We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Applying for Probate

I’m hoping someone here will be able to help me understand a few things about applying for probate on behalf of my Dad.

I’ll try to be as succinct as possible but this may end up being a bit long winded.

After my mum passed my dad went to the bank to arrange for the money that she had in various accounts to be transferred to him. The bank asked to see her will before they could do that and so my dad in going back to the will writers discovered that they were no longer in business but his will was still on file with another company (long story but lots of bs). Anyway he managed to get the will but before he was able to take it to the bank they contacted him to say they didn’t need to see the will as he was under their threshold for probate and so transferred the money.

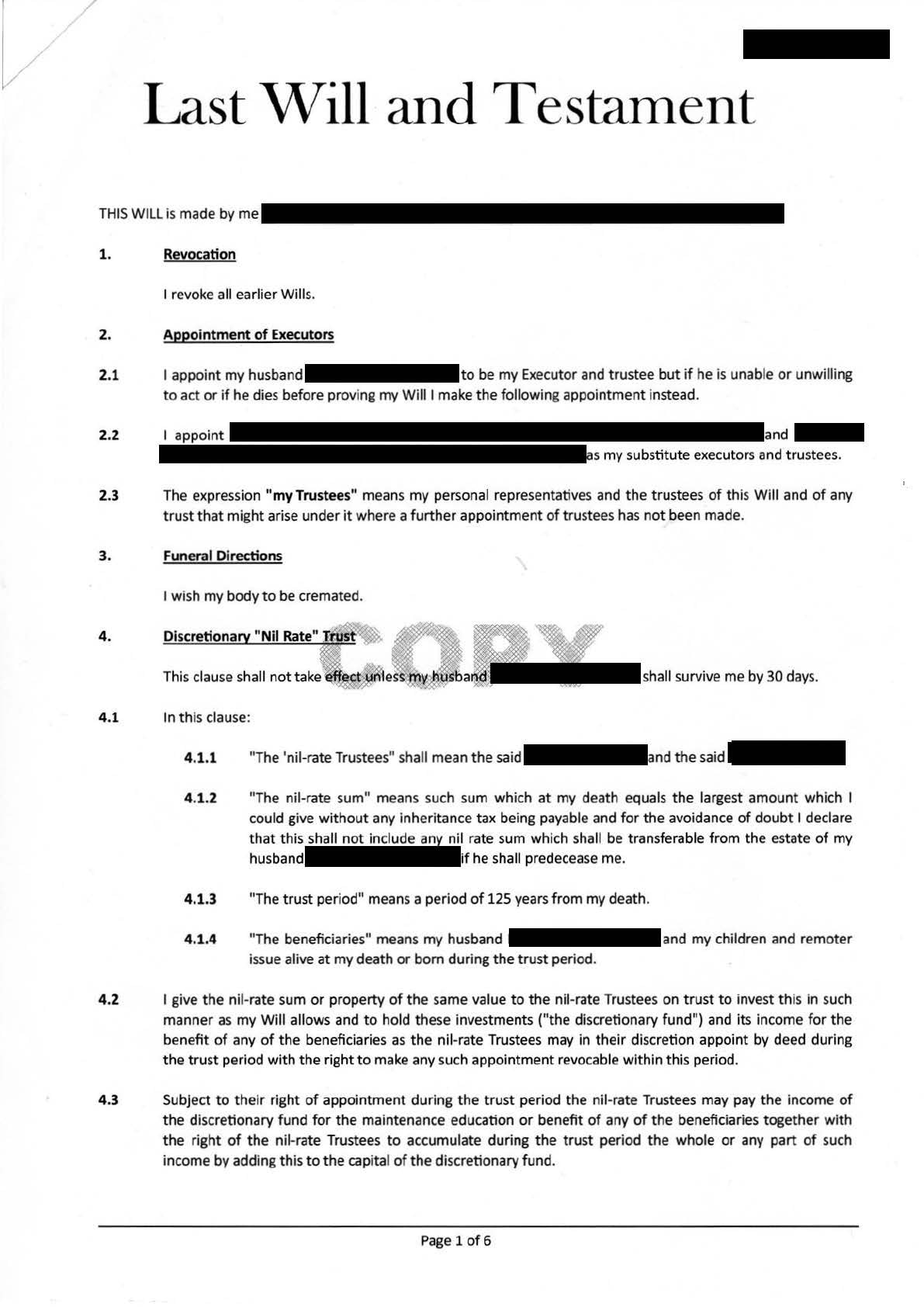

He then decided to get his will changed and sought advice from a solicitor who told him that it was all a bit of a mess because there was a Life Interest Trust and a Discretionary Trust involved. Neither of which anyone in the family knew about. My parents naively went along with the will writers suggestions without fully understanding what they were paying for and so were likely sold products that they didn’t need.

Myself and my wife are named as trustees and my dad is the executor of the estate.

I’ve checked the deeds to the house and my parents are named as tenants in common with a Form A Restriction. I can’t see mention of a percentage split so assuming it would be 50/50.

There is no IHT to pay as the total value of the estate is well under the allowance.

The solicitors want to charge my dad £1500 to obtain the grant of probate on his behalf but he’s already spent £400 just to get to the point where they’ve said they’ll do it and I’m reluctant to let my dad spend more money if it’s something I can do for him. Particularly as they wanted to charge him £350 + VAT to check if I had been made power of attorney which I ended up doing myself and it only took me 5 minutes to fill out the OPG100 form. I’m not power of attorney even though that was something else they had paid to be done by the will writer.

I’ve downloaded the Probate postal form just so I could look through everything and as far as I can see I feel relatively confident that I would be able to do it. I guess what I’m looking for by posting here is to find out if maybe there is something that I may not have taken into account or if the solicitors are correct and that due to the trusts it is a bit of a mess and so not as straight forward as I’m thinking.

Really hope someone can help and appreciate your time for getting this far.

Comments

-

When was the will written?

Immediate Post Death Interest Trusts are common as a means of ring-fencing a percentage of the value of the property for the benefit of children against remarriage, care fees etc. The terms are written into the will. They do now need to be declared to HMRC within 2 years of death.

If you've have not made a mistake, you've made nothing1 -

Thanks for replying @RAS The will was written in 2016. From what I'd read it's my understanding that the trusts are exempt from being registered for two years. Is that what you mean or am I getting confused?

I was planning to post a separate thread about the trusts and my responsibility with regard to the them and for now just concentrate on the probate side of things but maybe I need to be dealing with them as well?

0 -

I'd be happier if @poseidon1 could comment on the trusts. Some of these have implications for IHT now or later.

If you've have not made a mistake, you've made nothing1 -

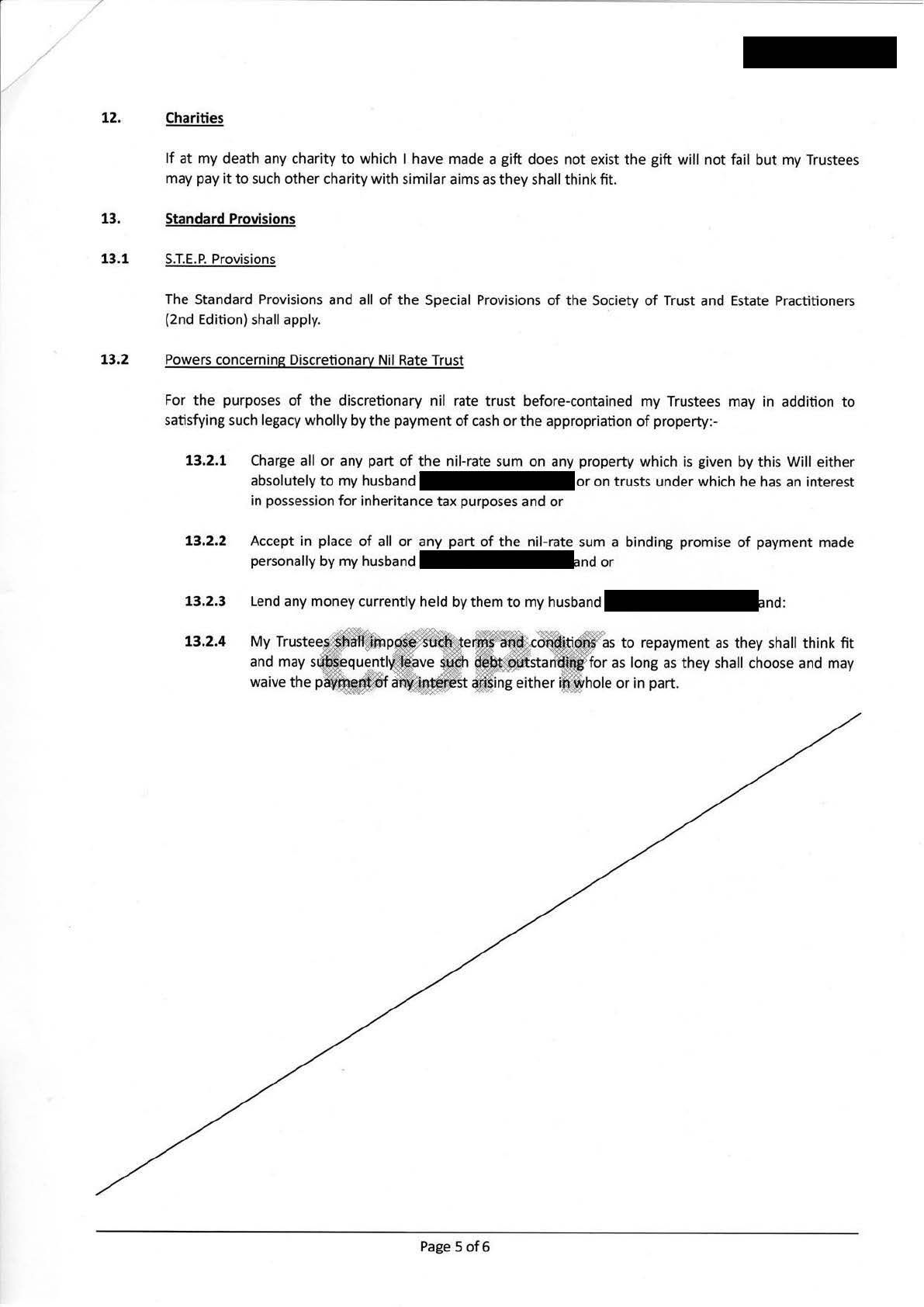

From I read, I have to confess to being truly appalled at what has been done here. Its probably the worse Will I have seen on this forum by way of unjustifiable complexities involving two different forms of trusts. If executed in 2016 as stated , then clearly a cynically prepared document designed to benefit the will writing firm to the detriment of the family.

If your father's will was a mirror image of this , it should be destroyed forthwith and replaced with a far simpler more straightforward document.

You say you are proposing to DIY obtaining the grant of probate to save legal costs, but I fear you do not understand what your mother's will has purported to do, and how that should be interpreted for probate purposes.

First, a nil rate band discretionary trust was established ( clause 4) which would have covered all her cash and non property investments ( eg, stocks and shares, ISAs etc) up to a value of £325,000.

Accordingly, the cash accounts your father assumed were his to transfer to his own account were not.

After allowing for estate expenses that cash forms part of the discretionary trust which unfortunately uses up part of your mother's nil rate band for IHT purposes. Even though your father is one of the beneficiaries of that trust it is not an IHT exempt gift to him. That needs to be properly reflected when apply for the Grant.

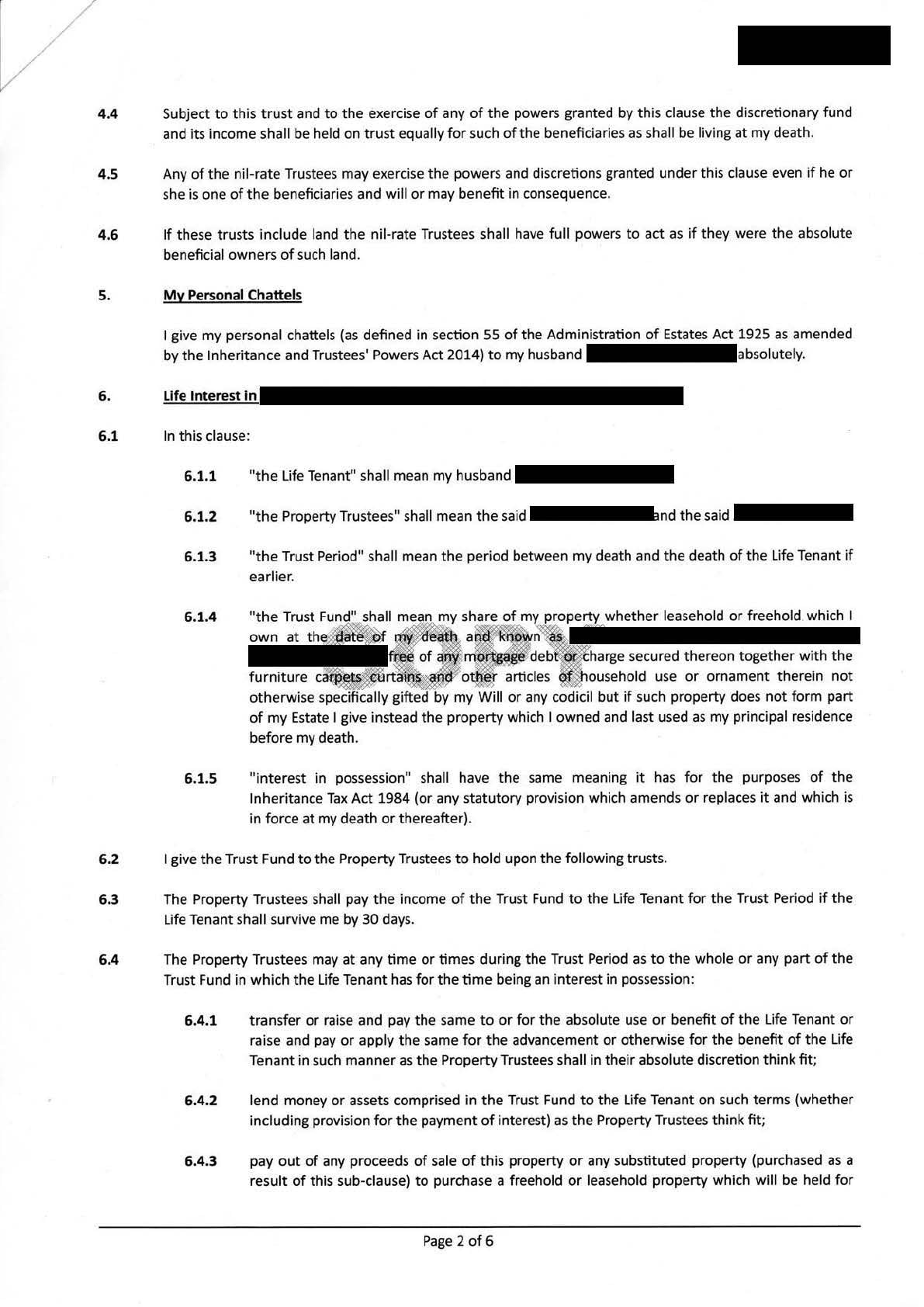

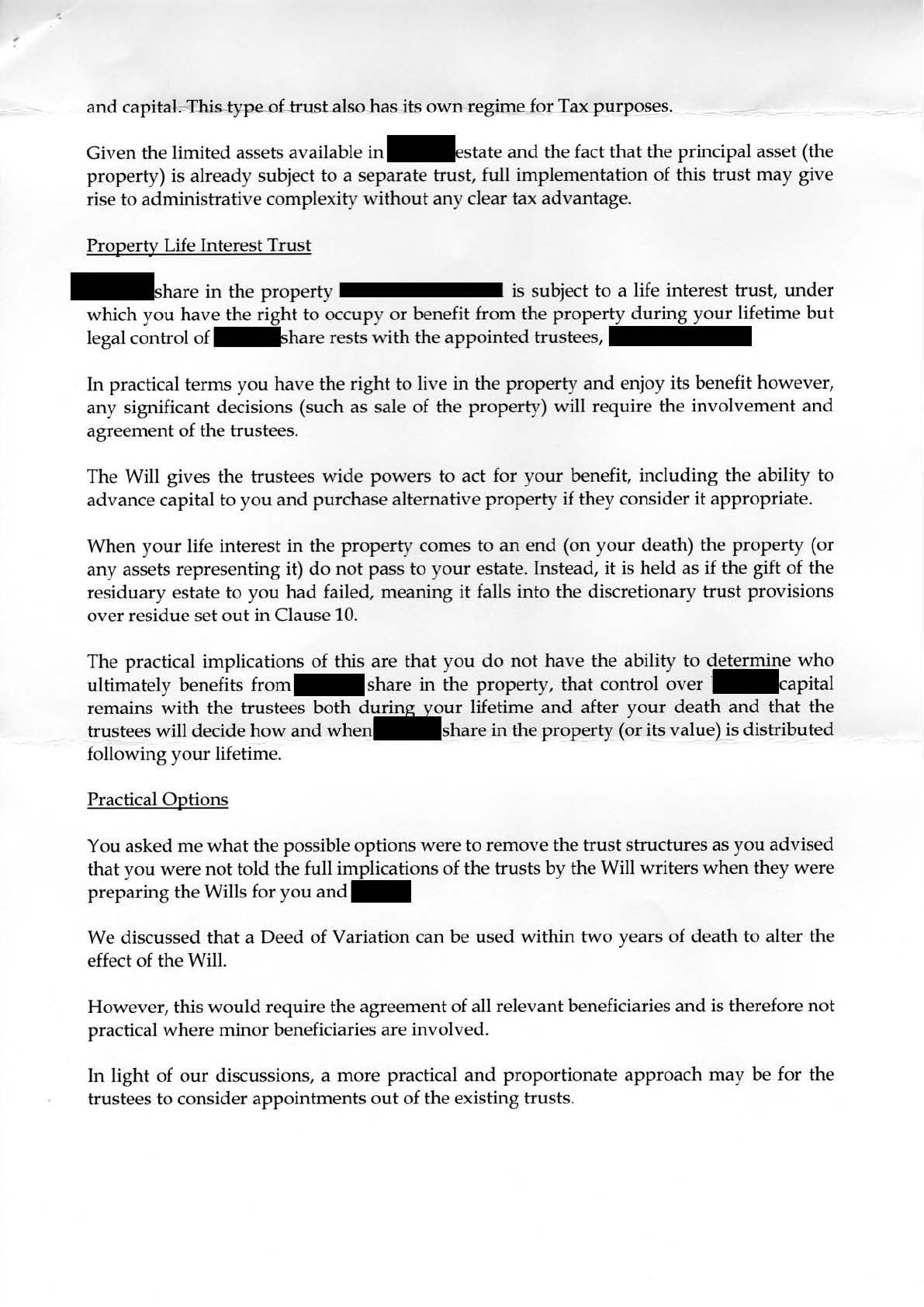

Turning to the life interest trust for your father of your mother's half share of the property, this would be considered an IHT exempt gift to him. However it is what happens to that property trust on his death which especially appalls me.

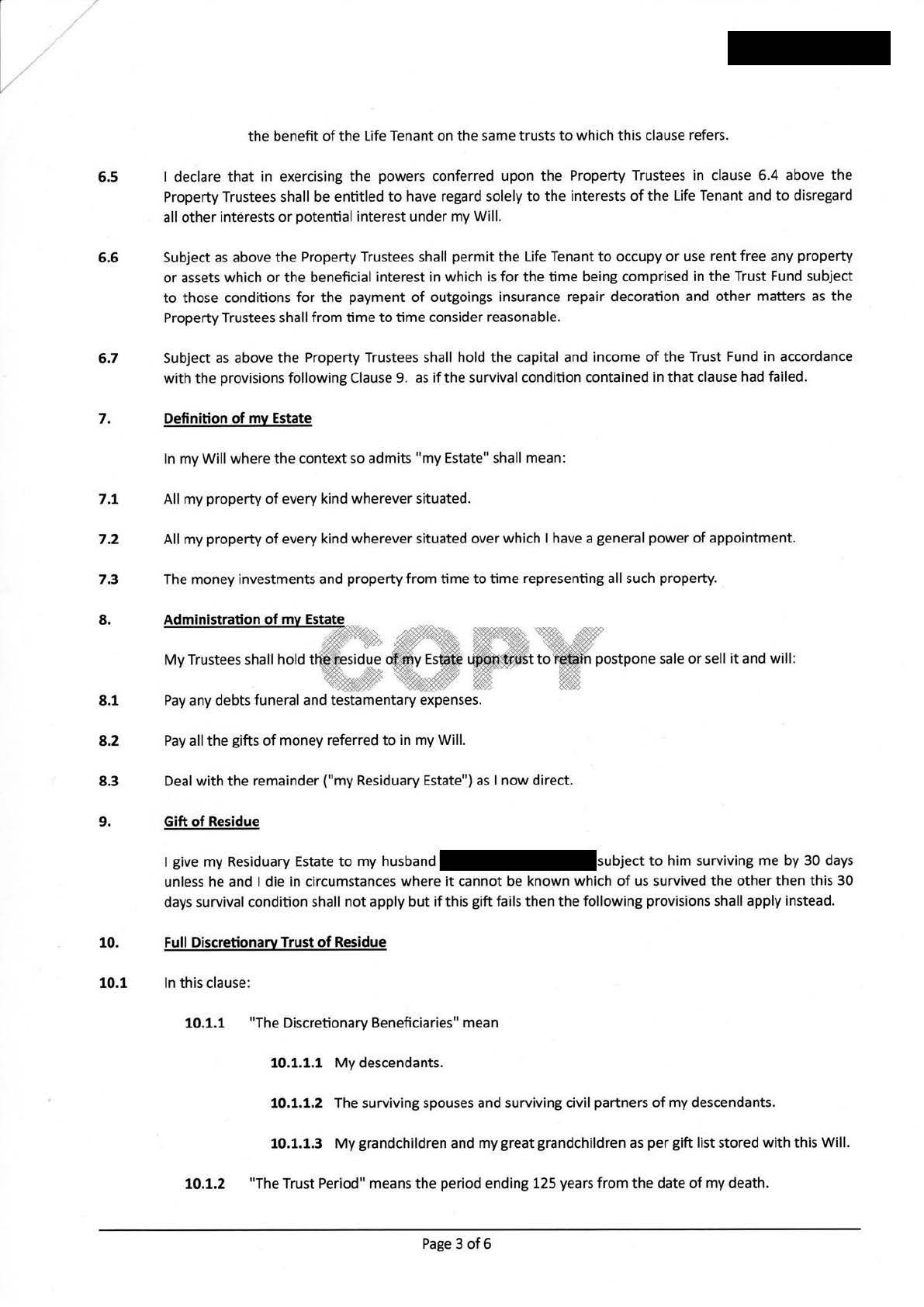

Ordinarily with these types of life interest trusts ( now known as IPDI trusts) on death of the surviving parent the property would revert to the absolute ownership of the children ( the remainderman). This would preserve the Transferable residence nil rate band ( TRNRB) ( £175k) of your mother, to use along side your father's residence nil rate band on his death. However, your mother's will inexplicably purports to resettle the life interest trust fund onto a residuary discretionary trust for her descendants, their spouses, remoter issue etc. As result this subsequent trust negates her £175k TRNRB - a disaster.

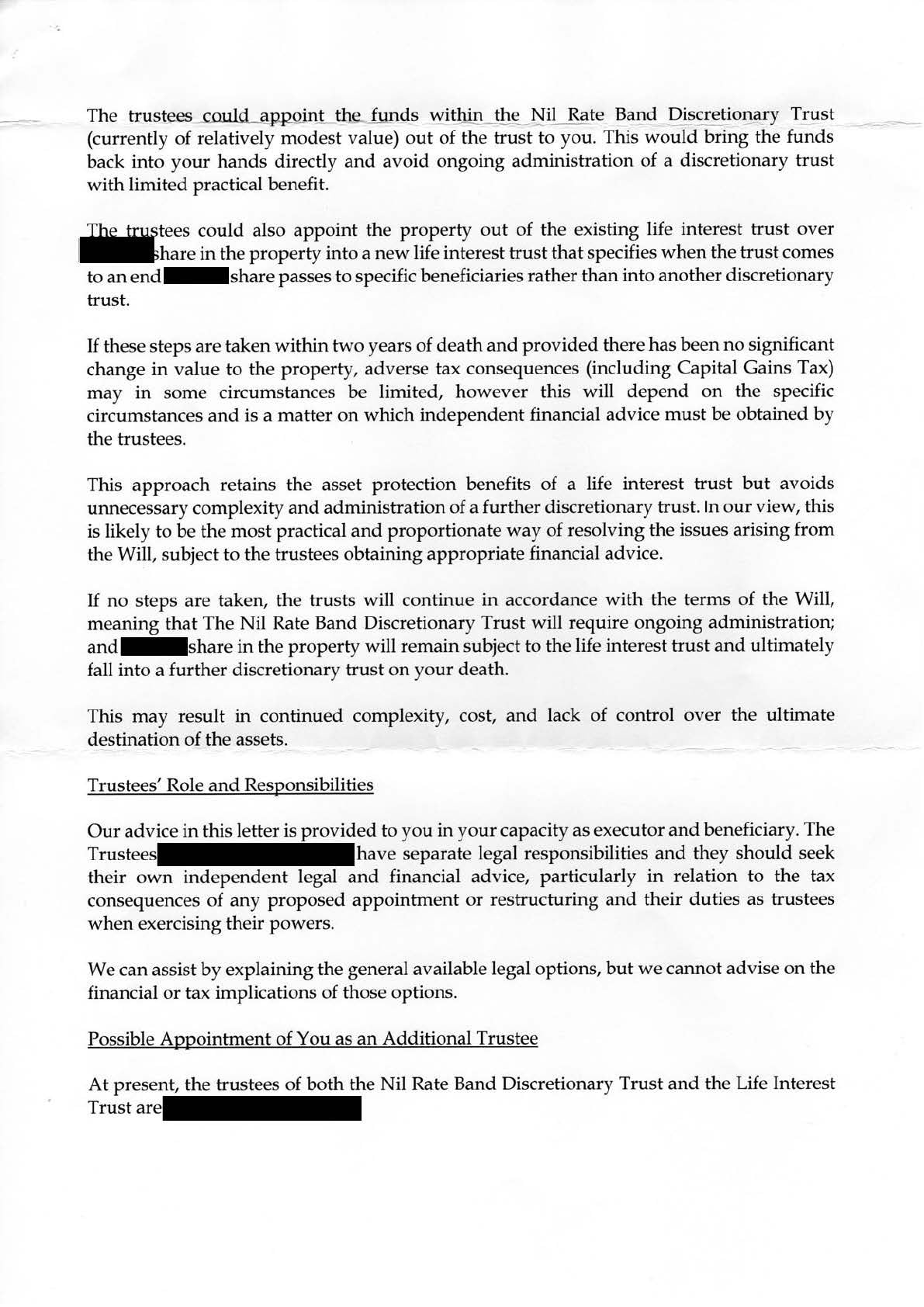

The upshot of the above, is that prior to obtaining probate the most urgent task is to devise a strategy to try and eliminate all the trusts created by your mother's will with the objective of reinstating her transferable nil rate bands for use when your father eventually passes.

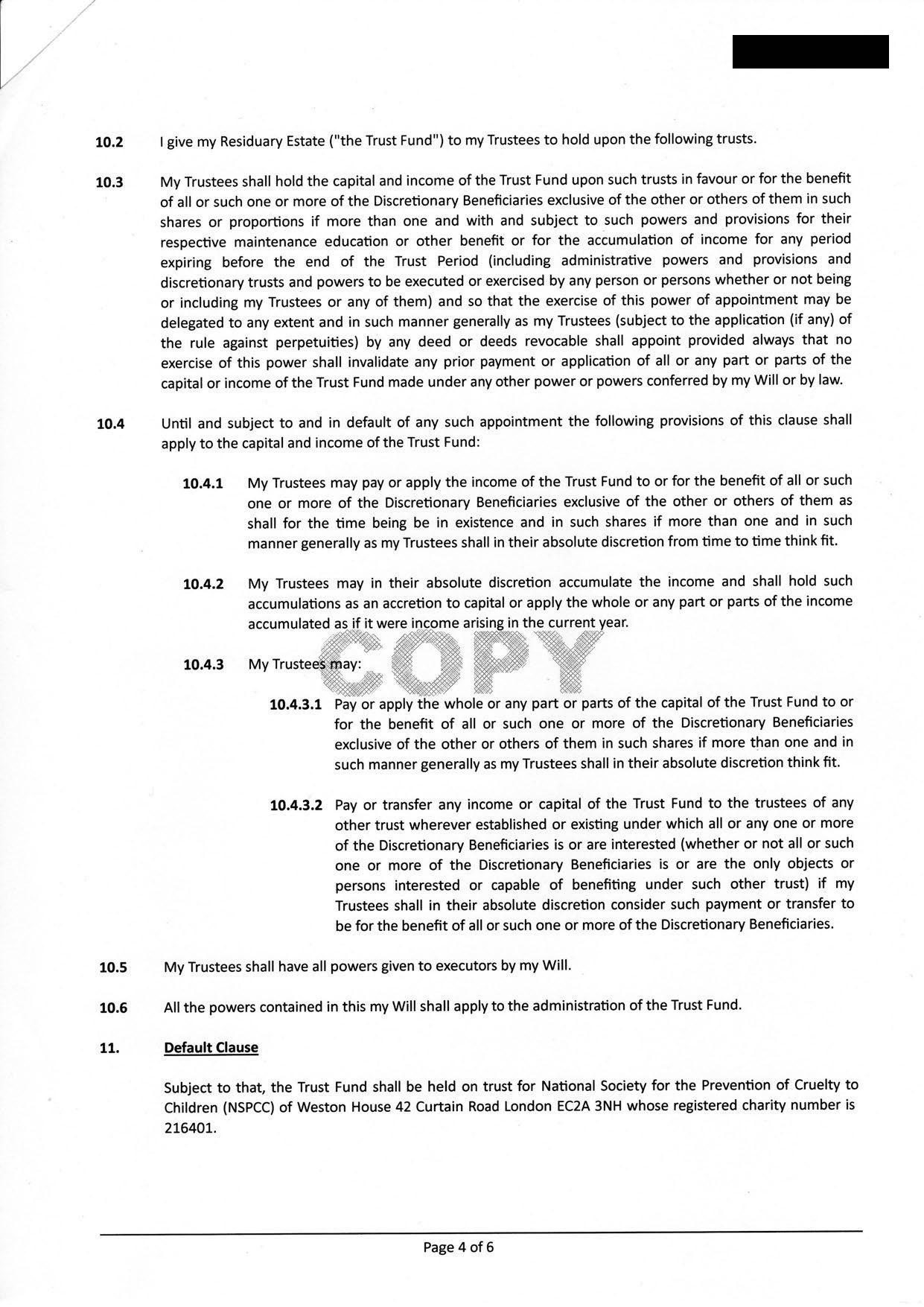

However this will not be easy, since utilising a Deed of Variation executed by all the adult beneficiaries is hampered by the fact that the discretionary trusts beneficial class include 'remoter issue' ie unborn babies and minors not to mention sundry spouses.

Accordingly the complexities and eventual IHT impact when your father eventually passes, are such that you have no other option than to seek the services of a highly experienced STEP qualified solicitor who can advise on options ( if any) available to the family to :

- Try and restore the part of your mother's nil rate band used by the clause 4 discretionary trust.

- Try and eliminate or amend the life interest trust for your father to restore the availability of your mother's transferable residence nil rate band.

I suspect the solicitor who gave you the £1500 quote may not be right for this task, especially if they did not relate to you any of the glaring concerns identfied above.

2 -

@RAS ok thanks. I had thought that IHT wasn't likely as the estates value isn't even half of the £325,000 allowance but yes if @poseidon1 was able to shed some light on that I'd be really grateful. Thank you

0 -

thanks @poseidon1

ah!

The problem with the solicitor is that they wouldn't talk to me because of a conflict of interest (being a trustee of the will) and so my dad (and my brother) went to meet them. As such I don't know the full details of what they said but they did come away from the meeting knowing that it was all a bit of a mess and that the will writing company had done a terrible job and clearly ripped them off. To which my dad obviously feels terrible.

And yes my dads will is a carbon copy of my mums.

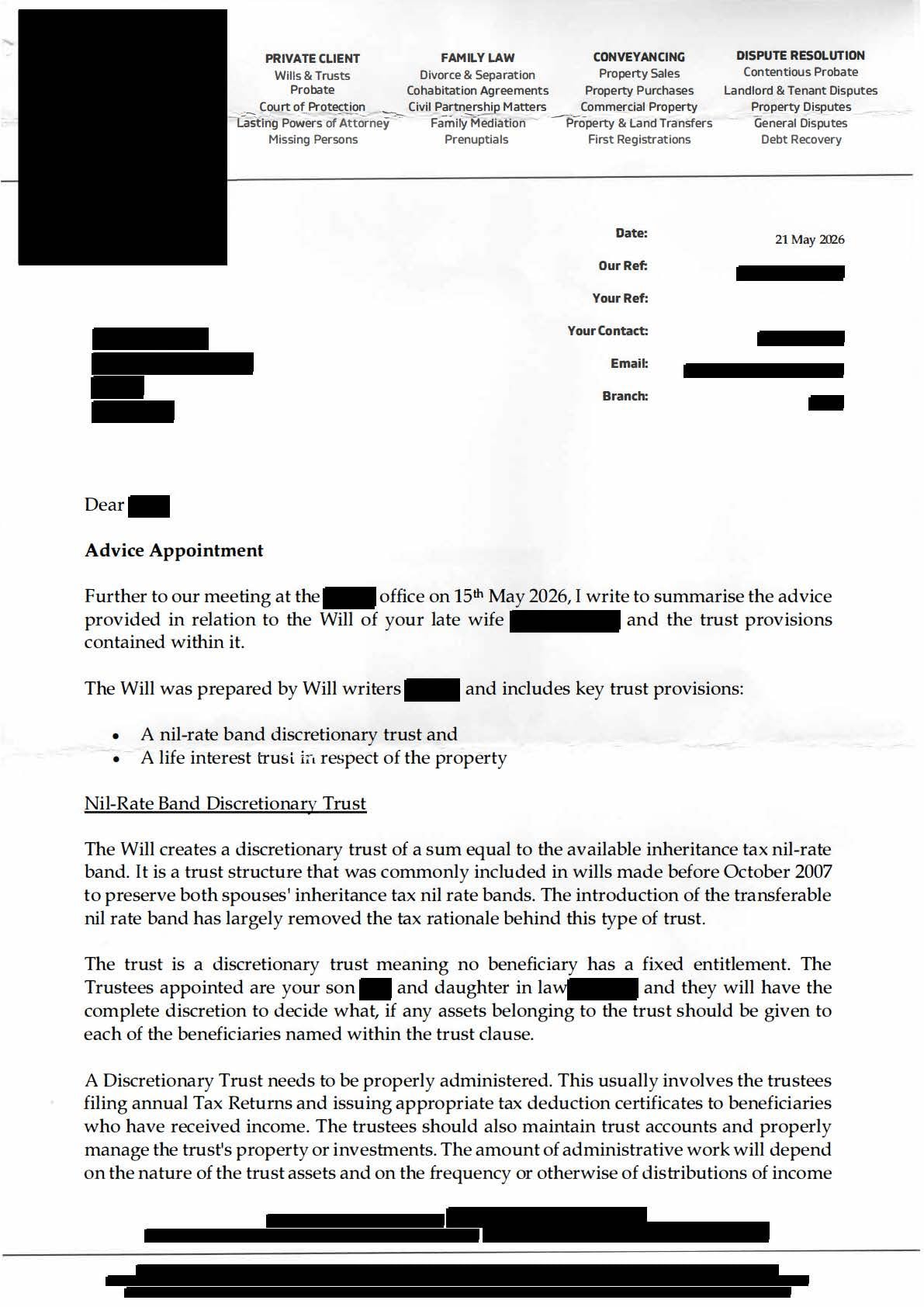

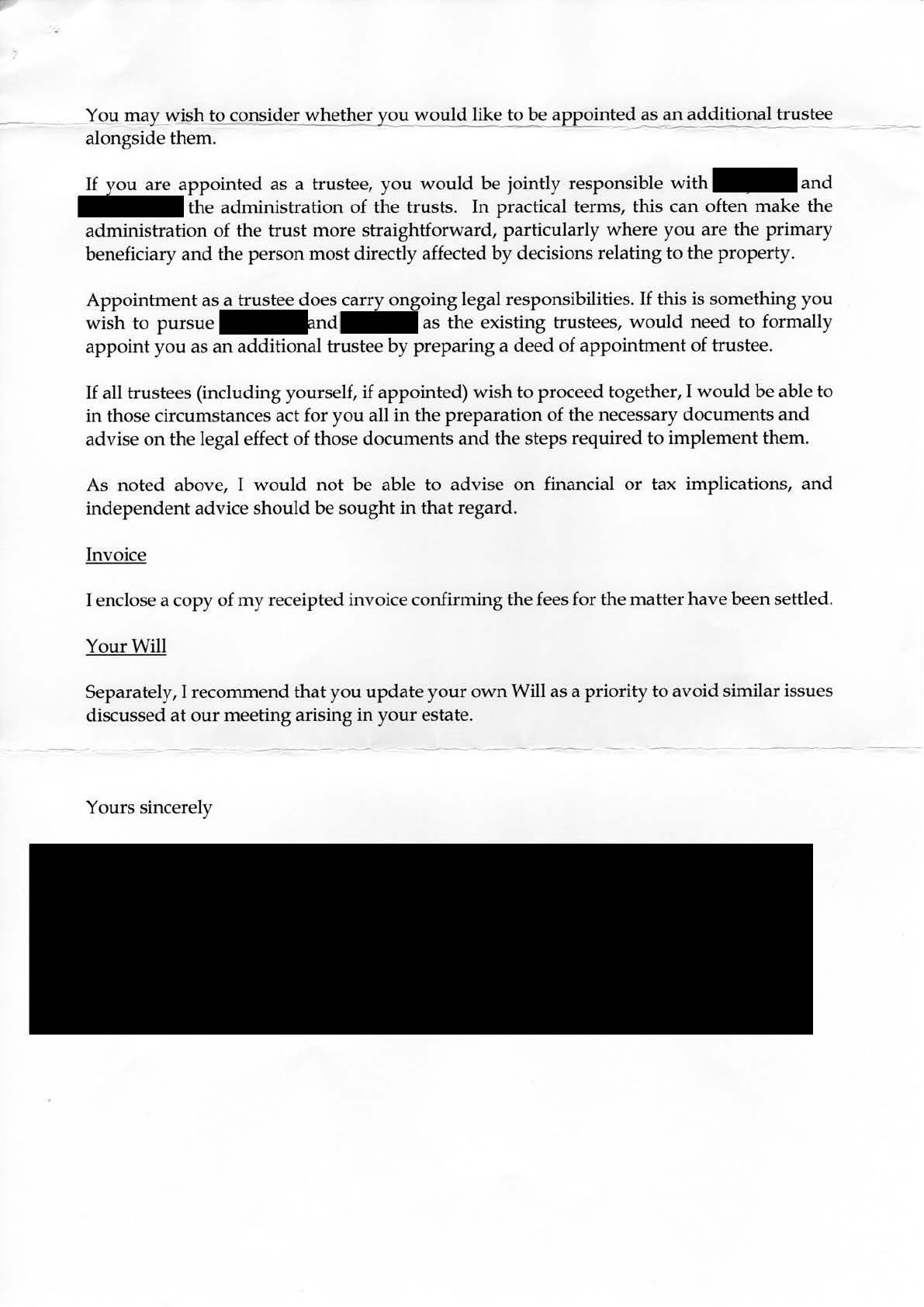

This is the letter my dad received after meeting with the solicitor.

0

0 -

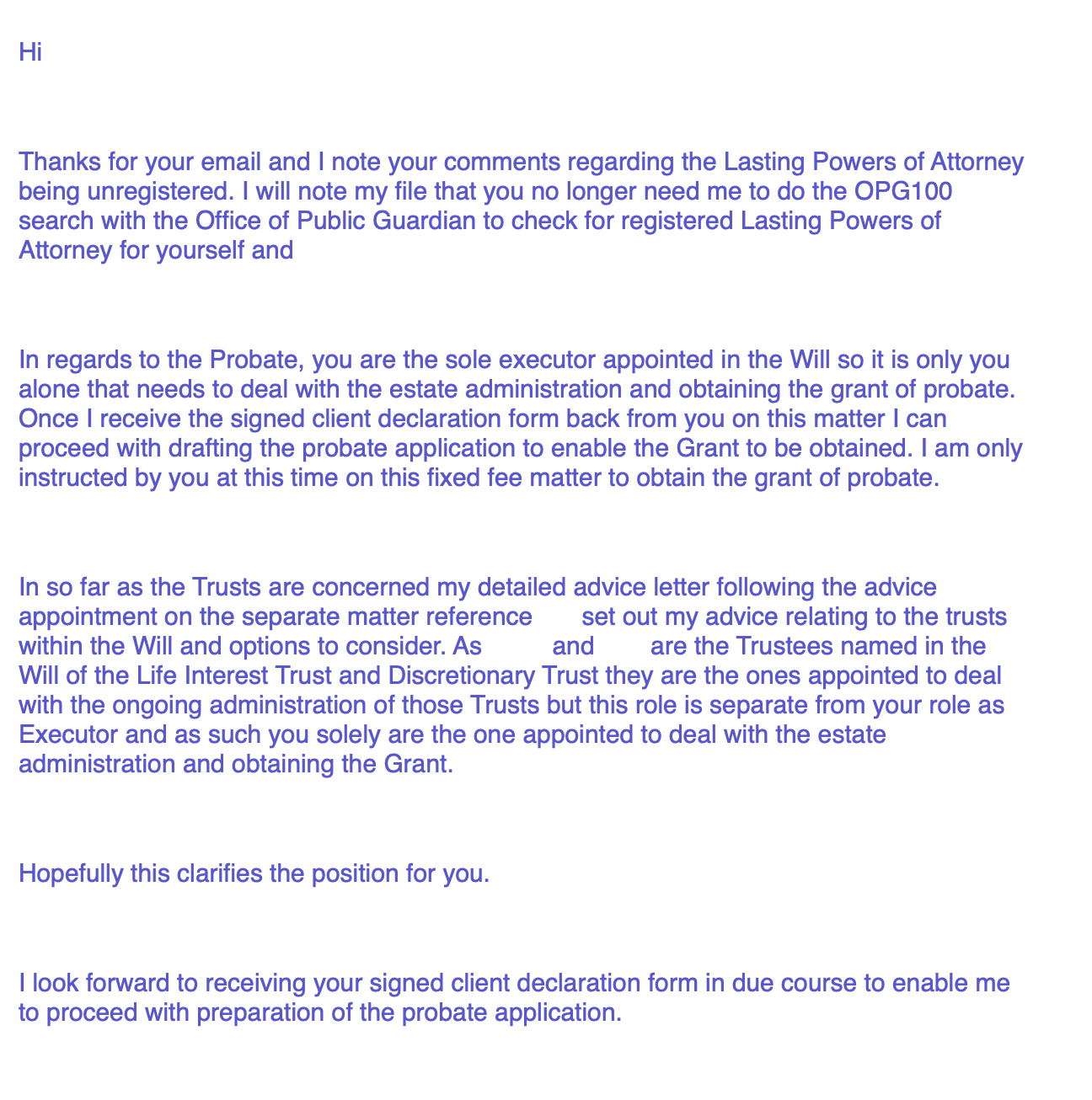

@poseidon1 also, I asked my dad to email the solicitors for clarification of what they would be doing and this is the response which is why I thought that if all they were doing was a grant of probate (i realise that is possibly much more involved than I first estimated) that I could do it for him.

0

0 -

This must be the best example seen on here of why you should use solicitors to make a will not unregulated will writers. It’s a real shame the will could actually be tracked down intestacy would have been a far better outcome.

1 -

Having seen the solicitors' very detailed response, it did indeed flag the issues I raised albeit in a far more moderated tone than I chose to use.

In my view he has clearly demonstrated being able to handle the dismantling of the discretionary trust by a simple deed appointing all the cash to your father, and varying the life interest trust to give it qualifying IPDI trust status going forward. All actions to be completed well inside the 2 year post death period for capital appointments and trust variations.

The solicitor has suggested you get independent advice on the course of action he has laid out, but frankly he has covered all the pertinent issues which concerned me, and I believe you can confidently use him to implement the post probate deed drafting excercise to deal with both trusts as advised.

I am also confident he can set you on the correct track for the future ( simple) administration of the life interest trust for your father as long as he remains able to reside there during his lifetime. Things get a little more complicated if he needs to go into care, and investing his trust fundsr to produce income becomes necessary, but cross that bridge when/if you come to it. I am sure the solicitor if still available at that future point can advise you accordingly.

In the meantime, if you still wish to proceed with the probate application yourself I would still get the solicitor to give it the once over before you submit, since the nil rate band discretionary trust aspect may trip you up.

If the £400 your father spent was for the solicitor meeting and subsequent detailed written advice, then it was money well spent and your father could do worse than use that solicitor for his new replacement will.

Yet another example of how these will writing firms are an unmitigated menace to the general public.

4 -

@poseidon1 thanks again for your help. Just so I'm sure I understand correctly. Applying for grant of probate myself is do-able and that once that is done I should go back to the solicitor in order to dismantle the discretionary trust and to alter the life interest trust and as long as this is done within two years should be something easy enough for them to do?

Regarding probate and coming unstuck due to the nil rate band discretionary trust, my parents are far from wealthy and so the value of the estate even if you include my dads half would be well under the threshold for IHT. So am I right in thinking that this wouldn't be an issue or am I being naive in thinking that?

Thanks again, I really do appreciate you taking the time to reply.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.9K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.7K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.7K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards