We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Am I making a mistake by delaying investing?

Comments

-

AddictedSaver wrote: »I don't know that it's at it's peak but the last two times it was this high is came crumbling down, first the dot com bubble and then the 2008 crash. Now I've got it sown into my mind that brexit will be the next one.

The US is sky high at the moment too

Now I know it will go up more in the future, the world just doesn't lose money over the long term, economic growth will always be more, unless there is a world war or something. Interest rates are super low at the moment too which is causes more people to buy into the markets, once the economy becomes a bit more stable, interests rates will go back up which will cause the markets to go down.

Perhaps I'm just letting my inexperience get the better of me. I'll hunt around for a well diverse global fund, a fund of funds preferably... I really like the Vanguard LS funds but what are some similar funds but that are not exclusive to the UK?

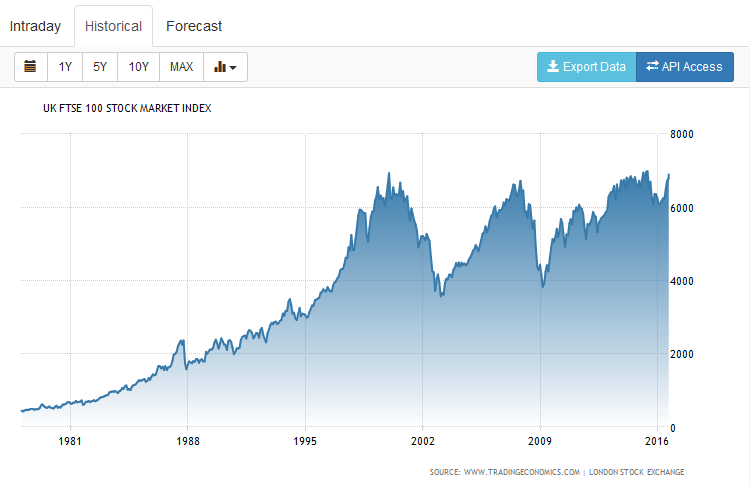

You are making a huge mistake by looking at a graph with a linear y axis. That makes it look like recent times are extraordinary with huge peaks compared to the past. You need to look at a logarithmic plot, and when you do so, you'll see that actually peaks are a universal feature of markets, and recent ones are not unusual. You could also use the linear plot but look at several with end dates of 2000, 1990, 1980 etc. The recent for this is that growth is compound, and hence exponential.

Like many here, I've lived through many a market crash, and firstly they offer buying opportunities, and secondly the markets always recover after a few years. Generally a crash is good news, unless you need to take money out e.g. during retirement. Then I guess you need to adopt some more clever strategies, or simply take out a bit more money while the going is good and forego some potential gains.

Oh, and the graphs only tell part of the story as they ignore dividends. So for us what really matters is the total growth of a sector including reinvested dividends.0 -

Forgot to mention that deriving an extra ordinary profit from timing the market is not dependent on calling the extreme top or bottom of the market. And neither does it involve disposing of all one’s holdings. All you need to do is trade the volatility inherent in some of the more popular shares/trusts etc with some of your capital.

Aha, so it's dead easy then. Sorted.

The trouble is with that little phrase you used, "All you need to do ". Reality is a wee bit more complex.I’m sure Woodford/Slater and other Alpha managers prefer buying low and selling higher rather than climbing in to any old share at month end regardless of its valuation.

There are a couple of points there. Firstly they will move into and out of asset classes and sectors according to how they perceive the valuation and outlook. Thus a sector might be popular, but they judge that it has run out of steam. Secondly they will buy into companies they consider undervalued, or which have a bright future. Both strategies require huge amounts of research and knowledge, something that someone like the typical poster here, including muggins and probably you too, does not have.If a trade goes against you, and it can in the short term, it’s just a matter of sitting on it until the outlook and valuation for that particular investment improves, just as the average amateur long only investor, such as yourself, does.

Again you use a little phrase "it’s just a matter of sitting on it". No, it is a case of being able to correctly make a judgement, something few of us can do.0 -

Invest now or time the market?

Personally, I do both.

Set up a regular monthly investment for lifetime investments that you will only call on when you are retired... then look occasionally at a bit of market timing for short term profit taking if you see an opportunity.

If there are no market timing opportunities then for me the left over goes into topping up my p2p or cash.

About 6 months ago CAPE showed Russia as a good punt. I made 30% and now have pulled out the profit.

If the timing didn't work as planned, happy to hold until it came good.

I also have some fundsmith. It looks high now, but then it's made profit year on year recently, so who's to say it will ever significantly fall to a degree that cancels out its good returns?

To the opening post, if you have a lump sum, I wouldn't go all in. I would drip feed into a balanced approach and then if the markers do drop (as you predict) you could then start adding your stash at a quicker rate to take advantage.0 -

The complexity involved in timing the market is in the hands of the user.

My method is basic thus very simple. The biggest hurdle to overcome, for a novice, is the courage to take the plunge.

Money is only lost by buying high and selling lower. All other advice, if wrong, only results in an investor losing out on a bit of growth or dividend income, not losing money. Which is why i offered the advice i did on the day i did – to rather delay taking the plunge – if wrong they lose out a bit, but being right enables an investor to buy in at a lower price on a future date – probably sometime between end of September 2016 and Feb 2017. Or maybe even sooner.

If you cannot make a judgement then don't follow advice/info, rather consult and pay an IFA.

Otherwise DYOR0 -

The PE10 is a poor predictor for short-term market timing, markets can stay overvalued (in terms of CAPE PE10) and make gains for years before they eventually correct.

What the PE10 is good at is predicting longer-term returns. For example the PE10 has a strong inverse relationship (high PE10 equals low returns, correlation -0.65) over the following 15 years.

If you do want to hedge against a correction in a high PE10 market, one option is dynamic asset allocation. In short that means adjusting the proportion of equities you hold according to the PE10. But with the long-term horizon which I understand you have, I’m not sure I would bother with PE10.

But what ever approach you do decide on make sure you understand what you are doing and why you are doing it. Chopping and changing strategies and panicking at every market correction is the easiest way to lose money - far more damaging than entering the market just before a correction but holding your nerve to ride it out and continuing to invest regularly throughout.This is a system account and does not represent a real person. To contact the Forum Team email forumteam@moneysavingexpert.com0 -

Can you spot the buy sell opportunities in this graph of a popular share? Some of us did and made a profit more than once0

-

Money is only lost by buying high and selling lower.

That's not strictly true. What about holders of shares that became worthless? Holding on so they didn't sell at a loss wouldn't have helped them.

There is a very big difference in risk and process for buying individual shares compared to buying into the market as a whole via a fund whether managed or tracker and many new investors suggested by this post should probably not be buying individual shares.Remember the saying: if it looks too good to be true it almost certainly is.0 -

-

Of course, a lot of people also spotted these buying opportunities before you;

They're not doing so well (yet).

On the contrary, the greatest volatility and thus opportunity for making profit is in a bear market. the yahoo finance web has several free tools that have helped me make many an informed buy/sell (profitable) decision in just such a situation you present here and regardless of the overall trend. You have identified some but not the best buy positions, but no sell positions, why? The tools would have provided the info.

DYOR, use the tools, its not difficult.0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.5K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards