We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

I don't understand why people can't be bothered!

Comments

-

Very true.

Plus society in general is now so very consumerist.

As others pointed out recently, even this very forum and website are very focussed on consumption and how to do it for less, rather than how to reduce it, and on how to make your money go further rather than how to make it work and grow.I am one of the Dogs of the Index.0 -

I guess it's the same mentality that means so many do the lottery every week. The hope of that big win that will make an immediate millionaire overnight, rather than patiently saving and achieving it yourself by investing and compounding over many years. One takes effort, the other no thought at all. Yet many would do better to invest that lottery money and after a few years would have a pot accumulated with no lifestyle changes.Thrugelmir wrote: »Jam today mentality. Lost are the old virtues such as take care of the pennies and the pounds look after themselves. Leveraging with debt ( aka BTL) is perceived to be a far quicker route to riches.

You do get the occasional article about someone who dies a millionaire and has invested over many years and has no outward trappings of wealth. Yet the lottery winners get far more publicity.Remember the saying: if it looks too good to be true it almost certainly is.0 -

From my own personal experience, I am 24 years old and a lot of my friends don't dabble in investments but instead choose safe cash ISAs/bank accounts.. For a number of reasons;

- Some think that investing is only for the rich/wealthy, so they don't even bother looking into it

- Little or no understanding of the concept of risk and return, and just choose the easy/simple option (bank accounts, cash ISAs etc). with little, to no risk and little return.

- Simply do not understand how investments and investment portfolios work. And little to no understanding of different risks other than capital risks (inflation risk, shortfall risk etc).

I guess I am fortunate because I work in financial services, in particular corporate pension schemes and I have worked at a big stockbroker before. I know a lot about them, both from my work and my own personal research/monitoring. I'm always happy to talk about investments with my friends, encourage them to take a look at them but often they just shy away or say they can't afford it (I think this is mainly down to attitude to saving/investing seeing it as super risky/for the rich rather than genuinely having no spare money after expenses etc)."If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes” Warren Buffett

Save £12k in 2025 - #024 £1,450 / £15,000 (9%)0 -

Perhaps the answer to the original question could be "The state will provide"

Consider person A. Always spends all their earnings cars,holidays, latest high tech, never worries about share prices. Retires on minimum state pension which will be topped up by Pension Credit, housing benefit, help with winter fuel costs , et all.

Fast forward they require residential care, no capital all paid by the state.

Person B steady saver, investor, worries about poor interest rates, share prices etc.

On retirement no additional state benefits paid. Again fast forward they require residential care, savings and capital needs to be used.

Yes I appreciate B will perhaps have availability to chose where they live and which residential home they go to, but is it worth all the effort.

Just my thoughts.

I dont believe that is the reason.

In my view the real factor is learned behaviour passing from parents to children. Certainly until the 2nd world war and perhaps 10 years after that significant numbers of people were living in abject poverty and many more living hand to mouth for the real physical basics. There was no culture of building serious capital because it wasnt possible, beyond a small weekly subscription for the Christmas Club.

The children and grandchildren absorbed the same attitudes which became increasingly inapproriate as general wealth increased. The "basics" simply got broader, rather than being constrained by a requirement that their satisfaction be sustainable.

Another factor, again passing from generation to generation, is that there was no expectation of living to a real old age. Pensions in general werent a serious issue until say the 1960s as people didnt usually live long enough to enjoy them for many years beyond retirement, and if they did their children would support them. Society driven by economics and technology has changed quickly, it takes generations for entrenched attitudes to change.0 -

Half the population have very little in savings according to recent research...most less than £5,000.

Maybe people with spare cash tend to see property or improving their home as a safer bet.

If you have limited savings theres nothing wrong with £50 a month in a cash ISA or even a fund.

Years ago people had a nice little £5 a month in a 10 year endowment policy and a nice little pick up at the end.

I've just had a look around various websites to compare cash and fund savings since the year 2000 as its been highlighted in previous posts..

The links below show the FTSE 100 and the FTSE All share together with MSCI World and FTSE World.

http://www.trustnet.com/Tools/Charting.aspx?typeCode=NM990100,NWORLDS

http://www.trustnet.com/Tools/Charting.aspx?typeCode=NWORLDS,NUKX,NASX

In 15 years the World Index is showing a touch above 80% and the FTSE 100 around 60% or more.

As I understand it this includes the dividends but not the management charges which could be 15% or more in the 15 year period.

Years ago investors paid an initial charge of 5-7% on fund purchase and around 1.5% annual charge.

Today with tracker funds you can reduce your charges to less than 0.5% annually so going forward you should have much better results.

Moving on to cash savers I've used the following link...

http://www.swanlowpark.co.uk/savingsinterestannual.jsp

From the year 2000 a cash lump sum would be around 88% higher in a cash ISA by 2014.

A bit of a surprise with the very low rates on offer recently and the figures used are the average rates.

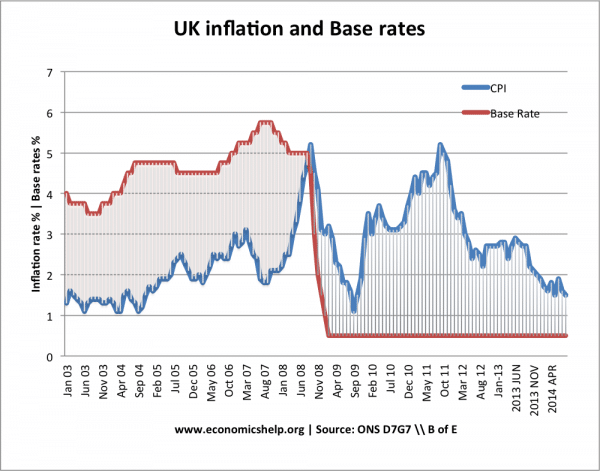

Another thing to consider is the link which has been broken between base rates and inflation..

http://www.economicshelp.org/wp-content/uploads/blog-uploads/2011/12/uk-base-rates-inflation-89-11.png

http://www.economicshelp.org/wp-content/uploads/2014/04/inflation-base-rates-since-03-600x471.png

All good stuff...maybe you need to be the markets 20 plus years to give yourself a chance...it aint easy.0 -

george4064 wrote: »- Some think that investing is only for the rich/wealthy, so they don't even bother looking into it

Good post! I think the part I quoted above is certainly true. I used to think that investing was for "other people", particularly Telegraph reading cigar smokers. The only reason I really changed my mind was because I got !!!!ed off at my bank for cutting my savings account to an absurd 0.1% return and I started looking around. I got caught up in finding the best possible interest bearing accounts, and started getting exposed to people advising me invest in stock markets. I learnt that in the long term there is virtually no risk at all if you do things sensibly. Which relates to the other point you made about education.0 -

Moving on to cash savers I've used the following link...

http://www.swanlowpark.co.uk/savingsinterestannual.jsp

From the year 2000 a cash lump sum would be around 88% higher in a cash ISA by 2014.

A bit of a surprise with the very low rates on offer recently and the figures used are the average rates.

Bear in mind those are gross interest rates and basic rate income tax is relatively low now by historic standards.'We don't need to be smarter than the rest; we need to be more disciplined than the rest.' - WB0 -

-

Look around you. How many newish cars do you see? How many people choose to live in houses bigger than the minimum they need and deliberately avoid areas where houses are cheap. People take more expensive holidays than they "need", assuming they need any. Not everyone buys their clothes in charity shops. All of these are choices.

Those people who dont have these choices clearly cant invest but simple observation shows that a large majority of people arent on the breadline.

Given the large number of people whose income is so low as to make them eligible for state top ups (over 3 million at the last count) I really wouldn't be so confident about using words like "large majority" in this context. Also, you don't allow for the number of people living a comfortable lifestyle but based on credit, where spare money should be geared to paying it off rather than investing money they don't actually have.

I too live in a pleasant, comfortable area but it doesn't blind me to the numbers of people who aren't so fortunate, neither does it make me believe that they don't invest simply because they "can't be bothered".0 -

Plus 2000 has been chosen because it shows the worst possible returns for the FTSE. Starting from 1997 or 2003 gives a very different picture.

Also unusual that someone would pay a lump sum in 2000 and do nothing else for 15 years. If someone drip fed the investment for 15 years the returns would have been much better, and much more consistent.0

{kind=link}

{kind=link}

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards