We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Want to become a Forum Ambassador? Visit the Community Noticeboard for details on how to apply

Safe fund beating savings accounts?

sebtomato

Posts: 1,120 Forumite

Hi,

I am only getting 1.2% or 1.3% on my savings currently.

Are there any investment funds (preferably available via HL or Vanguard) that can beat those savings rate (e.g. 2%) while staying fairly safe with the capital?

Any recommendations on some safe funds?

Thanks

I am only getting 1.2% or 1.3% on my savings currently.

Are there any investment funds (preferably available via HL or Vanguard) that can beat those savings rate (e.g. 2%) while staying fairly safe with the capital?

Any recommendations on some safe funds?

Thanks

0

Comments

-

No fund offers guaranteed returns.

No fund is 100% safe.

2 -

There aren't any 100 % safe funds. You need to assess your capacity and attitude to risk and allocate between savings and investments accordingly. If it's saving for a house, or you need in in the next <5-7 years, then you need to stay in savings accounts fully backed by FSCS or Treasury. If you don't need the money for 10 years, then the savings accounts are arguably more risky, as you know inflation is going to eat around 1% of their value every year.

"Real knowledge is to know the extent of one's ignorance" - Confucius1 -

You could also consider going 50-50, that is, keeping 50% in savings accounts for "safety" and investing 50% to improve the average return. Or whatever split you feel comfortable with.1

-

Yes, I know no funds are as safe as savings accounts.

However, some funds are more risky than others, and some funds must have performed well during the recent crisis while still giving small returns (e.g. 2% pa).

I am ideally looking for something that doesn't swing too much, and has moderate returns above savings account.

I already have a lot of riskier stock market investments, but currently with £50K of cash sitting on savings account earning basically nothing. I don't need that much in short term access.0 -

You clearly don't understand, there is NO magical fund like you are seeking, don't you think everyone would be investing there if there was?!?!?sebtomato said:Yes, I know no funds are as safe as savings accounts.

However, some funds are more risky than others, and some funds must have performed well during the recent crisis while still giving small returns (e.g. 2% pa).

I am ideally looking for something that doesn't swing too much, and has moderate returns above savings account.

Stick with the 1.2 or 1.3 % that you're getting and research investing until you understand the risks and accept there is no fund that will guarantee you a better rate than your savings accounts.2 -

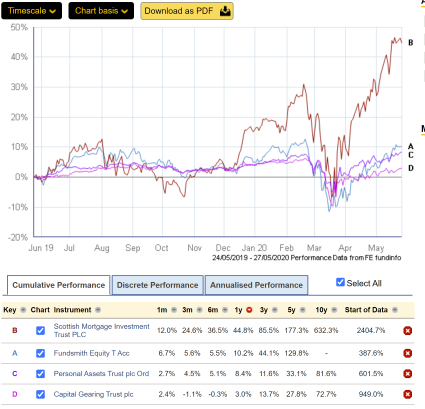

Many funds are up more than 2% over the last 12 months.sebtomato said:Yes, I know no funds are as safe as savings accounts.

However, some funds are more risky than others, and some funds must have performed well during the recent crisis while still giving small returns (e.g. 2% pa).

I am ideally looking for something that doesn't swing too much, and has moderate returns above savings account.

This includes

- the IA Global sector as a whole, at +5.5%,

- conviction driven 'big brand' investors such as Fundsmith (+10.2%)

- high conviction growth investors such as Scottish Mortgage Investment Trust (+44.8%)

- investment trusts with a capital preservation remit such as Capital Gearing Trust or Personal Assets Trust (3% and 8.4% respectively)

Of course, we know that Fundsmith or Scottish Mortgage could lose 50%+ in a bad couple of years (SMT has lost 70%+ in the past), while it is unlikely that CGT or PNL would do likewise (10-15% NAV drop at the worst of the market turmoil this March). We also know that it is difficult to predict the shape or duration of the next piece of market turmoil and if a 30% drop is not preceded by a 50% rise, or a drop does not recover but flatlines at a low level for a sustained period, then investors could have a Very Bad Time (tm).

So, the fact that some funds performed well during the recent phase of choppy markets does not mean they will do equally well with the next one, or that they will need to wait any more than a few months for the next one. It would likely be foolish to try to increment a 1% savings rate by an extra percent or so, and lose 10% in the process.

Cash and short dated gilts are not paying 2%. The underlying assets which can give 2-3% yields are subject to 10%+ capital loss. For a better chance of obtaining the 2-3% from underlying assets, you would blend together a range of different holdings including the aforementioned cash and shortdated gilts that return nothing, with higher risk bonds that hopefully return something and other asset classes that could return more (equity, infrastructure projects, real estate) but might not, and hope that the mix of different asset classes were not too well-correlated so that they did not all crash at the same time. In doing so you would have a mixed bag of risk and while you would expect to beat inflation over the long term you would risk losing 10-20% over shorter (but perhaps multi-year) periods.

So, the 'safe boost to my savings interest rate without taking much risk' does not exist.

recent harts of the above mentioned funds fyi. Past performance not to be assumed to repeat in future etc.

5 -

Don't forget that even were you to find that mythical safe fund that returned 2%, HL and Vanguard will charge you a platform fee of 0.45% or 0.15% thus reducing the return

3 -

RCI bank are offering 1.8% on a 5 year fixed rate , which is about as close as you will get to what you want.0

-

How depressing. So to have a chance to earn 2 or 3% returns per annum nowadays, you need to be willing to have capital going down by 10%??

What's left for investors?

0 -

Thanks, but I don't want my "savings" to be stuck for 5 years just to earn 1.8%. Doesn't seem to be a good return.Albermarle said:RCI bank are offering 1.8% on a 5 year fixed rate , which is about as close as you will get to what you want.

If I wanted to lock the money down for 5 years, I think I would just drip feed into the stock market, and probably would have a high chance of earning the same amount (or more).0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.9K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 246.9K Work, Benefits & Business

- 603.5K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards