We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Early-retirement wannabe

Comments

-

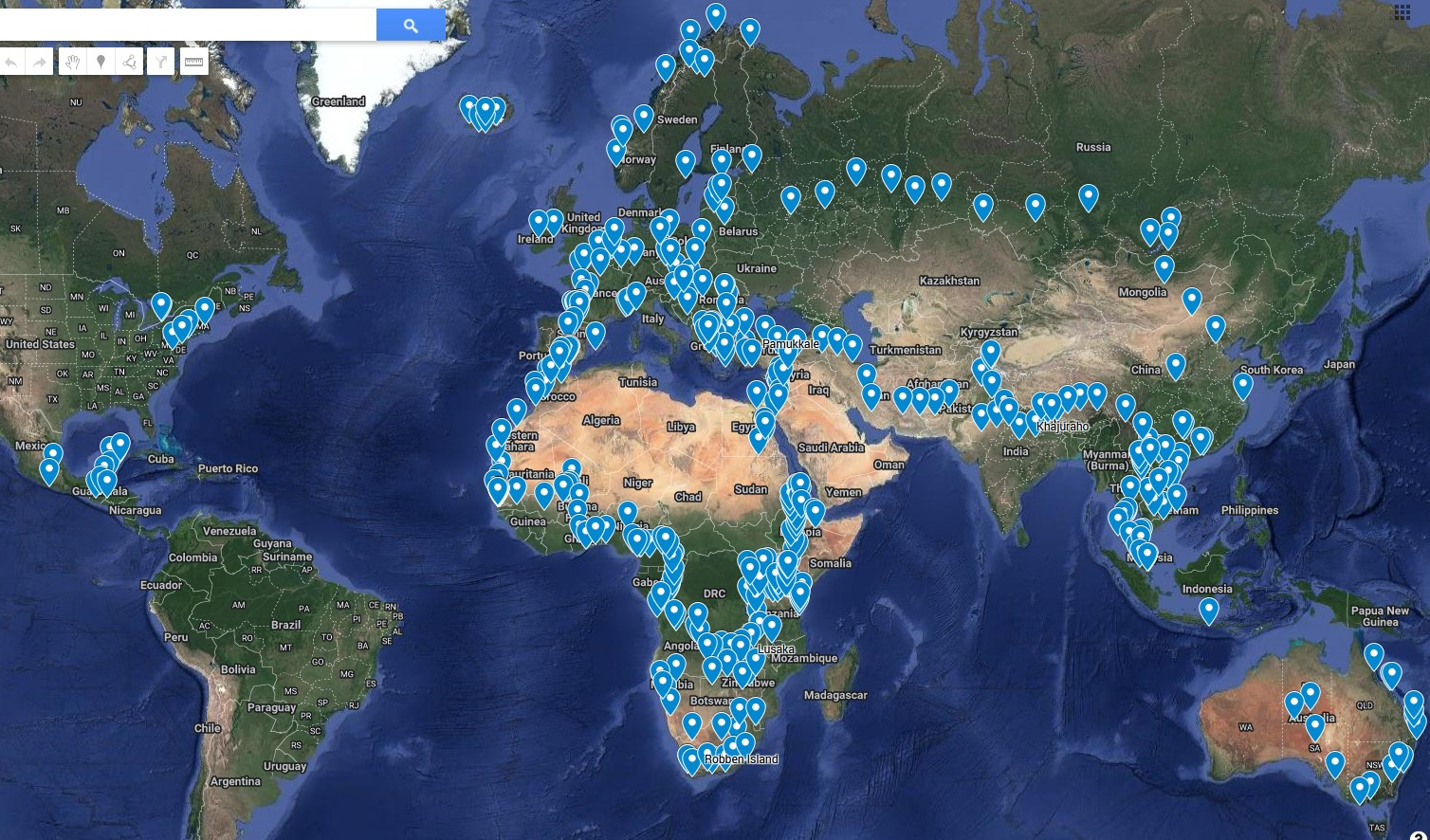

Exactly one month now remains until my last day at work, then we have a couple of weeks to clean house, see family and fly to Anchorage to start our 2 year (ish) travel plan. My wife will get to celebrate her 45th birthday shortly after we set off, when we get to Vancouver. I'll probably celebrate my 45th in Guatemala, a few months into the trip.Things are going amazingly smoothly. I signed the tenancy agreement for my house this week so that is nearly all sorted. I still have just a last few things to sort in terms of getting the house fully ready, but they should all be straightforward and hopefully done over the next couple of weeks.After this week it should mostly be straightforward things to sort out - things like setting up new laptop, learning to use my new GoPro and how to edit video for YouTube and so on. There will then be lots of house accounts to close, and of course the final deep clean of house and final tidying of garden in the last days/weeks.The end is now very much in sight, with just 45 days remaining until we arrive to start our big trip through the Americas. Although I will soon start to fill in the big blank patch on the list of places I've visited, it won't be until at least November that I add a new country to the list of 77 I've visited. Unfortunately, I'll only visit 14 new countries in the Americas, and up to another 3 on the other trips we are likely to take after the Americas. That will be rather frustrating, as I envisaged hitting 100 countries on this trip but that might be quite difficult. I will definitely reach the 100 target at some point, but it might be with European travel after the end of this big trip.Map of places already visited

It was very satisfying to discover I can buy AirBnb gift cards with a 4.5% discount through a workplace scheme - we will be spending many thousands at AirBnb in the coming couple of years!Although very much not wanting to look too far ahead, after the Americas I think there are two trips which are some way ahead of others. First would be fly to Kuala Lumpur, take a ferry to West Sumatra and travel down through Indonesia to Bali, fly from there to Darwin and then travel down to Uluru. That would finally complete an overland journey between London and Sydney (there is no sensible way to arrive in Australia by boat unfortunately, other than on cruises or cargo vessels both of which involve long journeys, not just a trip from Bali to Darwin). After that we would visit friends in Australia and my wife wants to see New Zealand.The other trip I'd like to do would be flying into Addis Ababa to go and see Lalibela, the Danakil Depression, Axum, Gondar, and then take a bus over to Khartoum and on to the Meroe pyramids and up to Abu Simbel and onwards up through Egypt which my wife has never visited. That would then complete a giant overland circle which I've almost travelled, aside from the marked red circle, as a result of various past overland travel. Unfortunately the troubles in northern Ethiopia may make this impossible for a while yet.Map of large overland circle already traveled (gap highlighted)

It was very satisfying to discover I can buy AirBnb gift cards with a 4.5% discount through a workplace scheme - we will be spending many thousands at AirBnb in the coming couple of years!Although very much not wanting to look too far ahead, after the Americas I think there are two trips which are some way ahead of others. First would be fly to Kuala Lumpur, take a ferry to West Sumatra and travel down through Indonesia to Bali, fly from there to Darwin and then travel down to Uluru. That would finally complete an overland journey between London and Sydney (there is no sensible way to arrive in Australia by boat unfortunately, other than on cruises or cargo vessels both of which involve long journeys, not just a trip from Bali to Darwin). After that we would visit friends in Australia and my wife wants to see New Zealand.The other trip I'd like to do would be flying into Addis Ababa to go and see Lalibela, the Danakil Depression, Axum, Gondar, and then take a bus over to Khartoum and on to the Meroe pyramids and up to Abu Simbel and onwards up through Egypt which my wife has never visited. That would then complete a giant overland circle which I've almost travelled, aside from the marked red circle, as a result of various past overland travel. Unfortunately the troubles in northern Ethiopia may make this impossible for a while yet.Map of large overland circle already traveled (gap highlighted) I'm not sure what coming back will look like exactly. We shouldn't need to work again, but Plan A is still to return to London and our previous jobs for up to a year whilst selling house and buying retirement house - not least as that enables us to purchase with an offset mortgage which we would keep fully offset and would provide an option should we want to spend more prior to age 57 which then would be paid back using DC pension. But there are other possibilities, and we might not want to be away for the full 2 years - that is an awful lot of travel. In my experience, Plan A rarely ends up being what actually happens, but there are usually at least some similarities.It is going to be a huge relief when we finally drive away from our house next month and can relax, the last 8 months have been very busy and taxing. But, it does feel great to finally be doing something unusual again, rather than just following a normal Western lifestyle which is very comfortable but rather limiting. Taking unpaid leave from job, leaving the house we have lived in for 12 years and traveling a very long way from all of our friends and family is changing our lives about as much as is possible and it is nice to reset and rethink virtually every single thing we currently do.19

I'm not sure what coming back will look like exactly. We shouldn't need to work again, but Plan A is still to return to London and our previous jobs for up to a year whilst selling house and buying retirement house - not least as that enables us to purchase with an offset mortgage which we would keep fully offset and would provide an option should we want to spend more prior to age 57 which then would be paid back using DC pension. But there are other possibilities, and we might not want to be away for the full 2 years - that is an awful lot of travel. In my experience, Plan A rarely ends up being what actually happens, but there are usually at least some similarities.It is going to be a huge relief when we finally drive away from our house next month and can relax, the last 8 months have been very busy and taxing. But, it does feel great to finally be doing something unusual again, rather than just following a normal Western lifestyle which is very comfortable but rather limiting. Taking unpaid leave from job, leaving the house we have lived in for 12 years and traveling a very long way from all of our friends and family is changing our lives about as much as is possible and it is nice to reset and rethink virtually every single thing we currently do.19 -

I've just found a rather surprising and very unforeseen benefit of this thread. I plan to make a "Contingent Decision" argument under the regulations arising as a result of the McCloud judgment (which affects me), with the argument being that I would have made higher voluntary pension contributions had I not been moved to the Civil Service alpha pension scheme in April 2015 (as pension inputs under the alpha scheme are higher than inputs under the older schemes).That would be extremely hard to clearly evidence in the normal run of events, just relying on data about income, pension contributions and pension inputs to make the argument, but looking back at a post of mine in this thread from 13th April 2014 I wrote (page of comments here, for reference):So far, ISAs have been largely neglected in favour of pensions in my plans, so only have about £40K in ISAs now but that will start to rapidly increase from this year onwards. It will accelerate in 2015/16 as by then I will have used up all my Annual Allowance carry-forward and won't be able to pension off all my higher rate income.I'm fortunate in having kept all key financial records for the period, P60s, Self-Assessment returns, details of pension contributions and Pension Saving Statements for the full 2015-2022 period, so all of that data along with the evidence of a stated intent with a clear date stamp on a large public website should bring about a water-tight contingent decision argumentIt was also extremely interesting looking at a few other posts around that time - 8 years ago - to see how what I was planning back then has turned out. Our ISAs are now up to £333K and some of the other things I wrote at that time are:

The extra flexibility (talking of the then recently announced pension freedoms), plus a slightly better past year than forecast, has brought forward my viable retirement date from 2022 to 2021. Earliest possible date is 2018, 2020 just about doable, 2021 viable and 2022 most likely date. The earlier dates are only possible in the event of inheritance or redundancy offer as they would involve too much of an income sacrifice.As it turned out, we did get one inheritance but it was about a quarter of the maximum amount which could have been possible (which is a good thing, as it means there was only 1 death). We were going to leave in 2021, only for it to be postponed due to COVID. Our actual leaving date ended up being 26th August 2022 so very much in line with planning from 8 years ago.As well as risk of policy change, the main uncertainty left is how to manage the transition between work and retirement and home ownership. Ideally, I'd have a mortgage which is paid off with pension income which would really help balance liquidity efficiently between pre and post age 55 periods. However, when I retire I want to go travelling for a couple of years before returning to a completely different part of UK. Ideally I'd sell house before going travelling but that isn't conducive to keeping a mortgage...so perhaps I might reluctantly rent out house, which should enable me to keep and in due course port a mortgage to a new property when sold a couple of years later. Something I'll worry about as the time gets closer though.I ended up paying off my mortgage in 2020, but will be renting my house out when we go traveling. Plan A is currently to return to work after traveling for a short period (up to about a year at most) during which time I'll buy our retirement house, hopefully using a no-fee offset mortgage such as this. The mortgage will immediately be fully offset, and so provide a no cost pool of easy borrowing should we end up needing it before I can access DC pensions at age 57 which will then provide a nice capital reserve and if necessary be used to once again fully offset mortgage. So slightly different to the approach outlined above, but very much consistent with the line of thought back then.I find it very interesting that despite the finer details of our plans changing a lot, such as the exact age I take each pension, paying off mortgage earlier than anticipated, and higher than expected DC returns (and to a lesser extent, ISA returns), the overall plan has proved very resilient and the outcome in 2022 is almost exactly as I anticipated in 2014 following the big change arising from pension freedoms. It is fair to say there have been quite a few shocks and unexpected political and world events in that time too.4

The extra flexibility (talking of the then recently announced pension freedoms), plus a slightly better past year than forecast, has brought forward my viable retirement date from 2022 to 2021. Earliest possible date is 2018, 2020 just about doable, 2021 viable and 2022 most likely date. The earlier dates are only possible in the event of inheritance or redundancy offer as they would involve too much of an income sacrifice.As it turned out, we did get one inheritance but it was about a quarter of the maximum amount which could have been possible (which is a good thing, as it means there was only 1 death). We were going to leave in 2021, only for it to be postponed due to COVID. Our actual leaving date ended up being 26th August 2022 so very much in line with planning from 8 years ago.As well as risk of policy change, the main uncertainty left is how to manage the transition between work and retirement and home ownership. Ideally, I'd have a mortgage which is paid off with pension income which would really help balance liquidity efficiently between pre and post age 55 periods. However, when I retire I want to go travelling for a couple of years before returning to a completely different part of UK. Ideally I'd sell house before going travelling but that isn't conducive to keeping a mortgage...so perhaps I might reluctantly rent out house, which should enable me to keep and in due course port a mortgage to a new property when sold a couple of years later. Something I'll worry about as the time gets closer though.I ended up paying off my mortgage in 2020, but will be renting my house out when we go traveling. Plan A is currently to return to work after traveling for a short period (up to about a year at most) during which time I'll buy our retirement house, hopefully using a no-fee offset mortgage such as this. The mortgage will immediately be fully offset, and so provide a no cost pool of easy borrowing should we end up needing it before I can access DC pensions at age 57 which will then provide a nice capital reserve and if necessary be used to once again fully offset mortgage. So slightly different to the approach outlined above, but very much consistent with the line of thought back then.I find it very interesting that despite the finer details of our plans changing a lot, such as the exact age I take each pension, paying off mortgage earlier than anticipated, and higher than expected DC returns (and to a lesser extent, ISA returns), the overall plan has proved very resilient and the outcome in 2022 is almost exactly as I anticipated in 2014 following the big change arising from pension freedoms. It is fair to say there have been quite a few shocks and unexpected political and world events in that time too.4 -

hugheskevi said:Map of places already visited

I see from your map that you have yet to visit western australia.

If you come to go in that area, I have visited Perth many times over the years, and one place we love to visit when we can is a small island that you can get to via Ferry from Perth which is called Rottnest Island.

It's home to the quokka, a small wallaby-like marsupial.

They have a wide variety of accommodation that you can choose from Camping, to a hut, to a big Hotel.2 -

I'd love to see a quokka - they are almost cartoonlike in their cutenessrjmachin said:hugheskevi said:Map of places already visited

I see from your map that you have yet to visit western australia.

If you come to go in that area, I have visited Perth many times over the years, and one place we love to visit when we can is a small island that you can get to via Ferry from Perth which is called Rottnest Island.

It's home to the quokka, a small wallaby-like marsupial.

They have a wide variety of accommodation that you can choose from Camping, to a hut, to a big Hotel.I’m a Senior Forum Ambassador and I support the Forum Team on the Pensions, Annuities & Retirement Planning, Loans

& Credit Cards boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com.

All views are my own and not the official line of MoneySavingExpert.1 -

The final day at work has just been completed

") I am aged 44 years and 8 months, wife is 44 years and 11 months old.

I am aged 44 years and 8 months, wife is 44 years and 11 months old.

My wife and I now have a couple of weeks to finish off getting the house ready to let out and see family before we fly over to Anchorage to start traveling, with the trip expected to be around 18-24 months (but no fixed period, will see how things go).

It won't be until mid-October that we start on unpaid leave from work, before that we use up accrued leave. Once we start unpaid leave we will then start getting tax refunds through PAYE. All that along with monthly rent will go a long way toward paying travel costs. We have also pre-funded a fair amount of the first couple of months of the trip, having already paid for an 8-day cruise and 5 weeks of car hire and insurance.

As of today, the financial position (for wife and I combined, we have no debts of any type) stands at:- £87,000 - cash savings to be used for travel, I expect to not need to touch ISA over the next couple of years

- £334,000 - ISA investments to be used between age 47 - 55 (we are both 44 at the moment)

- £583,000 - house value, to be used to fund buying and moving to a new home when we return from traveling

- £49,000 p/a DB pension (pre tax) with uncapped CPI revaluation and indexation from age 55 (or £62,000 p/a from age 60)

- £247,000 DC pension (this will effectively replace State Pension for the years between age 57 and 68, unless we take out a mortgage and then use this to repay that mortgage)

- We will both have full State Pensions from age 67/68 (assuming 68, but currently it is slightly lower for both of us)

I don't know if this will actually be the start of early retirement or not at this stage. I certainly don't envisage much more work if we do go back - probably up to about a year unless something very strange has happened.

Some other random financial stats, remembering these cover both wife and myself:- £3,200 spent improving house before renting it out - largely replacing garden fences destroyed in storm

- £1,700 on letting fees and compliance (ie EPC, EICR and things like changing fuse board which I wouldn't do if living here myself and so don't consider as house improvements)

- £2,000 spent on car hire and insurance (about 6 weeks in total)

- £900 for 8 day cruise (excl tips) between Anchorage and Vancouver

- £800 on travel insurance (18 months)

- £800 for two single flights from Dublin to Anchorage (amount covers both tickets)

- £500 on vaccinations (mostly rabies)

- £264 renewing passports (two UK, one Irish)

- £357 on various other things (ESTA fees, coach booking, malaria tablets, etc)

20 -

Many congrat's hugheskevi. It's finally here!

I hope you (both) have a wonderful time. Something tells me you'll be absolutely fine financially..!😁3 -

@hugheskevi please do pop back and tell us how it is going - maybe splash out on your own dedicated diary thread. I hope you have a brilliant tripI’m a Senior Forum Ambassador and I support the Forum Team on the Pensions, Annuities & Retirement Planning, Loans

& Credit Cards boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com.

All views are my own and not the official line of MoneySavingExpert.5 -

Yes, I second the dedicated diary thread! I am sure all of the regulars on here would like to know how you are getting on from time to time.Think first of your goal, then make it happen!4

-

I haven't posted on this thread previously but read it regularly. I'd be interested to read a dedicated diary thread from @hugheskevi as I have serious travel (and early retirement) envy 😎

Their plans for the next couple of years travelling sound amazing, hope you have a fabulous time!4 -

I think MSE threads are a bit limiting for diaries, and the pension board certainly isn't the place. I plan to go a bit higher tech and use more modern tools but still stay faithful to rigorous data and detail. I'll still put occasional updates on this board, but that will be more focused on big-picture strategic and financial stuff at the end of financial years rather than diary sort of things.

We will be limited by wi-fi/internet availability until our Anchorage to Vancouver cruise finishes, which will be 23rd September, but after that, I plan to upload two YouTube updates per week. That will show what we are doing and how long it took us.

It has long been a frustration of mine that since the age of the internet, travel has collapsed into the vast majority of people doing exactly the same as everyone else, rather than using the vast online resources available to blaze their own trail, so, in addition to the YouTube channel, I will also keep a Google Sheet recording every bit of our expenditure. That will mean anyone can see what we are doing on YouTube, and also what it cost to do it - accommodation, food, travel, activities, everything.

If folk would be interested in a sneak peek, it will be this Google Sheet here. I'll update it each evening of our travels, so over time, it will be a definitive record of where we went, how far we traveled, and how much we spent in every place. For now, it isn't too interesting, just the pre-trip spending I've mentioned above.

And the final data record will be a visual record, using the map here, which has everything for the first two weeks logged, and which I will update each day so that we have a visual record of the entire trip showing where we went.

That should give a nice set of tools documenting what we are doing, where we are doing it, how long it took, and how much it all cost. That would then enable anyone to replicate a portion of the trip if they wished, knowing exactly what they would see and how much it would cost. Not I expect anyone to do so, but it might give some people a few new ideas along with detailed data to inform them.

I'll post a link to the YouTube channel when it is up and running, but the links above will always be the very latest update. The YouTube channel will be the heart of things, with the spreadsheet and map linked from it.

I just have to learn how to use my GoPro Hero 9 and how to edit video for YouTube in the next few weeks!

16

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards