We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Stocks & Shares ISAs

Comments

-

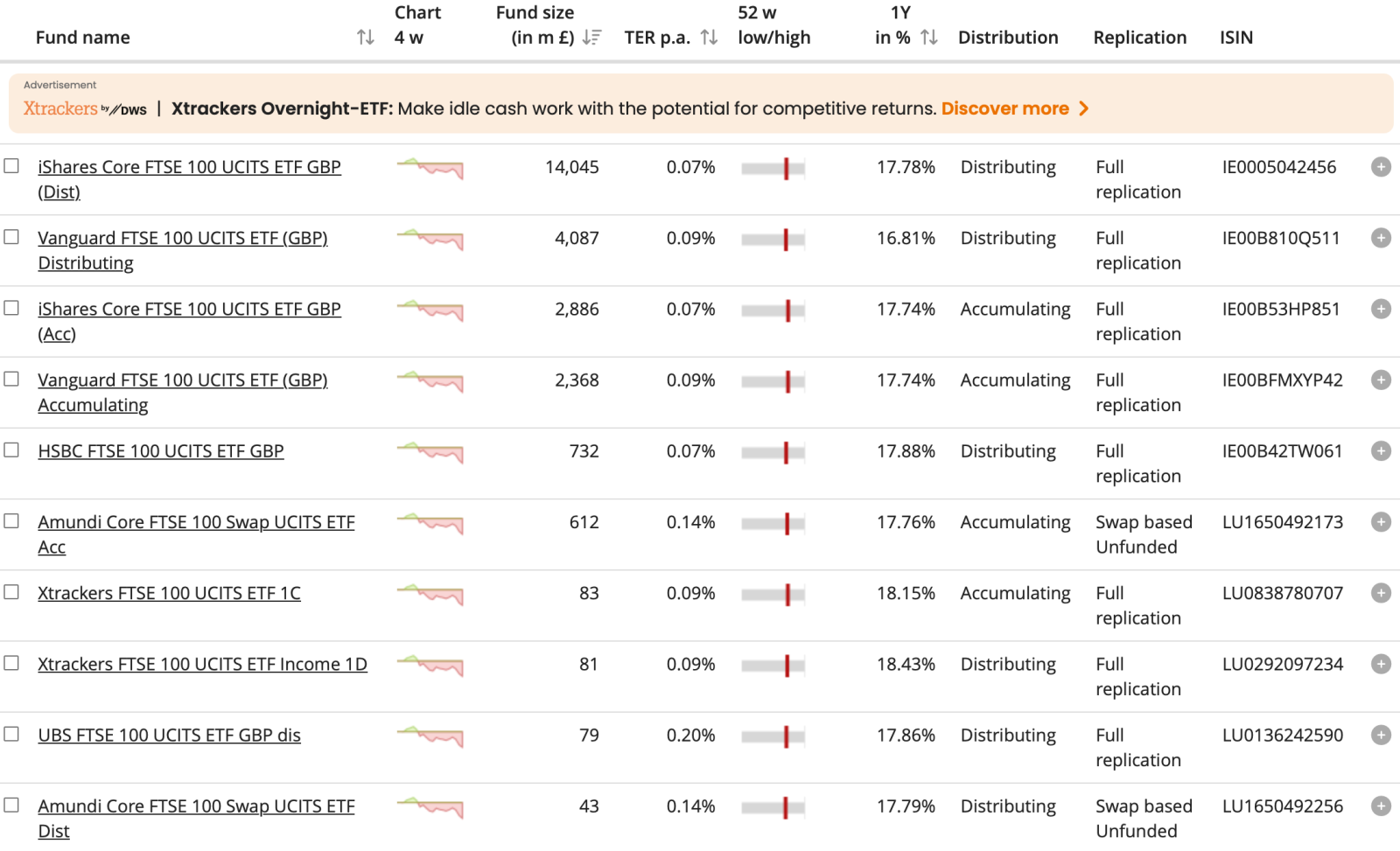

There are a few ETFs. iShares (LSE:ISF), Vanguard (LSE:VUKE) and HSBC's (LSE:HUKX) are probably the main ones.

https://www.hl.co.uk/shares/shares-search-results/i/ishares-plc-core-ftse-100-ucits-etf-dist

https://www.justetf.com/uk/search.html?search=ETFS&assetClass=class-equity&country=GB&index=FTSE%2B100

0 -

I'm currently getting my head round the new rules for ISA subscriptions as of next April - i.e. £12K limit for Cash ISAs, and the remaining £8K only available for Stocks & Shares / Innovative Finance ISAs.

I'm finding the proposed transfer restrictions (ending transfers from S&S ISAs to Cash ISAs) a bit offputting. Same goes for the proposed taxation of uninvested funds and "cash-like investments" (e.g. money market funds). Seems to me like these changes would actively discourage current Cash ISA folk from dipping the toe into finance ISAs…

But anyhow, what I specifically wanted to ask about - I've been planning to take a holding in gold, probably in the form of an ETC.

My question is this - would (Gold) ETCs be in danger of being classified as "cash-like", and therefore taxed (despite being in an ISA wrapper) ?

In particular, what if the ETC is hedged against currency?

0 -

Personally I'd have thought that the volatility of something like that would rule it out of the mooted restrictions on cash-like investments, but the key point is that nobody knows yet, as the rules are still being designed, so at this stage it's all just speculation…

1 -

Unlikely. The previous test was investments capable of losing money over 5 years were ISA eligible. Gold ETCs are well beyond that line.

2 -

Yeah, that was my impression. I just hope that once the rules are set out, they don't start changing them on the hoof when the new dispensation is in place and they see what people are actually doing.

As it stands, I could imagine a number of folk transferring funds out of S&S ISAs into Cash ISAs before next April - just to leave their options open until such time as the new system is bedded in...

0 -

It obviously makes sense for people to read the rules once they're published, and decide what to do thereafter, and it's not unreasonable to expect significant transfer activity at the end of the 2026/27 tax year, but choosing to liquidate S&S ISA holdings without having a clear and valid reason to disinvest is likely to be counterproductive.

0 -

We can be sure people are subscribing to cash ISAs who didn't normally do so ahead of the announcement to get ahead of the issue, and I'm sure you're correct that people will also transfer from S&S to cash ahead of the end of this tax year. But existing S&S ISA investors are likely to know being 100% cash over the long term is unwise, and so I'd be surprised if it was taken to an extreme. Whereas nobody who has never invested will invest less as a result of this change and some may opt to use the remaining part of their annual ISA allowance. So it will be interesting to see the overall statistics over the coming years.

0 -

My own feeling about the £12K / £8K limit is it was basically a good idea, in terms of the stated objective - cos I guess I'm a member of the target market they were looking to get interested in UK investments.

But it feels like the various restrictions to prevent folk circumventing the new limit are counterproductive.

I mean I fully admit my reaction to the initial news was to Google how soon you could transfer from a S&S ISA back to a cash ISA - and then research things like interest rates on uninvested balances, money market funds etc. Yep, circumvention was my kneejerk response. 😉

But it would have got me over the crucial inertia barrier, and I would have had an investments ISA. So after my initial low-risk approach I would likely have started to branch out and experiment. In my case, Martin L was right - the carrot would have been more effective without the stick…

As it stands, the main factor in me getting an investment account will probably be not-the-chancellor, but Donald Trump and his bad crazy in the Middle East (and not wanting to have to bury gold sovereigns in the garden). 😅

0 -

I’m just trying to check how the main deposit promo works on IG. Can I put 10,000 into a general account, transfer 1000 into a stocks and shares ISA, then take out the 9000 again without having invested it and just leave the 1000 there until September to claim the full 200 quid bonus? Thanks in advance.

0 -

whoops that should have said MAYDEPOSIT

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards