We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

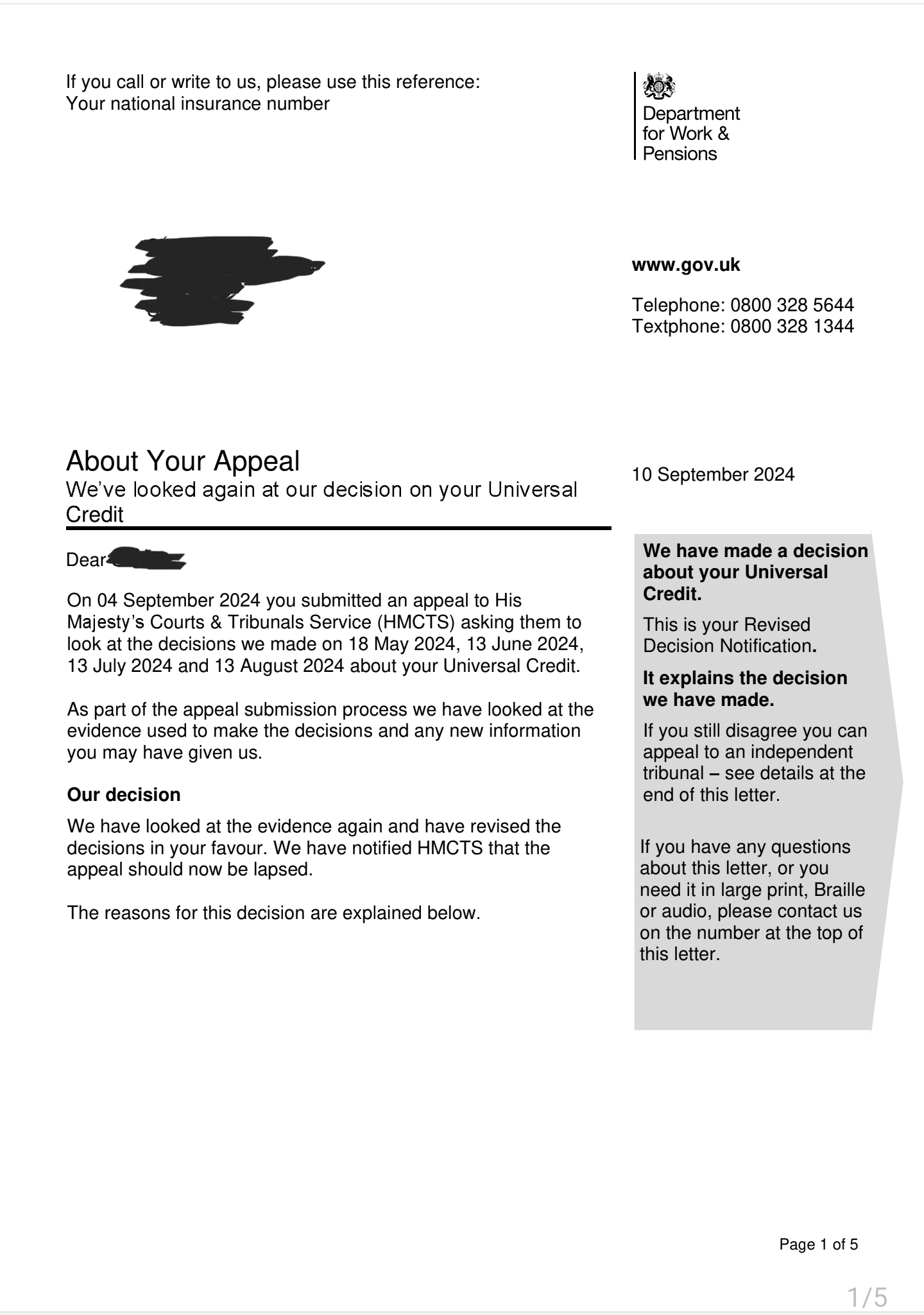

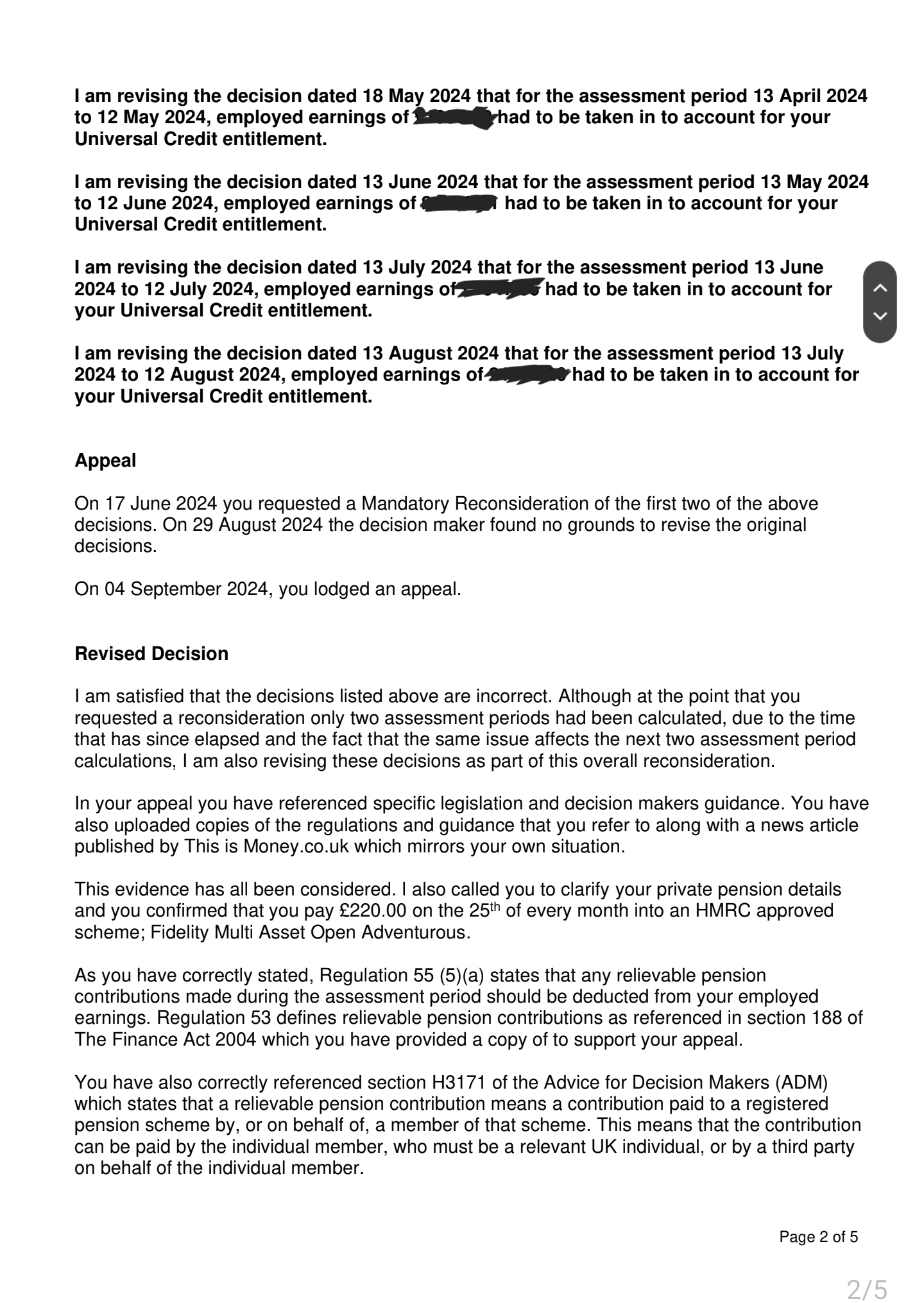

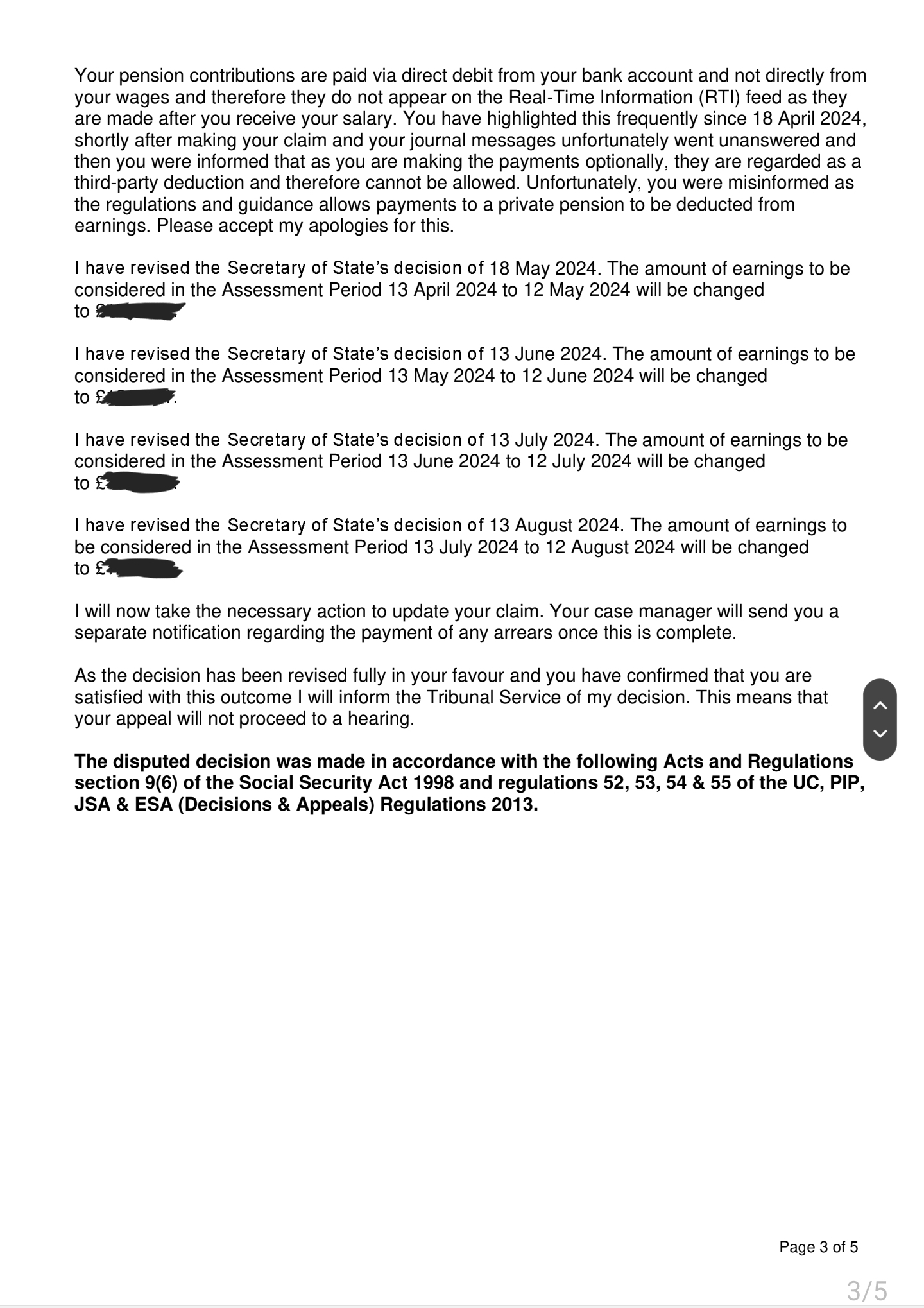

Universal credit and private pension contributions

Comments

-

P68696c said:Thank you all for your responses. That is very helpful and I will certainly be acting on (or refraining from certain actions based on) some of that advice.

The main point we are trying to answer, though, is if/how my partner's pension contributions can be taken into account.

Increasing my pension contributions would not achieve what we want because, although it may have the same net effect on the UC award received, the money would then be in my pension not may partner's.

All we want to do is have her pension contributions fairly taken into the calculation of the net household income being reported on our joint claim, in the same way it was when we were on Tax Credits.

Does anyone know if it is at all possible to do this with UC?

Thanks againOn UC, any pension contributions your partner makes can only be deducted from their earned income, not yours.If they have no earned income, because they are not working, then there is nothing to deduct from, so any pension contributions they may or may not make are completely irrelevant (to UC).If you want to reduce your earned income, then you must contribute to your own pensionUC will then look at your combined earned income when calculating your UC award.

I am a Forum Ambassador and I support the Forum Team on the Benefits & tax credits, Heat pumps and Green & Ethical MoneySaving forums. If you need any help on those boards, do let me know. Please note that Ambassadors are not moderators. Any post you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own & not the official line of Money Saving Expert.1 -

That has already been answered in this thread.P68696c said:Thank you all for your responses. That is very helpful and I will certainly be acting on (or refraining from certain actions based on) some of that advice.

The main point we are trying to answer, though, is if/how my partner's pension contributions can be taken into account.

Increasing my pension contributions would not achieve what we want because, although it may have the same net effect on the UC award received, the money would then be in my pension not may partner's.

All we want to do is have her pension contributions fairly taken into the calculation of the net household income being reported on our joint claim, in the same way it was when we were on Tax Credits.

Does anyone know if it is at all possible to do this with UC?

Thanks again1 -

You CAN'T do it , as you partner would need to have earned income. However You can still maximise UC claim by increasing your own pension contribution. Depending on you current contribution and personal circumstances.P68696c said:

All we want to do is have her pension contributions fairly taken into the calculation of the net household income being reported on our joint claim, in the same way it was when we were on Tax Credits.

Does anyone know if it is at all possible to do this with UC?

Thanks again

We put 100% of our take home pay into pension each month. So our earnings for UC calculations is 0. If we did not do this we would lose 55p in the pound from our UC claim for every £1 we don't put into our pension.

0 -

justwhat said:We put 100% of our take home pay into pension each month. So our earnings for UC calculations is 0. If we did not do this we would lose 55p in the pound from our UC claim for every £1 we don't put into our pension.

Do you get called in for work search reviews and regular messages due to doing that?

0 -

No because i i am over the hourly threshold for work search reviews.Aaron77r said:justwhat said:We put 100% of our take home pay into pension each month. So our earnings for UC calculations is 0. If we did not do this we would lose 55p in the pound from our UC claim for every £1 we don't put into our pension.

Do you get called in for work search reviews and regular messages due to doing that?1 -

justwhat said:

No because i i am over the hourly threshold for work search reviews.Aaron77r said:justwhat said:We put 100% of our take home pay into pension each month. So our earnings for UC calculations is 0. If we did not do this we would lose 55p in the pound from our UC claim for every £1 we don't put into our pension.

Do you get called in for work search reviews and regular messages due to doing that?

There's other threads about people who's NET earnings fall below the AET of £1437 being called in, so that seemed to be the measure used not hours worked, not sure even DWP broadly know what their own policies are tbh!0 -

Pretty sure the rule relates to earnings and is translated to hours using NMW (possibly it is based on x hours times NMW but then the check is on the money not the hours). Personally I find it useful as if you do earn more than NMW you can work fewer hours than the stated number which was not an option under UC and you can also then make personal pension contributions which (should eventually) get deducted from the income that is used to assess the payment level.Aaron77r said:justwhat said:

No because i i am over the hourly threshold for work search reviews.Aaron77r said:justwhat said:We put 100% of our take home pay into pension each month. So our earnings for UC calculations is 0. If we did not do this we would lose 55p in the pound from our UC claim for every £1 we don't put into our pension.

Do you get called in for work search reviews and regular messages due to doing that?

There's other threads about people who's NET earnings fall below the AET of £1437 being called in, so that seemed to be the measure used not hours worked, not sure even DWP broadly know what their own policies are tbh!

The OP should definitely try not to have to opt out of their LGPS just to keep the same level of benefits as although they get to keep their 5.45% (less tax and benefit withdrawal) they effectively lost out on about a 29% of salary employer contribution - that is a big part of total renumeration lost.I think....0 -

Hi everyone,I've been lurking here for a while, reading through all the advice on dealing with Universal Credit and pension contributions. I've been going through the same situation, but thanks to the tips and guidance I've found here, I've finally managed to get them to take my pension contributions into account!Just wanted to pop in and say a huge thank you to everyone who has shared their experiences and advice. It's been incredibly helpful, and I'm grateful for the support!

7

7 -

Great update 👍1

-

i really do not understand why we have to jump through so many hoops. Its not even consistent hoop jumping lol1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards