We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Regular Savings Accounts: The Best Currently Available List!

Comments

-

'could earn' does not mean 'will earn'.Bigwheels1111 said:

It looks like it says £136.50 to me.gt94sss2 said:

You do realise the T&C don't actually say that?Bigwheels1111 said:jameseonline said:

Have asked them on chat they saying I'm not out of pocket, interest has been paid correctly etc.Bigwheels1111 said:

Ask for your £1.12, they will give it to you.jameseonline said:Just cashed out my First Direct Regular Saver £3735.38, so £3600 + £135.38 interest, not bad but not best either, it's advertised as £136.50 interest though, does say based on paying 1st of each month though but yeah.

Still it's better than last year's amount of £3710.44.

Also when did First Direct get push notifications?, took them long enough.

Although it's not much more so no great loss & more money may end up going into the poopy savings account anyway, last year an extra 66p ended up in it. 😁I just called them as said, your T&C state £136.50, why did I not get that.

So I pulled them on it.

I will pull them again in 12 months.

Plus on Monday, as used the wife’s account to get a second R/S she got paid even less than me. 3

3 -

I decided to hold off funding mine for now. I have all my non-ISA EA savings (barring accounts with minimum balances) at 5.5%+ now so the account is only one I'm opening speculatively.Gers said:@allegro120 - I've opened this account and deposited funds, it's showing as 5.2% in the app. No appointment made.

Skipton are one of those building societies where the account term starts on the date you make your first deposit rather than the date you apply for the account so by waiting a bit before making a deposit I can push the end date for the bonus rate on a bit.4 -

Ditto, although the app shows "Next interest due" as 12 May 24?Gers said:@allegro120 - I've opened this account and deposited funds, it's showing as 5.2% in the app. No appointment made.

PS : Off topic, not about a Regular Savings Account.....0 -

Another 3.8% here (both on App and funding confirmation (below)) with the next interest showing as 11/5/25.allegro120 said:

I can confirm it. I've opened the account, deposited £1 and the interest displays as 3.8%. I'll check tomorrow to see if it changes, but it looks to me like you need to make an appointment to get 5.2%.masonic said:

Yes, if you've agreed to have an appointment with one of their FAs, then they can offer you the account. Perhaps you'd be able to open the account without having such an appointment in place, but should expect a call to set one up.pokemaster said:

To me that reads as “if”SonOfPearl said:

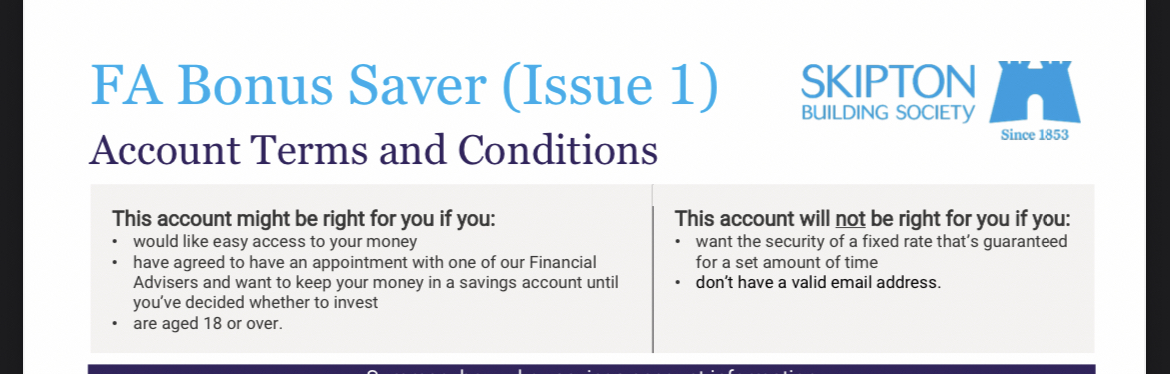

The T&C for the Skipton FA Bonus Saver states that you need to "have agreed to have an appointment with one of our financial advisers". That's a big no from me then. It's not worth the hassle for a 5.2% variable rate for six months when I currently have several accounts still paying 5%+ anyway.simonsmithsays said:

Even better is that Skipton are also offering a FA Bonus Saver which is easy access and pays up to 5.2% for six months variable (3.8% after that).gt94sss2 said:

Skipton's default rollover option for this account is a 3.8% "matured saver" instant access account

As one of the account holders who haven't closed this early (and then opened up the 7% RS) I see that upon logging into the app I see the following

Your account is due to mature on 31 May 2024.

We'll let you know about your maturity options around two weeks before your account maturity date'

They are also offering a 4.5% one year bond or you can switch to any of their other products available on the 1st June.

The maturity email doesn't list the app as a method of providing maturity instructions, but you can do so online, via email, post, webchat etc

If you want to open a new RS, you need to open a new account from 1st June

You'll see this option when you login online to complete your instructions and click on Full savings range available online

1

1 -

This is mine.

This is mine.

1 -

I assume the accounts showing 3.8% had a debit card deposit, and those showing 5.20% received an internal transfer (or possibly via faster payments) ?

0 -

True (FP).janusdesign said:I assume the accounts showing 3.8% had a debit card deposit, and those showing 5.20% received an internal transfer (or possibly via faster payments) ?1 -

flaneurs_lobster said:

True (FP).janusdesign said:I assume the accounts showing 3.8% had a debit card deposit, and those showing 5.20% received an internal transfer (or possibly via faster payments) ?

Mine was FP too.

1 -

I'm assuming that now I've opened (and funded) this account I'll get communication inviting me to make an appointment with their FA. Ignoring or refusing the request might mean account closure and return of funds (or it might mean nothing happens at all).Bridlington1 said:

For now I'll interpret it to mean that you can open it if you have an appointment with one of their financial advisers but this is not a requirement. I've just tried applying for the account online using a guessed application link and was successful in my efforts. My new FA Bonus Saver Issue 1 now sits awaiting funding in online banking.Further down the T&Cs it says this, which sounds very much like a requirement:

ETA application link:

https://secure.skipton.co.uk/portal/NewAccount/28105

However the Skipton FAQ's say "Our financial advice service could be right for you if you have at least a lump sum of £20,000 or £500 on a monthly basis." so it could be a very short meeting.

It's an original and interesting marketing pitch, bit better than the usual "would you benefit from a financial health check" that NWG have been punting at me for the last umpteen years.0 -

I took this option to open an FA Bonus Saver account with the funds from my maturing Members Regular saver at the end of the month. If I get a query from Skipton about why there's no appointment booked, I will point out that I've already had the meeting - it was about thirty years ago and have no wish to have another! And I'll not hesitate to tell them that their "advisor" was arrogant and unhelpful - I learned nothing new.flaneurs_lobster said:

I'm assuming that now I've opened (and funded) this account I'll get communication inviting me to make an appointment with their FA. Ignoring or refusing the request might mean account closure and return of funds (or it might mean nothing happens at all).Bridlington1 said:

For now I'll interpret it to mean that you can open it if you have an appointment with one of their financial advisers but this is not a requirement. I've just tried applying for the account online using a guessed application link and was successful in my efforts. My new FA Bonus Saver Issue 1 now sits awaiting funding in online banking.Further down the T&Cs it says this, which sounds very much like a requirement:

ETA application link:

https://secure.skipton.co.uk/portal/NewAccount/28105......

0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards