We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Unenforceability & Template Letters III

Comments

-

never-in-doubt wrote: »Don't waste time with this notion right now mate - its an unenforceable account as things stand and going on MBNA's past performances, i'd not be too worried at this stage that they will comply.

Just stick to the plan - this is a technicality issue that you don't need right now!

OI Chippy - shurrup will ya! (or i'll pinch your [STRIKE]meat[/STRIKE] bird!) :rotfl: :rotfl:

OK letter sent by 1st class recorded") 0

0 -

Thanks

not sure how you quote (tell me please!) but you said:

What happened? Did you send back to wescot or send to the OC?

I sent it back to Wescot.

I have posted reminders to them all today, except for Apex (who I will leave alone now), is this the right thing to do?

I sent CCA requests to everyone that i had an credit agreement with, the others that i was referring to (sending change of addresses to) were utility companies etc., all of my debts were on my DMP apart from a CCJ which i am paying independently to get it paid quicker.

It is almost 30 days since i first wrote to them - do i need to do anything else?

Missal0 -

Sorry forgot to ask,

Should i send your copy of the formal demand to my creditors who have filed defaults against me or should i sit and wait for replies and where they do not comply with my request correctly send it then?

must admit your letter is much better than the one i found just couldn't find it on here for some reason.

To date i have sent my letter requesting default proof to barclays(current account), o2(mobile phone account) and 3g(broadband account) all of whom i could not CCA. I have not sent default letters to any of the ones where i have sent cca, as i though as part of the process, if thy have not complied that i would request removal at that time.

Am i right or wrong - don't want to send duplicate letters confusing everything and making myself look a dummy (even though that's what i am!)

Missal0 -

HI Nid - hope you are well.

I just need a bit of advice please. I have got a CCJ because of a Marks & Spencers account that was opened in 2002. I have just received a CCA from them for another account that was opened in 1997 which has come back completely unenforceable as none of the prescribed terms are on the signature page and hasn't been signed by themselves :j:j(another £3000 that is unenforceable - thank you so much as it makes 11 accounts in total so far :rotfl::rotfl::rotfl:).

My question is would it be worth CCA'ing the CCJ'd account and if it came back unenforceable would I be able to get the CCJ removed and to stop payments or is it too late as it has already been registered? Unfortunately I found this thread after the CCA had been registered.

With many thanks for all you help - you are a star! (listen to the sucking up again!!!)0 -

Niddy, When you get a moment, could you please have a look at the following,

Amex 60 sec app form

4 page reply from Amex to the CCA request & follow up dispute

2 pages of Terms & conditions but in page 2 of their letter they say " If you have retained a copy of the original agreement, you will note that on the reverse of the agreement are the original Terms & Conditions applicable to the account."

So how can they fit these two pages onto the reverse of the original agreement?

Having read the enclosed do you think its enforceable or not and what should be the next step? Despite the account being in default (CCA dispute already sent) there have been letters from Westminster Solicitors, RMA Management Alternatives and now Newman Collections, some offering a chance to make an offer, others threatening all sorts of usual stuff.

Thanks

http://i769.photobucket.com/albums/xx337/zzm59/AMEX60Secform.jpg

http://i769.photobucket.com/albums/xx337/zzm59/AMEXpage1.jpg

http://i769.photobucket.com/albums/xx337/zzm59/AMEXpage2.jpg

http://i769.photobucket.com/albums/xx337/zzm59/AMEXpage3.jpg

http://i769.photobucket.com/albums/xx337/zzm59/AMEXpage4.jpg

http://i769.photobucket.com/albums/xx337/zzm59/AMEXTCp1.jpg

http://i769.photobucket.com/albums/xx337/zzm59/AMEXTCp2.jpg0 -

Thanks

not sure how you quote (tell me please!) but you said:

Click this type logo thingy-mejiggy! What happened? Did you send back to wescot or send to the OC?

What happened? Did you send back to wescot or send to the OC?

I sent it back to Wescot.

GoodI have posted reminders to them all today, except for Apex (who I will leave alone now), is this the right thing to do?

Yes, well done. As for Apex, again, that's fine to ignore them now....It is almost 30 days since i first wrote to them - do i need to do anything else?

Nope - wait and see what they send back....

2010 - year of the troll

2010 - year of the troll

Niddy - Over & Out :wave:

0 -

Sorry forgot to ask,

Should i send your copy of the formal demand to my creditors who have filed defaults against me or should i sit and wait for replies and where they do not comply with my request correctly send it then?

must admit your letter is much better than the one i found just couldn't find it on here for some reason.

To date i have sent my letter requesting default proof to barclays(current account), o2(mobile phone account) and 3g(broadband account) all of whom i could not CCA. I have not sent default letters to any of the ones where i have sent cca, as i though as part of the process, if thy have not complied that i would request removal at that time.

Am i right or wrong - don't want to send duplicate letters confusing everything and making myself look a dummy (even though that's what i am!)

Missal

What you do is exhaust unenforceability route first then you move to the default removal..... so in your case send CCA request, then reminders then see what happens....

The default letter demand is a last resort..... 2010 - year of the troll

Niddy - Over & Out :wave:

0 -

My question is would it be worth CCA'ing the CCJ'd account and if it came back unenforceable would I be able to get the CCJ removed and to stop payments or is it too late as it has already been registered? Unfortunately I found this thread after the CCA had been registered.

Hiya

Of course you can check for unenforceability but the best person to speak to about CCJ's is my matey 10past6.

Send him a PM (say Niddy sent you) and ask him about it cos he will be able to check the process etc and confirm your next steps - when it comes to court stuff, he's your man.... I'll carry on with the unenforceability part for you though unless 10past6 says otherwise.

But yea, send the CCA Request to get the ball rolling then we'll establish whether the CCJ was issued properly... I'd assume that 10past6 will be asking to see a copy of the default notice and notice of termination etc so may be worth digging those out.... 2010 - year of the troll

Niddy - Over & Out :wave:

0 -

hiya Niddy and all

just popped in to try and catch up on the thread its a bit longer to when i left off so will take proper time out to read all posts later today

however, ive linked this thread to another i came across this morning to help those guys out i hope that was okay

the more that see this wonderful thread of yours the better and we can try and put a lot more people at ease with their fears and take positive action

however the thread is http://forums.moneysavingexpert.com/showthread.html?t=2269023

still putting all my paperwork in order and trying to find all default notices and any termination letters together so i can take further advice later

but what a week ive had with my first signing on the dole ever in my life it was an experience and half, im going to start a thread on my journey need to vent somehow

have a fun weekend all and happy mums day to all tomorrow:beer:

catch up later mazSealed Pot Challenge member 1525

"Knowledge is the Power to get Debt Free":j

Truecall device, stops all the unneccesary phone calls - my sanity has been restored and the peace in the house is truely priceless!:rotfl:0 -

Goodtimesahead wrote: »Niddy, When you get a moment, could you please have a look at the following,

It is unenforceable - see response below:

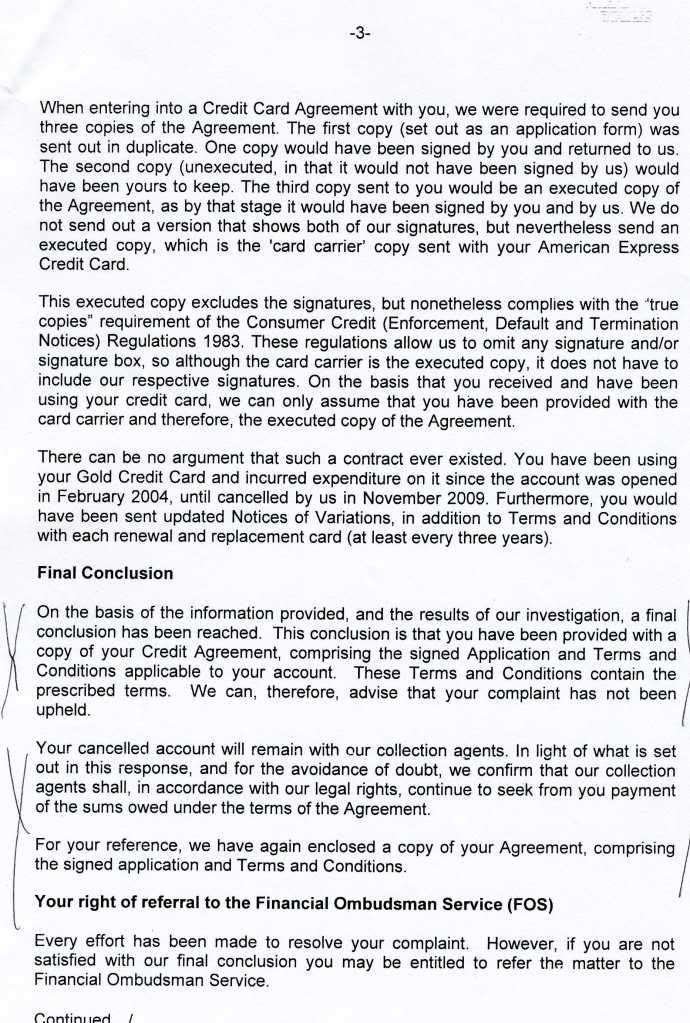

Send this off to them and also, send a copy of it to the latest DCA that has been hassling you along with a copy of this letter: Account sold whilst in Default of CCA RequestDear Sirs,Account No: XXXXXXXXI write with reference to previous correspondence, and in particular to the above numbered account which, for ease and clarity, I hereby deem unenforceable in line with s.127(3) CCA(1974) and this letter is my final response on the matter.

In my original letter, dated XX/XX/XXXX, I requested a copy of the credit agreement to which I genuinely expected to receive an exact copy of that which you hold in your records i.e. an actual photocopy of the agreement which is allegedly signed by myself and your representative, this is what you refer to as "copy 3" of the alleged 3 copies that you deem to retain. You said yourself, in this letter that the third copy is the executed agreement.

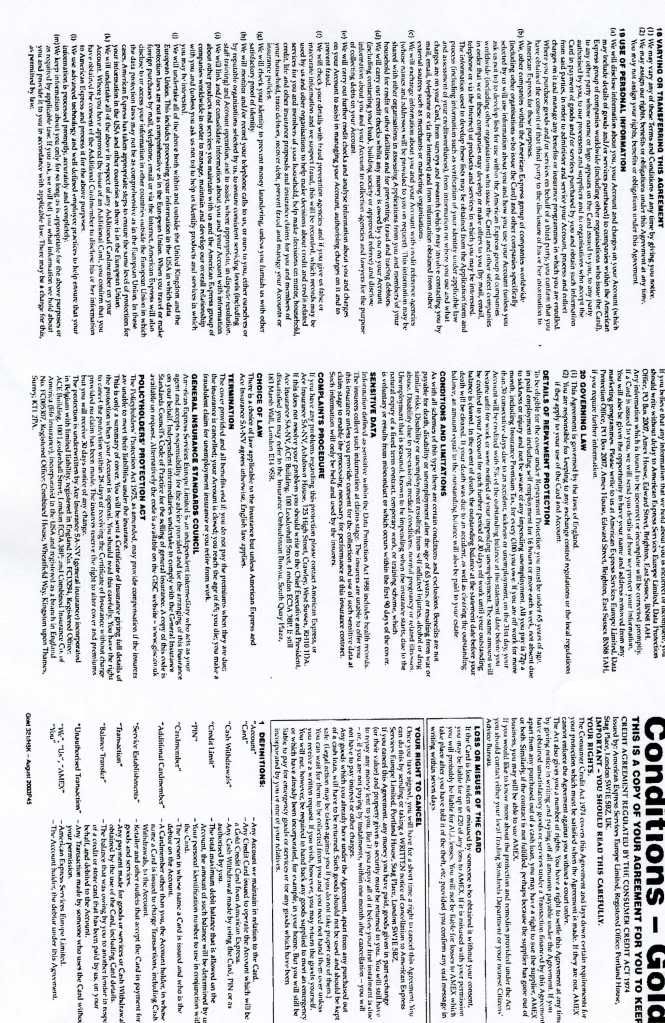

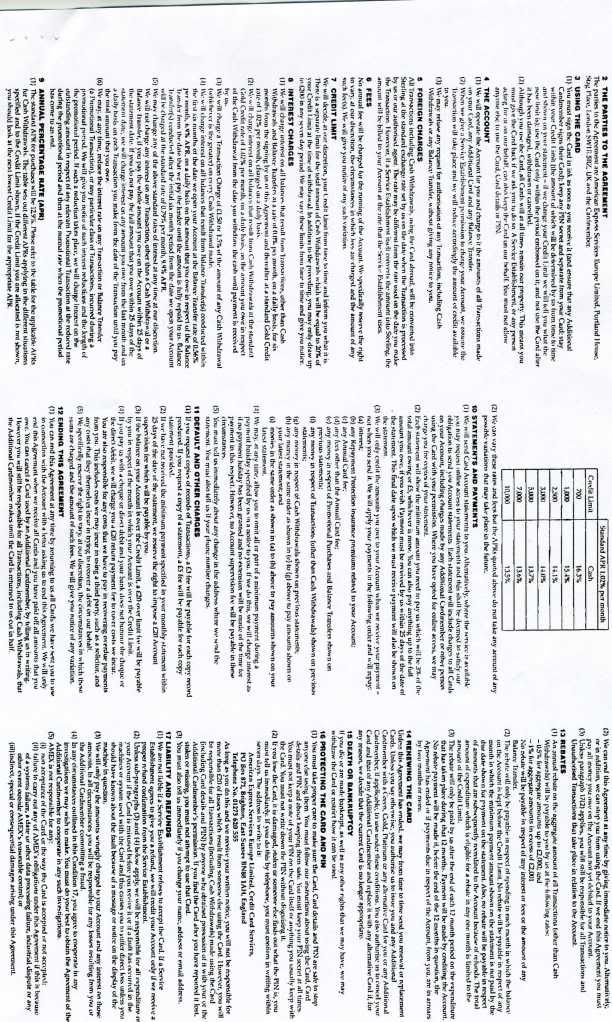

Whilst I appreciate that under the Consumer Credit (Cancellation Notices and Copies of Documents) Regulations 1983 you are able to omit a signature and date box from the copy, however I would like to hold in my records an exact copy of the executed document that bears both our signatures. I do not want a piece of paper that alludes to there being an agreement; i.e. a 60 Second Application Form.

Going back to your letter you state that because I allegedly used the account, this constitutes acceptance of your terms - well yes, it would if the agreement was enforceable but as we both know, account useage does not constitute enforceability.

Similarly, you've tried to explain your understanding of the prescribed terms, as defined in sch.6 (CCA1974) but I think you're missing the point in that these terms must be present on the signatory page of a clear agreement that does not mislead in any way. An application form is in no way referred to as an executed agreement and any judge that handles this case will be duty bound under s.127(3) not to pass judgement until such time you supply me with an executed copy of the agreement.

Regards to the terms you sent me, need I remind you that you should be sending, as part of s.78, a copy of the terms in place as at the time of signature and a copy of the most recent terms as at todays date. However what is interesting is that you claim that the terms were on the back of the 60 second application - how so? This was one page (I assume) yet you sent two pages of terms apparently relevant as at the date of application - how, therefore, did you get two A4 pages of terms from the back of one A4 sheet?

You then go on to state that within the signature box it has a phrase along the lines of "only sign if you want to be legally bound by its terms" - but unfortunately, this is another mistake because the prescribed terms are in fact supposed to be present on the signatory page or linked directly to additional sheets, for example "only sign if you want to be legally bound by the attached terms noted as page 2 of 2". By agreeing to blanket terms, there is no possible way to keep control of any agreement and therefore the linking to separate pages is key in my argument. I suggest you seek proper legal guidance on this issue prior to responding as you clearly lack the necessary knowledge required to counter-argue this point.

You are reminded that "reasonable collection activity" is acceptable in light of the recent McGuffick v RBS case but that does not allow you to act irresponsible or in a threatening or misleading way. I refer you to the recent OFT Guidance that was issued after the conclusion of the recent Carey V HSBC {and others} case in the Manchester courts.

Usual OFT Guidance clearly states that lenders would be acting unfairly, and potentially in breach of their consumer credit licenses, if they misled borrowers by:• hiding or disguising the fact that there was never a proper signed agreement in the first placeIn light of the above, I consider this account to be unenforceable until such time you properly comply with my original s.78 request and send a photocopy of the original purported document, signed by both parties with compliant terms, if such a document exists. If it does not, then you must confirm this to me in line with your licensing guidance, as detailed above.

• providing only a copy of the current terms and conditions, not the original ones

For clarification, the document you sent, purporting to be a credit agreement, does not contain all of the prescribed terms as required by section 60(1) Consumer Credit Act 1974. The Consumer Credit (Agreements) Regulations 1983 (SI 1983/1553) made under the authority of the “1974 Act” sets out what the prescribed terms are, I refer you to Schedule 6 Column 2 of SI 1983/1553 for the definition of what is required. Suffice to say, all of the required terms are not present within this document. Since this document does not contain the required prescribed terms it is rendered unenforceable by s127 (3) consumer Credit Act 1974, which states:127(3) The court shall not make an enforcement order under section 65(1) if section 61(1)(a)(signing of agreements) was not complied with unless a document (whether or not in the prescribed form and complying with regulations under section 60(1)) itself containing all the prescribed terms of the agreement was signed by the debtor or hirer (whether or not in the prescribed manner).This situation is backed by case law from the Lords of Appeal in Ordinary (House of Lords) the highest court in the land. Your attention is drawn to the authority of the House of Lords in Wilson-v- FCT [2003] All ER (D) 187 (Jul) which confirms that where a document does not contain the required terms under the Consumer Credit Act 1974 the agreement cannot be enforced.

In addition should you continue to pursue me for this debt you will be in breach of OFT guidelines. These guidelines (issued July 2003 & updated December 2006) relate to debt collections and what the OFT considers unfair, I have enclosed an excerpt from page 5 of the guidance which states;2.6 Examples of unfair practices are as follows:As this account is clearly unenforceable, I expect you to write back and confirm that no further action will be taken and that the account is now closed and no further correspondence will take place; irrespective, unless you do supply a copy of the original agreement I will not correspond with you again and any threats will be averred and unlawful and vexatious with a counter-claim forthcoming.

h. Ignoring and/or disregarding claims that debts have been settled or are disputed and continuing to make unjustified demands for payment

Yours faithfullySign digitally 2010 - year of the troll

Niddy - Over & Out :wave:

0

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards