We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

10 years of stock growth wiped?

Comments

-

moneysaver2x said:

Which companies would you invest in?Kendall80 said:Once the 'bottom' is reached you could probably put your money anywhere and achieve excellent results. If only one could find the bottom. Instead, I will be dripping in extra and keeping some available for further large drops.

I wouldn't invest in single companies. I learned that painful lesson early on fortunately. To answer your question, it would be a world tracker or VLS 100 - if I had my crystal ball enchanted with bottom-finding elixir.

0 -

I can relate to that! at least when things like this happen in stocks you can buy more, unlike P2P when it goes wrong!keyboardworrier said:I'm remarkably calm about the whole thing. I think being involved in P2P has given me a flavour of what real risk is!

1 -

Now is not the time to be in P2P at all.takesyourchances said:

I can relate to that! at least when things like this happen in stocks you can buy more, unlike P2P when it goes wrong!keyboardworrier said:I'm remarkably calm about the whole thing. I think being involved in P2P has given me a flavour of what real risk is!3 -

Which world index do you recommend? My broker is HL and the only one they list is HSBC which has a 0.20% annual fee.Linton said:You are ignoring 2 important factors1) Dividends. If you reinvested the dividends, which is probably what would have happened had you bought a tracker, you would still be 40% up.2) Investing solely, or even mainly, in the FTSE100 would be poor investing. If you had invested in the FTSE World Index with reinvested dividends over the past 10 years you would still be up 140%.0 -

You had a thread of your own on this subject but poo pood the responses. So, why are you asking again if you didnt like the comments first time around?CreditCardChris said:

Which world index do you recommend? My broker is HL and the only one they list is HSBC which has a 0.20% annual fee.Linton said:You are ignoring 2 important factors1) Dividends. If you reinvested the dividends, which is probably what would have happened had you bought a tracker, you would still be 40% up.2) Investing solely, or even mainly, in the FTSE100 would be poor investing. If you had invested in the FTSE World Index with reinvested dividends over the past 10 years you would still be up 140%.I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

Fidelity Index World P is 0.12% charge, I think this is the cheapest global tracker (But am not 100% sure about that...)

0 -

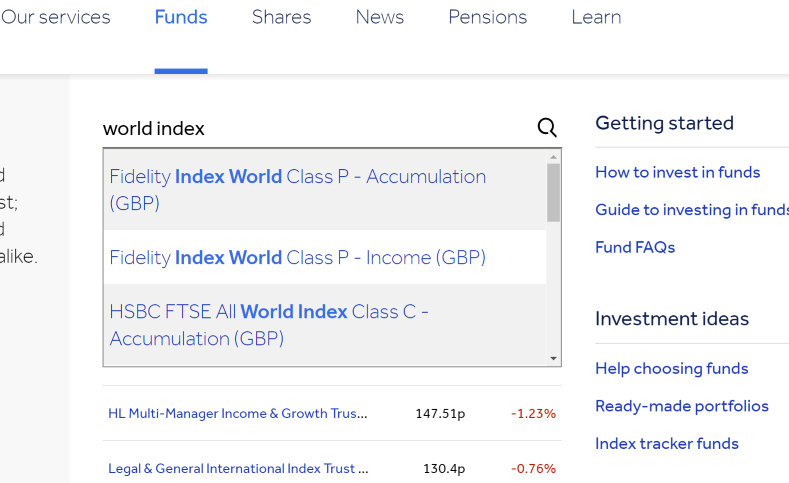

It's not really true that that's the only one they list (in fact it isn't one they even promote in their 'Wealth 50'. For examples of others they sell, see the screenshot below for a bunch of tracker funds holding global equities, found through the URL at the top of it. Via HL you also have access to loads of ETFs listed on the London stock exchange, which gives you many more others to choose from.CreditCardChris said:

Which world index do you recommend? My broker is HL and the only one they list is HSBC which has a 0.20% annual fee.

0 -

Oh thank you. I just searched for "world index" in the funds search field and it only returned HSBC and some other fidelity one that only had a fund market cap of £60million so not that popular. Their wealth 50 funds are a bit scammy though, very high fees for essentially the same tracker? I think they just put that little green star next to it to make people think the performance is better than a normal index tracker?bowlhead99 said:

It's not really true that that's the only one they list (in fact it isn't one they even promote in their 'Wealth 50'. For examples of others they sell, see the screenshot below for a bunch of tracker funds holding global equities, found through the URL at the top of it. Via HL you also have access to loads of ETFs listed on the London stock exchange, which gives you many more others to choose from.CreditCardChris said:

Which world index do you recommend? My broker is HL and the only one they list is HSBC which has a 0.20% annual fee.0 -

Thrugelmir said:

Now is not the time to be in P2P at all.takesyourchances said:

I can relate to that! at least when things like this happen in stocks you can buy more, unlike P2P when it goes wrong!keyboardworrier said:I'm remarkably calm about the whole thing. I think being involved in P2P has given me a flavour of what real risk is!

I'd concur growth street who I used to use sent an email this evening, there's no issues with the loans but due to the large number of withdrawals they're now halting withdrawals. Long term will probably be fine, but short term liquidity could be problematic

0 -

CreditCardChris said:

Oh thank you. I just searched for "world index" in the funds search field and it only returned HSBC and some other fidelity one that only had a fund market cap of £60million so not that popular.bowlhead99 said:

It's not really true that that's the only one they list (in fact it isn't one they even promote in their 'Wealth 50'. For examples of others they sell, see the screenshot below for a bunch of tracker funds holding global equities, found through the URL at the top of it. Via HL you also have access to loads of ETFs listed on the London stock exchange, which gives you many more others to choose from.CreditCardChris said:

Which world index do you recommend? My broker is HL and the only one they list is HSBC which has a 0.20% annual fee.

I didn't believe you so I tested it myself.

Here is the screenshot. If you click on the Fidelity fund and scroll down to fund size, it shows a fund size of £1.526m

So, over one and a half billion. I agree 60 million would not be a big fund, but £1,526 million is over 25 times that size.

Also in the screenshot to the right of the search under 'investment ideas' you can see there is a dedicated link for 'Index tracker funds'. If you go to that page you'll see the table of tracker funds that they include in the Wealth 50, which they show you first, but below that there is a search box with a big heading "Search for index tracker funds" and below the search box there's the text "VIEW ALL INDEX TRACKER FUNDS" which gives you a long list, and my earlier screenshot showing 25+ options was just a small extract of that list (the ones they grouped under the Global heading). So they are not hiding anything from you.Their wealth 50 funds are a bit scammy though,

Wealth 50 is a marketing list. They are the funds they want you to buy as they have negotiated better fee rates for sending large volumes of customers to those managers, which cuts your cost of investing so that you won't mind paying their high platform fees. However, the wealth 50 index tracker funds which you find by following the 'index tracker funds' link do not appear particularly 'scammy'.a bit scammy though, very high fees for essentially the same tracker?Your comment about 'very high fees for essentially the same tracker' doesn't really make any sense. The HSBC FTSE All-World tracker that you were able to find yourself has an ongoing charges figure of about a fifth of a percent, as you mentioned (declared OCF is 0.19%). That's relatively cheap for a world tracker with lots of holdings across all developed and emerging markets. So how much more expensive are the ten tracker options on the Wealth 50 list?

If you look down the list of Wealth 50 trackers, there is not a single one of the ten that costs any more than 0.16% net of discount. The L&G International Index is discounted to 0.08%, and you could combine it with an L&G UK index (0.04%) and an iShares Emerging Markets index (0.16%) in the same proportions as the All-World index so that you had built your own portfolio for less than 0.09%. There would be some extra effort needed on your part to maintain the proportions between those three components. But it doesn't mean 'very high fees for essentially the same tracker', at all.I think they just put that little green star next to it to make people think the performance is better than a normal index tracker?They don't say the performance is any better than a normal tracker. They say, "To help narrow down the choice we have selected our favourite tracker funds across the major sectors." And the funds they selected as their favourites all have discounted fees to a level of 0.16% OCF (for emerging markets) down to 0.04% for UK and 0.06% for US with 0.08% for developed world ex-UK.

The bigger issue is that the fee they charge to hold any open-ended fund is subject to a platform fee of 0.45% which may be two to three times the amount of money you're spending on the fund itself. But it doesn't make any sense for you to decide to use HL (which has pretty much the the highest percentage-based fees of any platform on the market) and then complain that their Wealth 50 tracker funds are 'a bit scammy, high fees' when they are pretty much the lowest OCF of any funds on the site.

It seems that despite creating 50+ threads here over the last 18 months to ask about stuff, you have a habit of ignoring the answers or giving up on the thread, or just borrowing a soundbite or two to use later. You don't really give the impression you know what you're looking at, or what many of the terms or concepts mean. Still, good luck with it.

5

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards