We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Retirement Living Standards

Comments

-

Don't wait until just before retirement it's a really useful metric for budgeting and saving. It was early in my investing for financial independence that I kept a couple of years of detailed expenditure. Easy to see what spending become discretionary and where savings or deferred gratification can be applied to fill the retirement pots. Finger in the air 4% SWR gave me a capital number to work with.

1 -

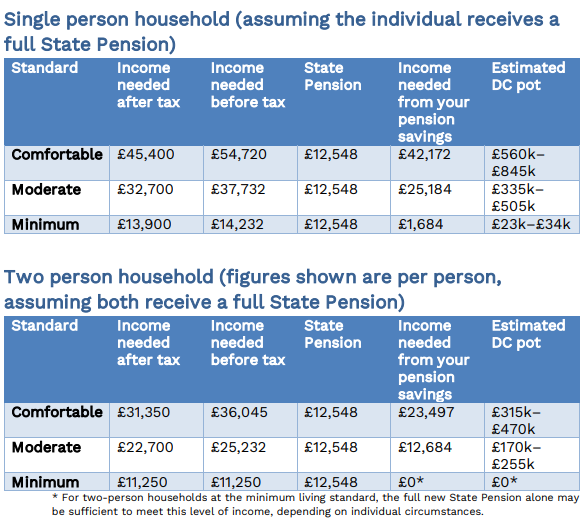

The link I posted estimates that a Moderate couple would need a DC POT of about £450k ( presumably minus any significant other savings or investments), after taking two full state pensions into account.

3 -

Previous years the estimated pot sizes were considerably on the low side, perhaps with the recovery in annuity rates they are now more realistic?

I think....1 -

As always I'm a sceptic and you only have to look at the sponsors to see why. Pensions companies have a vested interest in getting people to invest in pensions. So to me the way the data is collected and processed is not representative of reality.

What would you like in retirement is entirely different to how would you describe your retirement. People may say what they think is a comfortable lifestyle but that most likely does not correlate with what those in retirement say is a comfortable lifestyle.

Their holiday figures are I think a good example of this. If I went on a two week half board holiday I cannot imagine me and Mrs O spending £230 a day between us on top of the cost of the holiday. But if you asked me when I was younger I might say I'd like to be able to do x y and z.

To be blunt, the figures are a poorly researched wishlist and not reflective of what many in retirement consider. As others have said, look at your own wants and needs. For me and Mrs O, we get a lot more out of life in our plans on a lot less than the comfortable figure.

8 -

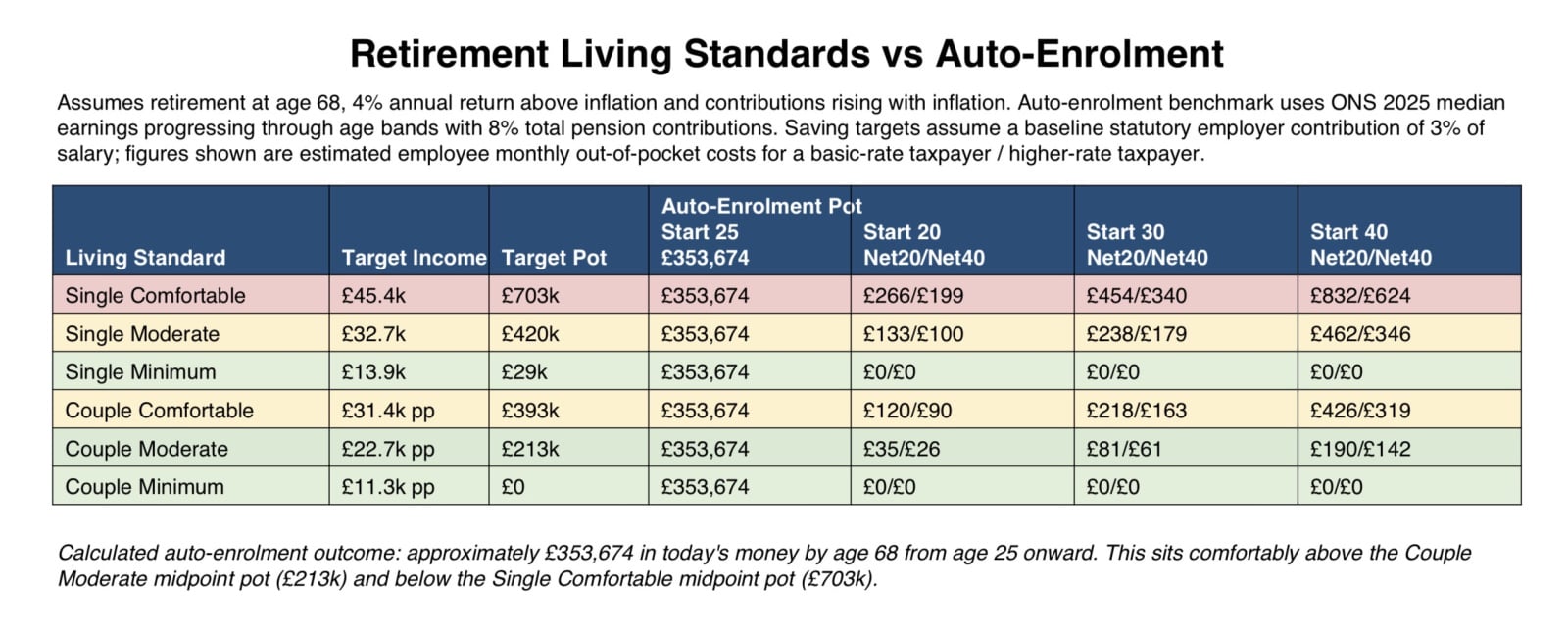

ah - that took me a second to decode. so its assuming this is retiring at normal state pension age, and the couple values are per person income and savings needs?

almost not bad. Although the absolute amount feels a little high and I’d trade some of that for retiring earlier - thats obviously a subjective thing.

What would be nice would be to extend that further to get a full end to end picture.

min/moderate/comfortable - cost per person at normal retirement age - how much in your pot to service that….and how much to save per month/year to achieve that with conservative growth starting at 20/30/40.

might have a play if I’m bored but this kind of data is most likely used by slightly younger - if you’re in your 50s you should already have a grasp on your budget and have a good idea of your retirement budget too. you use a rule of thumb if you’re further away or its more abstract. so give them the full info

1 -

I read that link that the Moderate Couple would need a DC POT of £450k EACH, not just a total pot of £450k.

Is your comment relating to "Moderate" or "Comfotable"?

Anyway, from the link you posted:

If a Comfortable Single Household requires income of £45.4k and a DC POT around £850k, then the line for Comfortable Two Person Household must be income needed £31.3k each and, hence the required DC pot is £450k each.

It makes no sense to think that a Moderate Single requires £45k and £800k pot but a Moderate Couple only need £31k and £450k pot between them.

I do think the table is poorly laid out but, only on the umpteenth reading did I notice the note in brackets "figures shown are per person"

1 -

Interesting that the estimates of DC pot requirements indicate a withdrawal rate between 5 - 7.5%…….at SP age, a withdrawal rate starting at 5% seems in the ballpark, but 7.5% might be pushing it a bit……

Also, the part where they say that "for a two-person household at the minimum living standard, the full NSP alone may be sufficient"…….that rather ignores the issue of what happens when one partner dies (and that partner's NSP dies with them)

2 -

using the target amounts in the living standards - per person targets. Taking the mid point of those totals and estimating how much you need to contribute starting at different ages. Figures are net impact to your salary for 20% and 40% not assuming salary sacrifice. Also assumes a simple 3% (minimum statutory) employer contribution. Statutory is assuming median earnings and adjusted for each age group 20s/30s/40s etc using ONS data. So reality might be a little lower at the start and higher later?

these are quite intersting I think. Couples clearly an easier lift - even the comfortable isn’t far off statutory if you keep that up you’re not a million miles away. Single you need to push a little even from the start. and as we mostly all start as singles that might be the simpler rule of thumb - aim for moderate initially which seems doable, and if you transition into a couple you should be fine.

0 -

Not really.

A couple require £11,250 each and that may be fully met by SP so zero DC pot is required.

When one of the couple deceases, the household becomes a Single Person Household on the other table requiring £13,900 and a DC pot of £34k

0 -

These reports always end up with overanalysis and comment about how all the figures are wrong, biased, I live on much less than that and I work etc etc.

However the figures are about living expectations in retirement. If you have always worked on minimum wage, but have lived on that income and you expect this to continue the tables give an idea of how much of a pot you need to continue to do so.

Similarly if a couple have had well paid jobs, bought a home, have two cars, have weekends away, holidays abroad, decent meals out, a busy social life and they expect that to continue they need more.

From my experience the figures aren't miles out,0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.7K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.5K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards