We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

PLEASE READ BEFORE POSTING: Hello Forumites! In order to help keep the Forum a useful, safe and friendly place for our users, discussions around non-MoneySaving matters are not permitted per the Forum rules. While we understand that mentioning house prices may sometimes be relevant to a user's specific MoneySaving situation, we ask that you please avoid veering into broad, general debates about the market, the economy and politics, as these can unfortunately lead to abusive or hateful behaviour. Threads that are found to have derailed into wider discussions may be removed. Users who repeatedly disregard this may have their Forum account banned. Please also avoid posting personally identifiable information, including links to your own online property listing which may reveal your address. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Buy to Lets - Yields

McThingy

Posts: 2 Newbie

What is considered a good yield on a buy to let investment please? I can't seem to find any benchmarks so wondered in the current economic climate what would be considered as a good yield. Thanks.

0

Comments

-

6% or above is considered decent0

-

Is the 6% yield figure gross or net (before or after tax and other expenses)? Is there a formula for calculating yield?0

-

Depends...some people look for a potential for capital growth and so will take a lower yield.I'm a Forum Ambassador on the housing, mortgages & student money saving boards. I volunteer to help get your forum questions answered and keep the forum running smoothly. Forum Ambassadors are not moderators and don't read every post. If you spot an illegal or inappropriate post then please report it to forumteam@moneysavingexpert.com (it's not part of my role to deal with this). Any views are mine and not the official line of MoneySavingExpert.com.0

-

calcualating the yield and getting the rent off the tenant are 2 different things lol

watched an episode of tenants on benefits last night and someone bought a house that was a 12% yield on paper, turns out 8 months or so down the line he hasnt received a penny in rent - yield not so much 12% anymore 0

0 -

It use to be 10% or over, I guess buy to let is becoming more uneconomic over time as they over pay for the housing.

At 6% it makes void periods more dangerous as well as urgent maintenance.:exclamatiScams - Shared Equity, Shared Ownership, Newbuy, Firstbuy and Help to Buy.

Save our Savers

0 -

I wouldn't just look at what is considered a good rental yield. As a general rule of thumb, the higher the yield the higher the risk like in the example given by Argghhh. The higher yields tend to be at the lower end of the rental market where tenants are more likely to be in receipt of benefits and then your business becomes very dependent on the whims of the government.

HMO properties give higher yields as well but they require more managing so therefore more of your time or higher agent fees if you choose to use one. HMO also tend to have a higher churn of tenants.

Have you looked at any other less hassle investments as well as BTL?0 -

Totally depends on the area and type of housing, and the interest rate environment.

A BTL at 6% looks great at 1.5% mortgage/savings rates. It looks awful at 4% rates that existed only a few years back.

If you are earning it on a million-pound London house it will nicely cover your overheads. If you are earning it on a bedsit in Sunderland it barely pays you to spend the time organising it.

etc.0 -

princeofpounds wrote: »Totally depends on the area and type of housing, and the interest rate environment.

A BTL at 6% looks great at 1.5% mortgage/savings rates. It looks awful at 4% rates that existed only a few years back.

If you are earning it on a million-pound London house it will nicely cover your overheads. If you are earning it on a bedsit in Sunderland it barely pays you to spend the time organising it.

etc.

When considering yield it is also interesting to consider capital growth, while you can maybe get 12% in some places if you can get 5% with a good capital growth.0 -

I'd say upwards of 5% gross (i.e. before expanses and tax) is OK, espcially in areas of reasonable prospect of capital growth; which isn't guaranteed in every region of the UK; to take our experience as an almost 'accidental landlord' as an example;

My first purchase; a 2-bedroom ex-council flat has increased in value and is arguably worth £175k-£200k and now enjoys a rent of £10k pa; a return of around 5-6% on current value; so no great shakes. But as we bought it over 16 years ago for £34k (not really as an investment or to become a LL but because my GF's daughter and grandchild was in a damp rental and needed a decent home for a couple of years) the capital appreciation has been immense; in effect, as much as the total rent over the years. Similarly, a BTL wreck I bought at auction for £67k and had to spend £25k+ rebuilding in 1997, went for £180k three years later; so the gain was more than I earned in wages in those 3 years, although the rental return wasn't bad after 6 months initial work.

However, having bought a 3-bed seaside flat - another wreck -for £155k at the height of the market in 2007, and spent £20k doing it up, we decided to rent it out and only got 4% return due to a poorer market in that eastern coastal region, then in effect lost a couple of thou' when we decided to sell in 2010 and got £173k (albeit off-set by 18 months' rent; around £12k gross). But we took that cash, bought a suburban London flat for £152k in an area of higher rental return and got 7% gross. Plus reasonable prospects of capital growth as be bought at the bottom of the market.

So back to your Q; 4%?, 5%?, 7%?... take your pick! Capital growth or capital loss? Just hope you get lucky with timing and location! Best wishes0 -

Whilst you are right, I think the understanding of capital growth in the BTL community is often very poor.When considering yield it is also interesting to consider capital growth, while you can maybe get 12% in some places if you can get 5% with a good capital growth.

There is often an assumption that buying a low yield property (say 3%) in a hot area (e.g. London or nice SE town) will lead to perpetually higher capital growth than somewhere less popular (say Sunderland 7%), and the run of London property in the bull market of the last 20 years is cited as evidence for this.

If we assume that London house prices grow 4% faster than Sunderland every year to 'compensate' for the lower yield, then you quite quickly run into ridiculous results:

In 5 years the London house price is now relatively 22% more expensive than the Sunderland house price, compared to the original prices.

But in 50 years (an investing lifetime) the London house price should grow 71x that of the Sunderland! Clearly that doesn't happen.

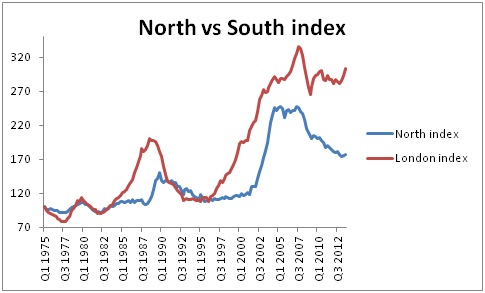

You can see from the chart below that what actually tends to happen is that London house prices do rise faster than the regions in a boom, but they also shrink faster during a slump (the most recent cycle is something of an anomaly compared to the last three, which are just as significant even if they appear smaller on the scale - remember this is not inflation adjusted).

[IMG]https://encrypted-tbn3.gstatic.com/images?q=tbn<img src=http://static.moneysavingexpert.com/images/forum_smilies/angel-smiley-002.gif border=0 alt= title=You are wonderful smilieid=16 class=inlineimg>Nd9GcSvntC3R7AbgEI75BgT1Dq5IXlI6LDvfRSFUN_mGqMR4V8HZCsM[/IMG]

(Edit: Chart didn't appear for some reason, trying to find a link again... ok try this, not the original but give you the idea)

http://moneystepper.com/wp-content/uploads/2013/11/North-vs-London-index.jpg

Now, that's not to say that London house prices can't grow faster for quite an extended period of time, decades or centuries even. But long-term that rise is capped by the productivity growth (~economic growth) of the land the property sits upon. And the negative cyclicality of prices can be much stronger in London than elsewhere despite the long-term outperformance.

London cannot grow faster than the rest of the UK forever, because if it did it would become 99.99% of the UK economy within a relatively short space of time, historically speaking.0

{kind=link}

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.1K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards