator. Indeed, in the Past Vanguard Life Strategy 100% Equity did win.

I herewith provided the past two years comparison Image:

https://i.postimg.cc/g2Cx8vBV/2-Years.jpg

I understand the index fund is not very volatile so you will have time to take action it if you keep watching it.

Currently majority of my investment is with Vanguard Life Strategy 100% Equity. Vanguard S&P 500 ETF performance is outperforming Vanguard Life Strategy 100% Equity with lower fee and it will stay like that at sometimes might be months.

So, I intend to sell all Vanguard Life Strategy 100% Equity and buy the Vanguard S&P 500 ETF from the same vanguard platform. I understand there is no fee of doing this (?).

I keep my eye a few days a week until I see the line is crossing where Vanguard Life Strategy 100% Equity start to outperform Vanguard S&P 500 ETF and I will be switching it back to Vanguard Life Strategy 100% Equity at that point.

What do you think with this plan? Your input and critics on this strategy is very much appreciated.

0 -

Yes, sometimes specialist investment A will outperform the diversified generalist investment B.adindas said:I understand the index fund is not very volatile so you will have time to take action it if you keep watching it.

Currently majority of my investment is with Vanguard Life Strategy 100% Equity. Vanguard S&P 500 ETF performance is outperforming Vanguard Life Strategy 100% Equity with lower fee and it will stay there at sometimes might be months

Sometimes, specialist investment A will underperform the diversified generalist investment B.

If you want to gamble to get the best possible result, you could buy the specialist fund A, taking also the risk that it will give you the worst possible result. It can underperform for months or years. Or it can stay there outperforming for months too. You don't know whether the next month will be the one in which it outperforms or underperforms. You have just looked at the last few years when it did better, not the 10-20 years ago when it did worse, so you are saying 'it's doing better at the moment' - but you don't know whether it will do better or not for the next day, week, month or year or decade.

You say it is not very volatile so you will have time to take action if you keep watching it. It can fall 20% in a matter of days or weeks. How are you going to 'keep watching it' and know whether it will do better or worse in the next day, week, month or year coming, when those days weeks months years haven't happened yet, and know when to switch to something else? Are you psychic? By the time you watch it and find out that it has been doing worse than some other index for a day, week, year, decade, you have already missed the chance to sell it before it did worse. But you still won't know whether the next day, week, year, decade will be better.I keep my eye a few days a week until I see the line is crossing where Vanguard Life Strategy 100% Equity start to outperform Vanguard S&P 500 ETF and I will be switching it back at that point.It is a nonsense plan, because it relies on you watching it get a worse result than something else while you hold it, and then you have already got the worse result. And then you are going to buy that other thing instead. The 'fear of missing out' will cause you to keep jumping into the thing that has just performed well before you get there, missing those gains, rather than buying and holding something that performs just fine.

What do you think with this plan? Your input and critics on this strategy is very much appreciated.

It is like being in a traffic jam on the motorway and every time you get overtaken by ten cars from the lane next to you, you move into that lane because it's 'winning', and then when ten cars in the original lane overtake you, you move back into that other lane because it's now winning. In doing so, you are now perhaps 5 or 10 cars further back in your original lane. You should have just kept your original lane, which is moving at its own pace towards a realistic goal. Being jealous of other cars or other specialist investment funds is all good fun until they crash and you are glad you didn't gamble on them always being the winner.3 -

Yes these are just the limits for the opening payment. You can then reduce to whatever you want. When I spoke to them to double check, they said they get this query all the time.

1 -

What is odd is why they don’t update their FAQs to reflect this kind of regular query. Their FAQs are minimal almost to the point of unhelpfulness.CityLights said:Yes these are just the limits for the opening payment. You can then reduce to whatever you want. When I spoke to them to double check, they said they get this query all the time.0 -

They don't charge you any fees to open an account or do investment transactions on it. They make money from your money being invested with them, an overall percentage of how much you've got invested.Keith80 said:

What is odd is why they don’t update their FAQs to reflect this kind of regular query. Their FAQs are minimal almost to the point of unhelpfulness.CityLights said:Yes these are just the limits for the opening payment. You can then reduce to whatever you want. When I spoke to them to double check, they said they get this query all the time.

In common with other platforms, if they're going to go to the trouble of admitting you to a fund and having shares issued to you, they would like you to do it in meaningful amounts, like £500, or by signing up to £100 a month:

Putting in at least £500 would mean that by the end of the year the investment platform will have earned (at 0.15%) at least 75p in platform fees from you to help cover the work done in establishing and maintaining your account and dealing with your share of the periodic dividends or corporate actions etc. If you actually call up and have a ten minute conversation with one of their team, or there is some query with a cash transfer or identity checks or a failed debit card transaction etc, they have spent enough money to cover a decade of fee income on the £500 investment. Meanwhile over the course of that first year the part of their group that acts as the fund manager will have earned maybe £0.5-£1 towards the costs of running the fund including management fee income.

Alternatively, if you committed £100 a month, by the end of the year you'd have £1200 in there, with the average balance for the year being a little over £600 and so the platform fee would still be less than a pound, but at least they are on track to make some money in the future if you keep adding to the investment with your monthly direct debit.

If you are asking "why don't they just advertise through their FAQ that once you get 'on the books' with one of their investments you can add really small amounts to it if you like", the answer is that they would prefer you not to reduce your investments - they want more from you and not less. They want to be cheap to access for all, but that doesn't mean they want to give away their services for nothing and have people investing nominal amounts. Every transaction is an incremental piece of work which statistically may lead to a query, and £25 transactions that earn them fourpence over a year are just a potential pain in the bum.

You may be thinking "a true MSE would game the system and put in £100 just to make the minimum and then maybe not even add to that fund ever, but still get a fully functioning website, online and annual statements, tax reports (to the customer or to HMRC or both), customer service helpline, compliance and legal services and a bunch of non client-facing staff in the background doing accounting, marketing etc, all for a pound or two per year. But sensible businesses aren't going to issue a FAQ saying "here's how you can avoid our minimums and invest less money with us".2

{kind=link}

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards