We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

CAA request updates / results part 2

Comments

-

Hi all!!!

Not been on here for ages due to all creditors being extremely quiet for a while!!! But I'm again after some sound advice!

But I'm again after some sound advice!

Firstly though, congrats Stapley on the success of your first thread! Now there's a brand spanking new one to fill up!;)

Anyway, back to the point with a quick recap about me. Been on a DMP since October 2007 and gradually starting to make a dent in the initial debt of approx £38,000!!!:eek::o Currently all going well, with all creditors playing ball and acccepting repayment offers, apart from Lloyds TSB credit card who have now been removed from said DMP and haven't been paid anything since January 2009. Currently fighting for ppi refund on this and complaint is now with FOS, but that is another story!;)

My problem is now with Equidebt, who are now in control of my former MBNA credit card account. I CCA'd them way back in March and they eventually replied in June with a dodgy looking copy of my "application form". The terms and conditions were apparently pasted down the side of the A4 size sheet according to some people who viewed it and were not part of the original document. The document was also illegible in parts, none conformance of CCA request me thinks! They rekon it is completely enforceable and that they have fulfilled their obligatons for this! Blah Blah Blah!

So not satisfied with this, I sent them a SAR request to see if they came up with anything else which resembled a credit agreement. This was in September. The 40 days passed and nothing came, despite them cashing the cheque and signing the recorded delivery slip. I sent them a reminder and a further 7 days to comply, but nothing!:mad: I dont even know if they have bought the debt or if they have any right to collect on it as I cant recall receiving any notice of assignment. Obviously, a SAR would also confirm this.

The thing is I have said that I will stop all payments if they do not comply and that they will have to take me to court to get any more money out of me if they are removed from my DMP. But, i'm reluctant to do this as the DMP is running along nicely and they are accepting the payments. The whole point in me seeing how valid the credit agreement was, was to offer a full and final that refected this. Unenforceable agreement equals really low offer to settle.

So what do I do next? Do I stop paying them and let them take me to court?:eek:Or do I just keep paying them their monthly installment and do nothing? They have blatently no regard for consumer laws, so I really dont want to let them get away with this, but the thought of going to court is not one I relish, even if I believe the agreement is unenforceable. Either way, I will report them to the Information Commissioner, but after reading hundreds of similar posts on the CAG website, I doubt this would make any difference!

I've been selling stuff left right and centre on Ebay to build up a F&F pot, so have some money set aside, however, i've seriously been considering using this money and appointing a local solicitor to check the agreement and represent me if this does end up going to court.

Any advice would be greatly appreciated as always.

Cocker:)0 -

Cocker,

They will not take you to court and without sight of the original agreement then they will lose in court anyway. If you say they sent you terms and conditions/application form or an illegible copy then there are templates for both in this thread: #18

I wouldn't worry though, if they threaten you with court action then just commence with CPR31.16 (disclosure) to see their version of the original document (assuming they have it), at which point you then agree to repay or decline as appropriate.

Paying a F&F will not help your credit file.... but if you do consider this, then here is a template: #10 2010 - year of the troll

2010 - year of the troll

Niddy - Over & Out :wave:

0 -

Many thanks for the reply n-i-d!

I've already sent a reply to the CCA and they replied stating that it was clearly legible and that they were sending nothing else.

At first, I thought it looked enforceable, as the prescribed terms were down the side and my signature was on it. However many people commented that the "t's and c's" looked liked they had been pasted on to the form as the MBNA agreements from 2003 never contained them on the application form. Also, they was no signature from MBNA.

There is a link to it somewhere on the old thread.

I have read about the CPR route over on the CAG website, but it just gets me bogged down with legislation everytime I read more and more! The template letters over they seem so complicated and I must say that I get lost with it all!:o

Cocker:)0 -

Many thanks for the reply n-i-d!

I've already sent a reply to the CCA and they replied stating that it was clearly legible and that they were sending nothing else.

At first, I thought it looked enforceable, as the prescribed terms were down the side and my signature was on it. However many people commented that the "t's and c's" looked liked they had been pasted on to the form as the MBNA agreements from 2003 never contained them on the application form. Also, they was no signature from MBNA.

There is a link to it somewhere on the old thread.

I have read about the CPR route over on the CAG website, but it just gets me bogged down with legislation everytime I read more and more! The template letters over they seem so complicated and I must say that I get lost with it all!:o

Cocker:)

Hiya - ok, well first off CPR is a distant dream, so is court! The last thing they would want to do is pursue court action, especially in light of the 2 test cases dropping the day before! Both were MBNA (the lead bank in the test case - 8 are theirs!)....

So you're left with the option of leaving the account in dispute or paying the debt via a payment plan or whatever. But bear in mind, just cos the lender says 'tough !!!!!!, that's all we're sending you' doesn't mean that you have to accept it. If you're positive that it is unenforceable then you stick to your guns and do not pay them and leave it in dispute. Any action they then take would be looked at dimly due to the fact you're disputing the account - Action cannot be taken against a disputed account (enforcement/harassing methods etc).

Therefore it would be best to send one of the templates just so they know you're not happy, and the reasons why you're not happy. It is for them to prove to you that it is indeed enforceable, not for you to prove otherwise. If they do not respond then let them take you to court - you'd win hands down!

I wouldn't worry so much - just send the letter and take a back seat and wait for them to make a move then post back again..... the guys on CAG will be right if they checked the CCA - so do whatever you feel best with - but don't be worrying - no need to worry (you're always in control). 2010 - year of the troll

Niddy - Over & Out :wave:

0 -

OMG Cocker where have you been:DHi all!!!

Not been on here for ages due to all creditors being extremely quiet for a while!!! But I'm again after some sound advice!

Firstly though, congrats Stapley on the success of your first thread! Now there's a brand spanking new one to fill up!;)

Anyway, back to the point with a quick recap about me. Been on a DMP since October 2007 and gradually starting to make a dent in the initial debt of approx £38,000!!!:eek::o Currently all going well, with all creditors playing ball and acccepting repayment offers, apart from Lloyds TSB credit card who have now been removed from said DMP and haven't been paid anything since January 2009. Currently fighting for ppi refund on this and complaint is now with FOS, but that is another story!;)

My problem is now with Equidebt, who are now in control of my former MBNA credit card account. I CCA'd them way back in March and they eventually replied in June with a dodgy looking copy of my "application form". The terms and conditions were apparently pasted down the side of the A4 size sheet according to some people who viewed it and were not part of the original document. The document was also illegible in parts, none conformance of CCA request me thinks! They rekon it is completely enforceable and that they have fulfilled their obligatons for this! Blah Blah Blah!

So not satisfied with this, I sent them a SAR request to see if they came up with anything else which resembled a credit agreement. This was in September. The 40 days passed and nothing came, despite them cashing the cheque and signing the recorded delivery slip. I sent them a reminder and a further 7 days to comply, but nothing!:mad: I dont even know if they have bought the debt or if they have any right to collect on it as I cant recall receiving any notice of assignment. Obviously, a SAR would also confirm this.

The thing is I have said that I will stop all payments if they do not comply and that they will have to take me to court to get any more money out of me if they are removed from my DMP. But, i'm reluctant to do this as the DMP is running along nicely and they are accepting the payments. The whole point in me seeing how valid the credit agreement was, was to offer a full and final that refected this. Unenforceable agreement equals really low offer to settle.

So what do I do next? Do I stop paying them and let them take me to court?:eek:Or do I just keep paying them their monthly installment and do nothing? They have blatently no regard for consumer laws, so I really dont want to let them get away with this, but the thought of going to court is not one I relish, even if I believe the agreement is unenforceable. Either way, I will report them to the Information Commissioner, but after reading hundreds of similar posts on the CAG website, I doubt this would make any difference!

I've been selling stuff left right and centre on Ebay to build up a F&F pot, so have some money set aside, however, i've seriously been considering using this money and appointing a local solicitor to check the agreement and represent me if this does end up going to court.

Any advice would be greatly appreciated as always.

Cocker:)

Remember me from the DMP support thread?

Weird you should come back at this mo, I'm getting advice off the wonderful(don't tell him ha ha) N-I-D on his other thread as we speak.

Good to see you back hope all is ok.:jDMP Support Thread Member 238DMP started October 20080 -

Good evening everyone

I've been reading through the forum, some of it's quite heavy going and I'm getting confused about a few things.

I am currently, just about, managing to make the minimum payments on my credit cards, of which I have 3 - RBS, Barclaycard and MBNA, each with approx £9k on them. All were signed pre2007, I am currently trying to reclaim PPI on the RBS card.

Ideally, I would like to clear the debt with no effect on my credit rating, realistically though, I'll probably just about manage to make minimum payments and the debt will go on for what seems like ever, or I'll end up missing payments on some cards.

Would there be any benefit in me asking for the CCA for the accounts, and trying to establish if they were enforceable? If they couldn't provide the CCA or it was unenforceable, would I be in a position to negotiate a reduced settlement on the account, or interest freeze or anything?

I recently had a phone call from a company offering to try and get my debt wiped on a no win no fee basis, with a 25% commission on a successful claim. I chased them, but is getting debt wiped a realistic outcome?

Sorry for so many questions, but I'm all over the place just now! Been considering DMP's, Trust Deeds etc

Thanks

Dave0 -

Well worth requesting the CCA if only to have a bargaining position when you find out the debt is unenforceable.

You may even get this sort of reply!

"At the moment we are unable to provide a copy of the original agreement or the signed application form." :j

Puts you firmly in control for whatever you may want to do next.Good evening everyone

I've been reading through the forum, some of it's quite heavy going and I'm getting confused about a few things.

I am currently, just about, managing to make the minimum payments on my credit cards, of which I have 3 - RBS, Barclaycard and MBNA, each with approx £9k on them. All were signed pre2007, I am currently trying to reclaim PPI on the RBS card.

Ideally, I would like to clear the debt with no effect on my credit rating, realistically though, I'll probably just about manage to make minimum payments and the debt will go on for what seems like ever, or I'll end up missing payments on some cards.

Would there be any benefit in me asking for the CCA for the accounts, and trying to establish if they were enforceable? If they couldn't provide the CCA or it was unenforceable, would I be in a position to negotiate a reduced settlement on the account, or interest freeze or anything?

I recently had a phone call from a company offering to try and get my debt wiped on a no win no fee basis, with a 25% commission on a successful claim. I chased them, but is getting debt wiped a realistic outcome?

Sorry for so many questions, but I'm all over the place just now! Been considering DMP's, Trust Deeds etc

Thanks

Dave0 -

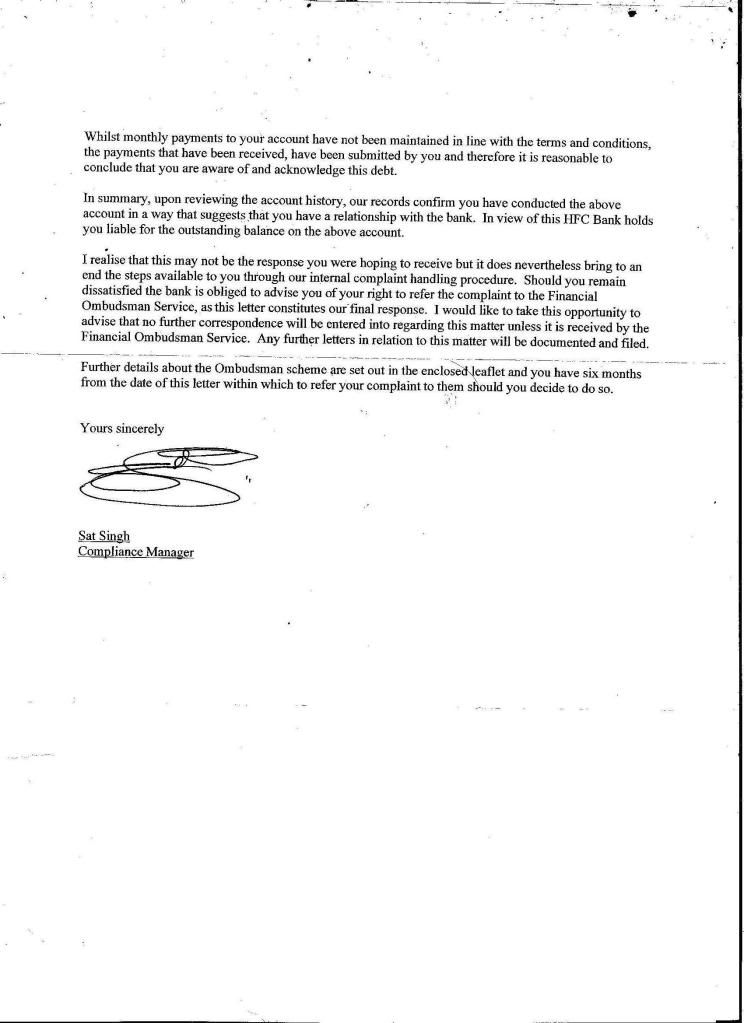

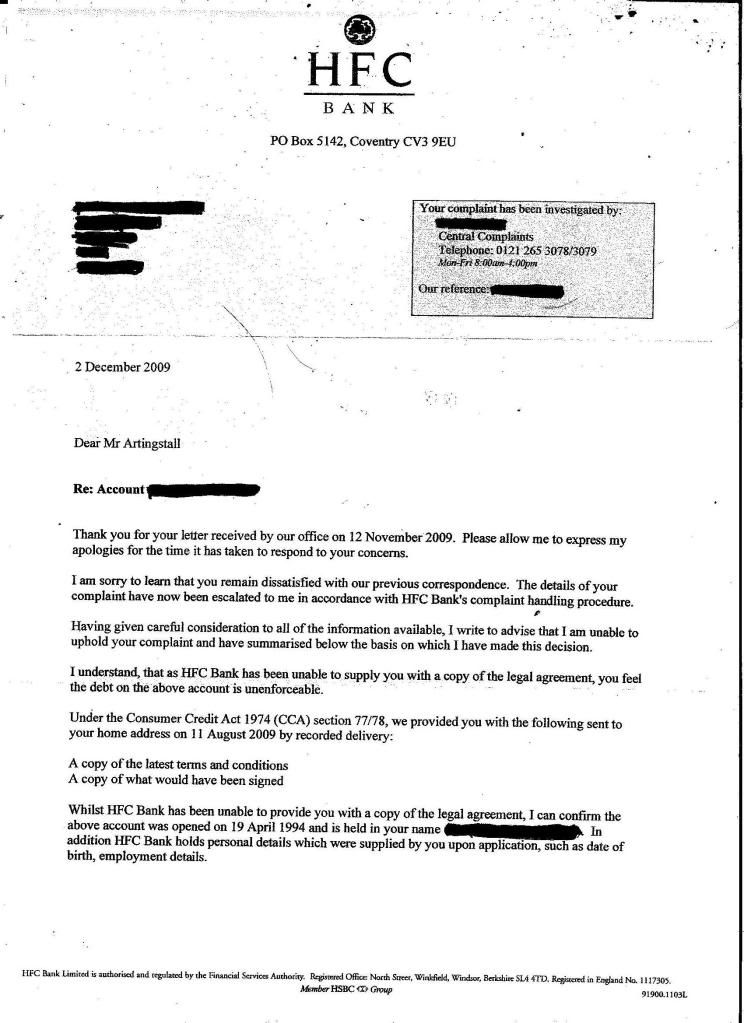

I have just recieved a letter from HFC bank telling me that they do not accept my account going into dispute if anyone has advice as to what I do next it would be appreciated they have not provided a cca at all and have basically said they do not have one I am in arrears with this account and have already offered them a full and final settlement which they have refused. http://i448.photobucket.com/albums/q...esponse001.jpg

http://i448.photobucket.com/albums/q...response02.jpg

these are the links to the letter that hfc bank sent me thanks in advance for any advice.Make £5 a day in May total so far £20 -

badgerbread wrote: »I have just recieved a letter from HFC bank telling me that they do not accept my account going into dispute if anyone has advice as to what I do next it would be appreciated they have not provided a cca at all and have basically said they do not have one I am in arrears with this account and have already offered them a full and final settlement which they have refused. http://i448.photobucket.com/albums/q...esponse001.jpg

http://i448.photobucket.com/albums/q...response02.jpg

these are the links to the letter that hfc bank sent me thanks in advance for any advice.

Hi bb - First of all, you should edit out your name from the HFC letter.

That said, their letter is little more than an admission that they have, in fact, failed to comply with their legal obligations under the terms of the Act. They state that they have provided you with:"A copy of the latest terms and conditions"

"A copy of what would have been signed"

Under the terms of the Consumer Credit Act, they should have provided you with a true and compliant copy of the original executed agreement. The 'latest terms and conditions' are, to this extent, totally irrelevant. The 'copy of what would have been signed' may or may not constitute a true copy of the original signed agreement - I don't know - as they are not legally obliged to send you a signed copy of the agreement.

However, the fact that they acknowledge, in their letter, that they are unable to provide you with a 'copy of the legal agreement' (they do appear to use a strange form of terminology) would indicate, to me, that none exists.

If this case were brought to Court, the court could insist that they provide the original signed agreement, without which the agreement would be unenforceable.

Did you send them the 12+2 day letter to inform them that they are 'In Default'? If not, do it now.I am NOT, nor do I profess to be, a Qualified Debt Adviser. I have made MANY mistakes and have OFTEN been the unwitting victim of the the shamefull tactics of the Financial Industry.

If any of my experiences, or the knowledge that I have gained from those experiences, can help anyone who finds themselves in similar circumstances, then my experiences have not been in vain.

HMRC Bankruptcy Statistic - 26th October 2006 - 23rd April 2007 BCSC Member No. 7

DFW Nerd # 166 PROUD TO BE DEALING WITH MY DEBTS0 -

I've seen it all now, This "Bank professional" admits they do not have a legal document AND yet still insists its enforceable. I've said it before, and I'll say it again..are bank workers EVER capable of learning?badgerbread wrote: »I have just recieved a letter from HFC bank telling me that they do not accept my account going into dispute if anyone has advice as to what I do next it would be appreciated they have not provided a cca at all and have basically said they do not have one I am in arrears with this account and have already offered them a full and final settlement which they have refused. http://i448.photobucket.com/albums/q...esponse001.jpg

http://i448.photobucket.com/albums/q...response02.jpg

these are the links to the letter that hfc bank sent me thanks in advance for any advice.0

{kind=link}

{kind=link}

{kind=link}

{kind=link}

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards