We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Capital Preservation ITs

capital0ne

Posts: 872 Forumite

The market will crash in the next 5 years - bonds and equities.

Which IT would preserve your wealth, mt research tells me it has to be RIT CAPITAL PARTNERS and PERSONAL ASSETS TRUST.

What other ITs are people considering to preserve your portfolio from being decimated when the crash comes? What other strategies are you considering besides the obvious cash, gold, vintage wane and automobiles and other collectibles

Which IT would preserve your wealth, mt research tells me it has to be RIT CAPITAL PARTNERS and PERSONAL ASSETS TRUST.

What other ITs are people considering to preserve your portfolio from being decimated when the crash comes? What other strategies are you considering besides the obvious cash, gold, vintage wane and automobiles and other collectibles

0

Comments

-

Continue to invest monthly and ignore all the noise?

The market will crash I agree, quite possibly within the next 5 years, maybe even twice in that time who knows?

RIT and PAT are ceratinly options, particularly if you have reached whatever your target is, or you have a looming "date" when you need to convert back to cash, and are now looking to "preserve" what you have rather than grow it.

Of your other suggestions, apart from a healthy emergency cash fund, they don't feature in my strategy at all.0 -

I hold the two you mention.

RIT is not really a "capital preservation" IT as much as, say, the Troy or Ruffer products you could have instead, though I am not using those as I already have and like Personal Assets and my portfolio doesn't have space for them all.

It has some interesting choices within its diversified holdings and though it's currently positioned more defensively than at other points in the cycle, I wouldn't call it "low risk". For me that's fine; when combined with a holding of Personal Assets you can get a reasonable "lower volatility mixed asset" allocation for your portfolio, though the equities within it aren't massively globally diversified.

Other things in the "non equity" space include things like HICL and INPP, some real estate, some absolute return etc.

Things like wine and vintage cars can be a bit of fun but are not at all defensive. When the market is frothy and people have huge stock exchange gains and investment banking bonuses, they can buy Enzos and E-Types and pay crazy money for Ch. Latour. When the markets are at a low and the fund bosses' total wealth dropped 30-50% and high paid jobs for six-figure++ salary brigade are somewhat less certain due to recession, those "alternative assets" are really just luxuries which fall out of favour.0 -

Cheers Folks, Okay, I've reached my target in my portfolio, its 60/20/20 Equities/Bonds/Property - 50/50 Global/UK and I have ample cash, along with an income after tax of £30k+. Portfolio is all reinvested automatically, house is mortgage free etc etc.

So my objective now is to preserve capital and get an annual growth of 5%+

I have a small holding in RIT so I'm thinking to increase this and also looking ahead to April when I'll be moving £40k into my ISA portfolio - my methodology is KISS!0 -

I plan on sticking to 100% equities and preserve my wealth by doubling it now so when and if it crashes I won't mind so much. Anything else seems like pointless guesswork0

-

If you know the market will crash in the next 5 years best buy lots of gold.0

-

capital0ne wrote: »What other ITs are people considering to preserve your portfolio from being decimated when the crash comes?

Your use of the word 'decimated' would historically have meant '1 in 10' but I think you mean much more than that, so how big a percentage do you think the markets will crash and how long will they remain down?

I think (but cannot guarantee) that even if the markets do fall then they'll get back most of those losses within a few years, so I'm staying fully invested given that only hindsight gives you the best time to buy and sell.0 -

I plan on sticking to 100% equities and preserve my wealth by doubling it now so when and if it crashes I won't mind so much. Anything else seems like pointless guesswork

I'm guessing you see it something like the link below..

https://img.iex.nl/profs/12siegel2108.jpg

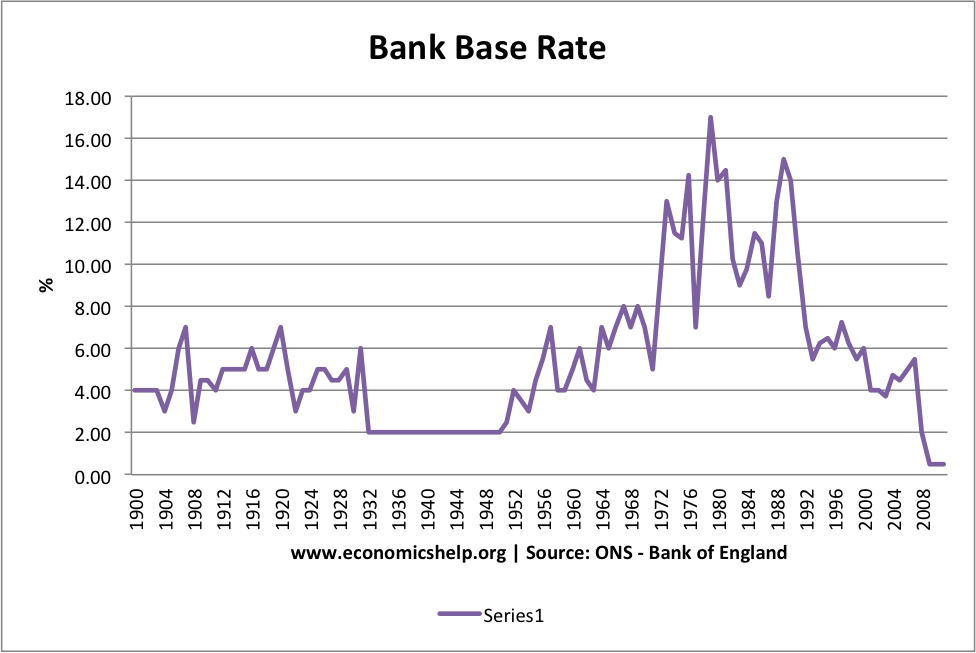

In that link 1994 isn't even the peak of base rates but they are certainly near a low now..

https://www.economicshelp.org/wp-content/uploads/2009/04/historical-interest-rate-1900-2011.png

http://www.marketoracle.co.uk/images/2010/Jan/libor-spread-dec09.gif0 -

It seems strange to see someone using ITs when it comes to talking about capital preservation and showing fear of a regular negative occurance.The market will crash in the next 5 years - bonds and equities.

Whilst you never know when it will happen, its not much of a stretch to suggest a crash in the next 5 years as crashes tend to occur within every 5 years. The last one was 2 years ago.

What did you do in preparation for the last crash 2 years ago?

Why are you using more advanced investment options if you are concerned about crashes "decimating" your value?

What do you mean be decimating? It means 10% if you follow it's true meaning but others use that phrase when they mean the majority of it lost.

Some of those are not obvious.What other strategies are you considering besides the obvious cash, gold, vintage wane and automobiles and other collectiblesI am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.0 -

I am in the position/age where any excess growth beyond inflation is likely to be wasted. So currently about 25-30% of my investment portfolio is split fairly evenly between RCP (RIT), RICA(Ruffer), Trojan 'O' and Jupiter Strategic Bond. See Linton WP on the GB - Invest-off thread.

Another 25-30% is invested as in an Income portfolio. The remaining 40% is aimed at well diversified high growth (See Linton Growth).

The strategy is to reduce Growth to 33% investing more in the Income portfolio. From then on annual rebalancing should look after most eventualities.0 -

I am in the position/age where any excess growth beyond inflation is likely to be wasted. So currently about 25-30% of my investment portfolio is split fairly evenly between RCP (RIT), RICA(Ruffer), Trojan 'O' and Jupiter Strategic Bond. See Linton WP on the GB - Invest-off thread.

Another 25-30% is invested as in an Income portfolio. The remaining 40% is aimed at well diversified high growth (See Linton Growth).

The strategy is to reduce Growth to 33% investing more in the Income portfolio. From then on annual rebalancing should look after most eventualities.

IMO your WP and Growth portfolio's are really good, would you mind me asking what you hold in your income portfolio?0

{kind=link}

{kind=link}

{kind=link}

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.5K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.6K Work, Benefits & Business

- 603K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards