We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Credit Rating Problems

andyg55

Posts: 16 Forumite

in Credit cards

Hello everyone

First time poster here. If this is in the wrong place, please let me know (I couldn't figure out the best forum to post in).

I am 26 and have really poor credit. This is because I have just finished my PhD and did the last year unpaid. To attempt to find money, I originally tried all the obvious things (asking for an extension to my student overdraft, applying for a personal development loan etc.), but I was always rejected. As such, my biggest mistake (but only option at the time) was to get credit cards.

I currently have:

- Barclays current account (£3000 overdraft)

- Natwest current account (£1800 overdraft)

- Natwest credit card (£3100 limit)

- Barclaycard (£2400 limit)

- Egg card, which turned into a Barclaycard (£500 limit)

All of the above got maxed out when I was a student. I REPEATEDLY missed credit card payments, as I had no money to actually keep up my minimum payments.

Now I have graduated and have a good job, I have started to pay my debts off. I have now halved my debt, approximately. But all accounts are still open.

The problem is, no matter what I apply for now (any new account, credit card, finance for a product e.g. laptop), I constantly get REJECTED.

MY QUESTION - What is the best way for me to start regaining my credit 'score'? I do not miss credit card minimum payments anymore, but I missed so many during the last couple of years I'm worried this will scar me for life.

Are there any tricks? I do not use my credit cards AT ALL anymore. Should I? Once I've paid them off, should I cancel them, or keep them open?

IF you have any advice whatsoever here, I would be very glad to hear it. I understand I've been a bit of a fool, but despite repeated cries for help when I was in need, no banks/credit card agencies would help.

Thanks!

First time poster here. If this is in the wrong place, please let me know (I couldn't figure out the best forum to post in).

I am 26 and have really poor credit. This is because I have just finished my PhD and did the last year unpaid. To attempt to find money, I originally tried all the obvious things (asking for an extension to my student overdraft, applying for a personal development loan etc.), but I was always rejected. As such, my biggest mistake (but only option at the time) was to get credit cards.

I currently have:

- Barclays current account (£3000 overdraft)

- Natwest current account (£1800 overdraft)

- Natwest credit card (£3100 limit)

- Barclaycard (£2400 limit)

- Egg card, which turned into a Barclaycard (£500 limit)

All of the above got maxed out when I was a student. I REPEATEDLY missed credit card payments, as I had no money to actually keep up my minimum payments.

Now I have graduated and have a good job, I have started to pay my debts off. I have now halved my debt, approximately. But all accounts are still open.

The problem is, no matter what I apply for now (any new account, credit card, finance for a product e.g. laptop), I constantly get REJECTED.

MY QUESTION - What is the best way for me to start regaining my credit 'score'? I do not miss credit card minimum payments anymore, but I missed so many during the last couple of years I'm worried this will scar me for life.

Are there any tricks? I do not use my credit cards AT ALL anymore. Should I? Once I've paid them off, should I cancel them, or keep them open?

IF you have any advice whatsoever here, I would be very glad to hear it. I understand I've been a bit of a fool, but despite repeated cries for help when I was in need, no banks/credit card agencies would help.

Thanks!

0

Comments

-

Stop applying for credit will help. Use a snowball calculator to pay off debt starting with highest rates, clear one card and put spending through this, paying in full monthly to avoid interest and start one thing looking good.

Your credit record will improve over time, and remember to pay one pound over minimum payment to stop that marker.

Good luck.0 -

Don't apply for anything that requires a credit check. Get a free credit check with the free trials. experian do one. MAKE SURE YOU CANCEL THIS. as it'll take money out if you don't. Just go on get the info you need then call immediately to cancel.

You will learn exactly how many negatives are against you. save all this information.

draw up a budget, use the budget calculator from this website. EVERYTHING that you can spare (minus say £100 for luxuries every month depending on your income for luxuries) divide it appropriately between your debts. If you have some debts which are small and relatively (several months) quickly paid off, get rid of them.

Draw up a plan based around this checklist.

One your debts are paid off, close the accounts. Having lots of accounts open does work against you.

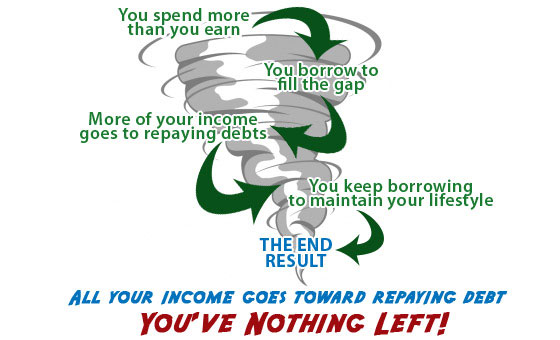

if you are rejected for anything, this shows up to anyone else who does a search to. Just calm it down, wait until you don't have any debt before you aquire more. see: debt spiral for more info.

You'll have other negatives than the amount of searches/rejections and debt working against you too. Read entirely through this section of the website, and any other sub categories that apply to you, in fact just read through everything.Debt Starting: £1995 | Current Debt: £1105

Rainy Day ISA £0 - had to emergancy empty

Say no to TV Licencing0 -

You're in a bit of a pickle but now that you're earning and making inroads into the debt then there's hope. Missed payments and defaults won't scar you for life, they will remain on your credit file for six years and then drop off. That's the good news. The bad news is that you're unlikely to be approved for any new credit for at least the next 12-24 months. To be honest, I would't even apply if I were you as each search will be recorded and if you have too many it will looks as though you're desperate and can't cope financially.

So, what you need to do is put all of your available income into reducing your current card debt. Pay just over the minimum for all of your cards each month and on time - try to avoid paying the absolute min payment as this is sometimes also recorded and can have a (slightly) negative effect. A pound or two extra is enough to avoid the minimum payment marker on your file. once you've made all of your minimum-ish payments each month, use all of your remaining free cash to pay off as much as possible on the account that charges the highest interest (whether that be your overdrafts or a credit card). Do this each month until you've paid this card off completely and then move on to the card with the next highest rate of interest and so on....

This is the most efficient way to pay off your debt without causing further damage to your credit file and it will help to repair some of the damage but it isn't necessarily going to improve your file a great deal on it's own. To do this you need to show that you can use credit responsibly as well as pay off what you owe. So, what I'd do is once you've cleared your first card, don't close it immediately. Set up a direct debit to pay in full each month and just use it for your normal spend instead of your debit card (just don't withdraw cash with it!). In fact, try to avoid using cash for anything if you can - cash has no influence on your credit whatsoever. Try to put all of your spending on your credit card, always ensuring that you have the money to cover it, and pay it off in full each month.

Once you've paid off another card then you can think about closing accounts as you go along. I'd probably decide which current account you see keeping long term and keep that credit card as the extra history with the bank may assist you if you decide to apply for anything else down the line.

Someone else may be more in the know than I am - but I believe that being in your overdraft is likely to be worse than having debt on a credit card (O/D are supposed to be for short term borrowing) so I'd probably try to clear those first. Then again if you're earning a decent amount and you O/D are still interest free from uni then you might be better off trying to smash down the CC debt as quickly as possible.

I have been in exactly the same position as you when I left uni. Luckily I managed to land a job paying a decent amount almost straight away and was able to clear about £10k in a year (student loan company is still hitting me every month but at least that isn't viewed negatively by lenders). If I were you I would (and did) implement self-imposed austerity measures. Seriously, I lived like a pauper for about six months and put virtually all my disposable income on repaying my debts. I also sold a load of stuff I didn't need on eBay and used things like cash-back websites to raise extra money to put towards my CCs. It sucked balls at the time but at the end of it I have the room to breathe financially to start actually enjoying myself.

Anyway, that might all be wrong but thats what I'd do!0 -

Haha! I took so long writing that that most of my points have already been covered (far more succinctly)! I'd avoid the experian free trial though. It's too easy to forget to cancel. Just sign up to noodle and you can see your file (updated once a month) for free forever.0

-

Your history drops off after 6 years - so pay on time and don't go over limit.

Don't take out cash on credit cards.

Dont apply for more than 2 lines of credit per year if pos.

Don't go too close to your limits. Lenders look at your credit based on percentage of your overall AVAILABLE credit - so keeping accounts open for now will be an advantage.0 -

Well first of all, thanks everyone for your response. You're very helpful! It's also good to know that other people have been in this situation and got out of it

")

I really like the idea of paying the credit card off with highest interest first, then using it to make my everyday purchases, then paying it off in full at the end of every month. I will be doing that ASAP.

I have a few more questions if you can help further?

1. I signed up to Noddle. It's great! So much easier than Experian, plus you can see everything there and then instead of having to send off and pay for a pass code. But my question - it gives me a credit score of 1/5. Everything on my file on Noddle is in order (I'm on the electoral role, I have no bankruptcies/insolvencies/judgements on my file, no financial connections). Where can you see the BAD stuff? I want to see what it is exactly that is making my score 1/5. Can you view this using Noddle? What are the main BAD points I should be taking notes from off Noddle?

2. You can pay Noddle £20 to add a dashboard that helps you 'improve your credit score'. Is this actually worth it/helpful/will it tell me anything I don't know already?

3. What is the main aim? 1 current account, 1 credit card? Or is it ok (and sometimes beneficial) to have more than one? I have also just opened a Tesco ISA.

4. Is it good to keep an overdraft and dip into it and pay it off, just like with credit cards? Or just best not to use it at all?

5. Is it possible to actually SEE your credit score? Or does it not exist? I would like to see it visibly improving as I go along, if you know what I mean.

6. I plan on becoming a house owner in approximately 4 years. Will all the black marks from missing credit card payments go against me getting a mortgage? Or will 4 years down the line be enough for this kind of thing to have been corrected?

Thanks again!!0 -

[/size]well first of all, thanks everyone for your response. You're very helpful! It's also good to know that other people have been in this situation and got out of it

i really like the idea of paying the credit card off with highest interest first, then using it to make my everyday purchases, then paying it off in full at the end of every month. I will be doing that asap.

I have a few more questions if you can help further?

1. I signed up to noddle. It's great! So much easier than experian, plus you can see everything there and then instead of having to send off and pay for a pass code. But my question - it gives me a credit score of 1/5. Everything on my file on noddle is in order (i'm on the electoral role, i have no bankruptcies/insolvencies/judgements on my file, no financial connections). Where can you see the bad stuff? I want to see what it is exactly that is making my score 1/5. Can you view this using noddle? What are the main bad points i should be taking notes from off noddle?

most likely late payment markers and high debt/limit ratios and searches.

2. You can pay noddle £20 to add a dashboard that helps you 'improve your credit score'. Is this actually worth it/helpful/will it tell me anything i don't know already?

it can be helpful for an at a glance view of your credit file but quite honestly you can work out what is wrong without needing a score. Remember that items not appearing on your credit file like income can be just as or if not more important in a lending decision.

3. What is the main aim? 1 current account, 1 credit card? Or is it ok (and sometimes beneficial) to have more than one? I have also just opened a tesco isa.

sounds good, a few lines of different types of credit. The tesco isa will have no effect as it is not a credit product.

4. Is it good to keep an overdraft and dip into it and pay it off, just like with credit cards? Or just best not to use it at all?

have an overdraft but don't generally use it!

5. Is it possible to actually see your credit score? Or does it not exist? I would like to see it visibly improving as i go along, if you know what i mean.

a credit score itself is pretty meaningless, don't waste your money. Just look what is wrong with your files and take corrective action, your file will improve with time and remember that other information not on your credit file could be just as important if not more.

6. I plan on becoming a house owner in approximately 4 years. Will all the black marks from missing credit card payments go against me getting a mortgage? Or will 4 years down the line be enough for this kind of thing to have been corrected?

it may influence the rate you get but if you are responsible with credit from now on then i don't think you will have a problem, negative information is only kept for 6 years from when it is posted.

thanks again!!

..........I have numerous qualifications in Business and Finance, Accountancy, Health and Safety and am now studying Law.

Don't rely on anything I write as it may be wrong!!!0 -

You've had good answers so far so not much to add but:

1) To see the 'bad' stuff, click on the little plus signs next to each credit product. That will show you things like your repayment history for the last few years as well as your limit and balances. Anything orange or red is 'bad' and is what's causing you to have 1/5. (Although the 1/5 doesn't really mean much it gives you an idea).

2) Don't bother, use the £20 towards your CC. All it will tell you is what youve been advised to do here.

3) Multiple accounts can be beneficial but you generally need good credit to get good products. Bear in mind that you may struggle to get new accounts for the next couple of years so don't go closing all of your accounts straight away. The limits you have aren't massive so having the accounts open but with no balance shouldn't go against you.

4) Have an overdraft but keep out of it unless you have no choice. I'd pay it off and reduce it to maybe £250 (lots of unused credit can be viewed as bad). Don't treat the OD like a credit card. Using a CC each month and paying in full = good. Going into your overdraft each month even if you pay it back = bad.

5) Don't worry about it, what you've been advised to do will improve your credit.

6) Like you've already been told. You should get a mortgage but maybe not the best rate. Maybe think about holding off for all the bad stuff to fall off your credit report (6 years since last bad thing) before applying. Use the extra time to save a bigger deposit.0 -

Again, thanks for your help.

The report wasn't as bad as I was expecting.

Natwest CC - 29 green / 2 red (Aug 2012 most recent red)

Barclaycard - 30 green / 3 red (Apr 2012 most recent red)

Egg - 57 green / 0 red

Natwest current acc - 71 green / 0 red

Barclays current acc - 40 green / 0 red

Orange phone - 47 green / 2 red (Mar 2012 most recent red)

So all in all, it looks like I'll have to wait for September 2018 for all reds to drop off my file.

Taking all of your advice into account I am going to:

1. Reduce to one current account, keeping it at about -£250 - not keeping it in credit

2. Reduce to one-two credit cards, using them for my daily spends

3. Pay credit cards off in full every month

4. Apply for maximum two credit schemes/year (but not until I've cleared all my current debt)

5. Wait until Sep 2018 to apply for a mortgage (to get a better one than I would get with reds on my file)

Sounds like a plan!0 -

why have a ISA earning peanuts when you have debts charging high APRs?

madness to reduce your current a/cs to only one.... do you not read the newspapers with tales of banks computer errors, a/cs frozen, ATMs not working etc.

If you loose or have fraud on your debit card you are cash less for a few weeks.

Never had a debit card refused abroad?

and using OD regularly, generally shows poor money management skills and is a real negative on your credit rating... get rid of the OD (unless 0% )

having several CCs is very useful for the same reason as having multiple current a/cs and anyway may have specific benefits (cashback, points, fee-free overseas spending/cash etc.0

{kind=link}

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.5K Banking & Borrowing

- 254.1K Reduce Debt & Boost Income

- 455K Spending & Discounts

- 246.6K Work, Benefits & Business

- 602.9K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards