We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Would you accept?

Comments

-

Just rememberedricky_balboa wrote: »Should i give more detail that they didnt reply to CCA requests") you could raise a complaint here re non compliance with your CCA request, you could use this "complaint "as evidence to support your defence Click here for Martins (MSE) advice on who to contact with Debt Issues - YOU HAVE NO REASON TO USE A FEE PAYING DEBT MANAGEMENT COMPANY- THEY CANNOT DO ANYMORE FOR YOU THAN THOSE LISTED IN MY LINK ABOVE.

you could raise a complaint here re non compliance with your CCA request, you could use this "complaint "as evidence to support your defence Click here for Martins (MSE) advice on who to contact with Debt Issues - YOU HAVE NO REASON TO USE A FEE PAYING DEBT MANAGEMENT COMPANY- THEY CANNOT DO ANYMORE FOR YOU THAN THOSE LISTED IN MY LINK ABOVE.

All information given by myself is offered informally and without prejudice - if in doubt seek help from a qualified and insured professional0 -

10past6,

I will fill in the complaints form on the Information Commissioner`s Office website, but i dont think i will have time now to include it in my letter.

Could i use it later as evidence?

Here is the finished letter (hopefully)

does it look ok?In the Swindon county court

Claim number

Between

Nationwide Building Society - Claimant

and

- Defendant

Defence

1. I am the defendant in this action and make the following statement as my defence to the claim made by Nationwide Building Society

2. Except where otherwise mentioned in this defence, I neither admit nor deny any allegation made in the claimants Particulars of Claim and put the claimant to strict proof thereof.

3. The Defendant is embarrassed in pleading to the Particulars of Claim as it does not comply with CPR part 16. In this regard I wish to draw the courts attention to the following matters;

4a) The Particulars of Claim are vague and insufficient and do not disclose an adequate statement of facts relating to or proceeding the alleged cause of action. No particulars are offered in relation to the nature of the written agreement referred to, the method the claimant calculated any outstanding sums due, or any default notices issued or any other matters necessary to substantiate the claimant's claim.

b) A copy of the purported written agreement that the claimant cites in the Particulars of Claim, and which appears to form the basis upon which these proceedings have been brought, has not been served attached to the claim form.

c) A copy of any evidence of both the scope and nature of any default, and proof of any amount outstanding on the alleged accounts, has not been served attached to the claim form.

5. Notwithstanding matters pleaded, it is denied that the Claimant has established a cause of action or that the claimant has a valid claim against the defendant.

Consequently, it is proving difficult to plead to the particulars as matters stand.

The Request for Disclosure

6. Further to the case, on 08/04/2010 I requested the disclosure of information pursuant to the CPR 31.14 (letter attached marked Exhibit A), which is vital to this case from the claimant.

7. To Date the claimant has not replied to my request under the CPR and I have not received any such documentation requested. As a result it has proven difficult to compose this defence without disclosure of the information requested, especially as I am a Litigant in Person.

8. Also, on four separate occasions 25/01/2010, 29/01/2010, 17/02/2010 & 16/03/2010 I requested that the claimant provide a true copy of the executed credit agreement, which they claim exists between parties pursuant to section 78(1) Consumer Credit Act 1974. The Consumer Credit (Prescribed Periods for Giving Information) Regulations 1983 sets out that the claimant must comply with such request in 12 working days of receipt of such request. (Copies of the letters are included as Exhibit") .

.

8. The courts attention is drawn to the fact that without disclosure of the requested documentation pursuant to the Civil Procedure Rules I have not yet had the opportunity to assess if the documentation which the claimant claims to be relying upon to bring this action even contains the prescribed terms required in Consumer Credit (Agreements) Regulations 1983 which was amended by Consumer Credit (Agreements) (amendment) Regulations 2004. The prescribed terms referred to are contained in schedule 6 column 2 of the Consumer Credit (Agreements) Regulations 1983.

9. The courts attention is drawn to the fact that where an agreement does not have the prescribed terms as stated in point 8 it is not compliant with section 60(1) Consumer Credit Act 1974 and therefore not enforceable by s127 (3). There is case law which confirms that where a document does not contain the required terms under the consumer credit act 1974 and the Consumer Credit (Agreements) Regulations 1983 and Consumer Credit (Agreements) (Amendment) Regulations 2004 the agreement cannot be enforced

It is submitted that if the credit agreement supplied falls foul of the Consumer Credit (Agreements) Regulations 1983 in so far that the prescribed terms are not contained within the agreement then the court is precluded from enforcing the agreement. The prescribed terms must be with the agreement for it to be compliant with section 60(1) Consumer Credit Act 1974. In addition there is case law from the Court of Appeal which confirms the Prescribed terms must be contained within the body of the agreement and not in a separate document.

10. If the agreement does not contain these terms in the prescribed manner it does not comply with section 60(1) CCA 1974, the consequences of which means it is improperly executed and only enforceable by court order.

11. Notwithstanding points 8 and 9, any such agreements must be signed in the prescribed manner by both debtor and creditor. If such a document is not signed by the debtor the document cannot be enforced by way of section 127(3) Consumer Credit Act 1974

12. The claimant is therefore put to strict proof that such a compliant document exists

13. Should the issue arise where the claimant seeks to rely upon the fact that they can show that the defendant has had benefit of the monies and therefore the defendant is liable, I refer to and draw the courts attention to the judgment of Sir Andrew Morritt in the case of Wilson v First County Trust Ltd - [2001] 3 All ER 229, [2001] EWCA Civ 633 in the Court of Appeal.

The Need for a Default notice

14. I put the claimant to strict proof that any alleged default notice sent to me was valid. I note that to be valid, a default notice needs to be accurate in terms of both the scope and nature of breach and include an accurate figure required to remedy any such breach. The prescribed format for such document is laid down in Consumer Credit (Enforcement, Default and Termination Notices) Regulations 1983 (SI 1983/1561) and Amendment regulations the Consumer Credit (Enforcement, Default and Termination Notices) (Amendment) Regulations 2004 (SI 2004/3237)

15. Failure of a default notice to be accurate not only invalidates the default notice, but is a unlawful rescission of contract which prevent the court enforcing any alleged debt,.

Conclusion

16. The Defendant denies that there has been any failure to make payment in accordance with the alleged contract. The Claimant has failed to produce a copy of a credit agreement in the requisite timescale/at all, and in the absence of such an agreement, which conforms to sections 60 and 61 of the Consumer Credit Act 1974, the Defendant avers that no agreement has ever existed for there to have been any failure to make said payment.

17. Without Disclosure of the relevant requested documentation I am unable to assess if I am indeed liable to the claimant, nor am I able to assess if the alleged agreement is properly executed, contain the required prescribed terms, or correct figures to make such an agreement enforceable by virtue of s127 Consumer Credit Act 1974

18. In view of the matters pleaded above, I respectfully request that the court gives consideration to whether the claimant's statement of case should be struck out as disclosing no reasonable grounds for bringing the claim, and/or that it fails to comply with CPR Part 16

19. Alternatively, should the court order the claimant to produce the necessary documentation. I will then be in a position to file a fully particularised defence and will seek the courts permission to amend my statement of case accordingly.

Statement of Truth

I, believe the above statement to be true and factual

Signed0 -

That's OK

Remember "at this stage" you only need to submit a brief defence, you'll need to submit a FULL defence at least 7 days BEFORE your hearing Click here for Martins (MSE) advice on who to contact with Debt Issues - YOU HAVE NO REASON TO USE A FEE PAYING DEBT MANAGEMENT COMPANY- THEY CANNOT DO ANYMORE FOR YOU THAN THOSE LISTED IN MY LINK ABOVE.

All information given by myself is offered informally and without prejudice - if in doubt seek help from a qualified and insured professional0 -

Hi 10past6 & all,

Sent the defence letter this morning special delivery.Will phone the court tomorrow to check its arrived.

Had a letter today from Nationwide, it is a reply to my CPR 31.14 request sent on 8/4.

The letter says in as many words:-

"thank you for the letter, i have contacted the relevant area to obtain a copy of the credit agreement.Once i have it i will send it.I dont anticipate it taking longer than a further 7 days.Please find enclosed the default notice and final notice that were sent to you prior to litigation commencing".

The letter is from the legal advisor,lending control legal services.

Now i dont know what everyone else thinks but isnt the following link something to smile about?

http://i740.photobucket.com/albums/x...ispute/IMG.jpg

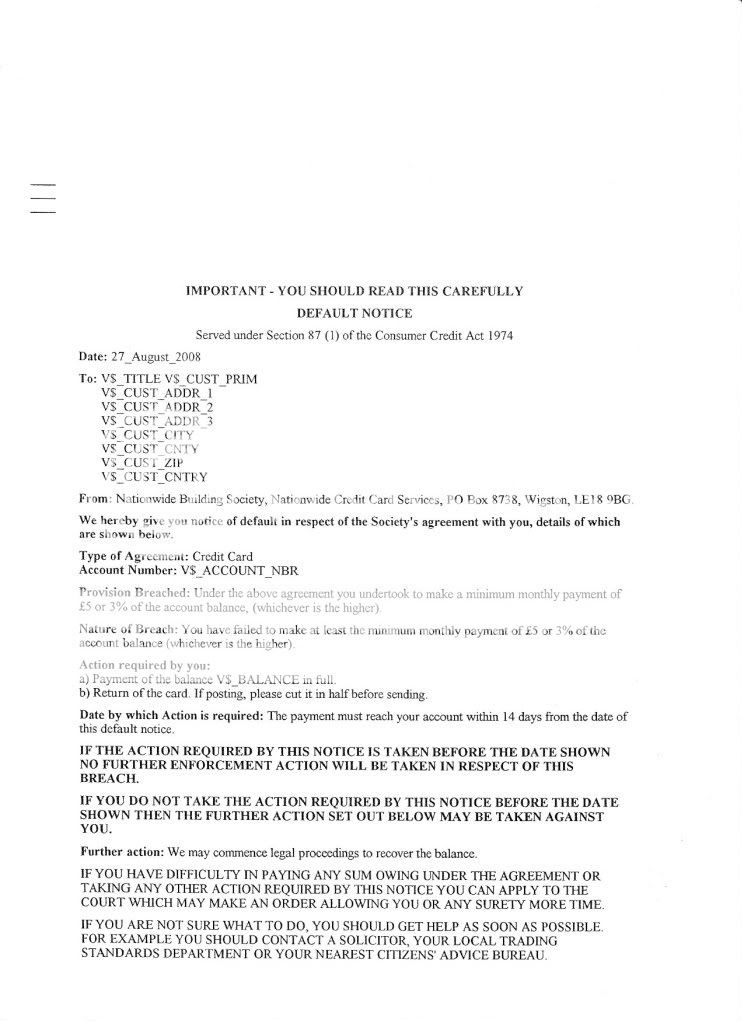

This is the default notice they sent me. The default notice they sent me before litigation is in Nov 09 not Aug 08.There are no details of me on this letter (i didnt even have to blank anything out!!).I had no default letters sent in Aug 08, i made a late payment but that was it.

The final notice letter is also dated 27th Aug 08!, and is written as the same format with no details of mine on it.Just the same v$_CUST_ etc marked on it.The account was used long after Aug 08!

Does anyone wonder what this is all about, do you think they have any letters on file addressed to me?They still have a couple of weeks till the Subject access request deadline.

Is this a proper reply to a CPR 31.14?

Willi ever get my CCA!?! 0

0 -

If they're in default of your CCA request, leave it at that, it's sufficient enough at this stage as a defencericky_balboa wrote: »Willi ever get my CCA!?! Click here for Martins (MSE) advice on who to contact with Debt Issues - YOU HAVE NO REASON TO USE A FEE PAYING DEBT MANAGEMENT COMPANY- THEY CANNOT DO ANYMORE FOR YOU THAN THOSE LISTED IN MY LINK ABOVE.

All information given by myself is offered informally and without prejudice - if in doubt seek help from a qualified and insured professional0 -

-

Hi all,

Finally had a letter from nationwide, which they say is my credit card agreement.It is a reply to my CPR31.14 request, I was sent several copies of the same pages for some reason (about 4 of each).

Here are all the pages sent to me, what do you guys think??

http://s740.photobucket.com/albums/xx49/slightly78/cca%20nationwide/

thanks for any advice as always.0 -

Hi

Can you go back in an delete the account number and application number, as therse are idenfiableIf you've have not made a mistake, you've made nothing0 -

thanks RAS....done...didnt notice!0

-

Does anyone else think this CCA sent to me is incomplete?0

{kind=link}

{kind=link}

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards