We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Pension advice

I got a pay rise in April and want to start putting the extra amount I get a month into the pension I am paying into at work, if I add extra money in manually will I still get tax relief on this money or do I need to get my employer increase the amount I pay in via my wage to get the tax relief?

Many Thanks for any help

Comments

-

Ultimately you get the same tax relief either way, but it would be easier for you to have it deducted from your wages and paid that way. That would certainly be the case if your employer offers salary sacrifice, because you'd then get an extra saving on NI. Have a chat with your employer to check what's possible from their perspective and take it from there.

Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0 -

Thankyou so much I am not sure if it is a salary sacrifice pension as I’m very naive when it comes to pensions I am currently on my 3rd pension scheme since being in the same employment as it started off council run then got tendered out to a charity then to another last October. The charity that is currently my employer pays in an amount slightly higher than me. When we got the payrise it shows the amount that they pay in has gone up slightly as has the amount that I do has. Since I haven’t missed the extra money I thought I’d put the extra in my pension. I will see tomorrow if they can up my contribution that comes for my wage.

many Thanks0 -

Thankyou so much I am not sure if it is a salary sacrifice pension as I’m very naive when it comes to pensions.

After you have contacted your employer, and hopefully sorted out the increased contributions, you may want to consider improving your knowledge about pensions. This would most likely bring some benefit for you as you get older. This website could be worth a look.

Pensions and retirement | Help with pensions and retirement | MoneyHelper

One mistake many people make is underestimating how much they need to contribute when working, for the pension to generate a decent income in retirement. Of course people have many other expenses and maybe on a low income, but the fact remains that contributions levels of 3% from employer and 5 % from employee ( which is very common) are too low.

3 -

Thankyou i appreciate that I will take a look, I’ve been looking at stuff a bit more recently since being enrolled in my 3rd work based pension scheme the others are now deferred, due to contracts being changed due to new company taking over. I have quite a bit of savings probably my annual income in cash ISAs and savings which has been saved over the years. It’s when I read in pensions that it’s in stocks and shares and it’s not guaranteed that you will get back what I put in that makes me feel that if it’s in savings I know it won’t go down.

I agree with what you are saying I’m not on a big salary and I don’t know whats round the corner as I could be made redundant at any point in the future as my work currently has a 3 year tender agreement with the council with a possibility of another 2 years so I don’t want to put too much out of my wage in a pension I can’t get at until I retire as I need to also be able to live comfortably now and have money to fall back on if the worst happened before I retire. Which is why I thought I’d top up my contribution in my wage with the difference from the pay rise as it’s extra that I didn’t have before and It wasn’t needed before so I won’t notice it. If I get tax relief anyway if I add extra not via my wage I will top up a bit extra when I feel I can.

0 -

It’s when I read in pensions that it’s in stocks and shares and it’s not guaranteed that you will get back what I put in that makes me feel that if it’s in savings I know it won’t go down.

The good thing about pensions is that they are long term. Over the long term, investments historically have gone up way more than the interest you get from cash savings. It would be a very very poor decision to leave a pension in cash long term.

Worth to have a look at this, especially the first graph that is shown.

1 -

I know a chap at work who refuses to put money into the company pension for the same reason as above. We use salary sacrifice, and the company pays in 10% as long as you put in 5% yourself, so he is literally missing out on £100k+ by the time he retires. He just can't get over the statement that you might get back less money than you pay in though.

I stayed at a campsite last year, where they seemed very keen to let me know that they weren't responsible for any losses from items taken from tents or cars etc. I can't say it made me feel very comfortable, so I asked the guy what sort of things people were taking, and he said no one has ever had anything stolen. They just have to have it in the terms and conditions for legal reasons.

Think first of your goal, then make it happen!3 -

A friend of mine has been working as a civil servant for over 20 years. He only started paying into the pension scheme about 8 years ago, due to his lack of "trust" in the scheme.

Another friend is in her 50s and has been a nurse her whole career. She never paid into the pension scheme. She could be retired by now, or at least a lot better off than she is.

My dad has never invested a penny in his life. He is currently 80 years old. Luckily he has a very good DB pension scheme which he did pay into, which covers all his financial needs. The cash he has is just a bonus.

I guess we all, or at least most of us, have similar anecdotes. There's definitely a skills gap in the UK, where many people are not getting investments to work for them. I doubt it's more pronounced here than other developed countries. The big difference being that here our government expects us to make the most of investments (e.g. the generous tax breaks on private pensions) whereas in other European countries investing is not treated so favourably.

2 -

It’s when I read in pensions that it’s in stocks and shares and it’s not guaranteed that you will get back what I put in that makes me feel that if it’s in savings I know it won’t go down.

Using cash savings actually increases risk compared to investing. You are replacing investment risk with cash, but you are increase in shortfall risk and inflation risk.

Usually, nervousness about the stock market is down to lack of knowledge and understanding. It's another risk that exists that is offen referred to as behavioural risk. I.e., you, the investor, can do things that are wrong because of your behaviour.

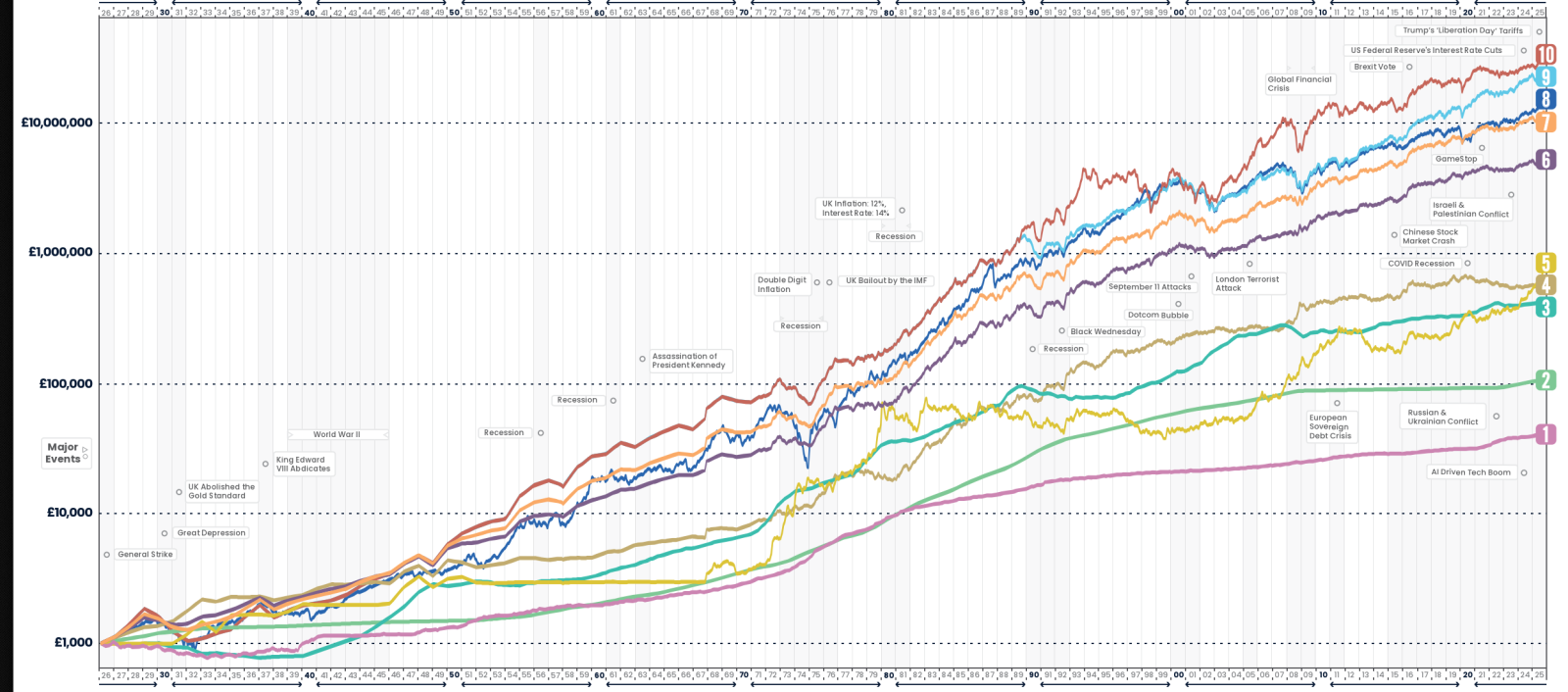

The following chart isn't going to work that well on a small screen. But the data isn't as important as the lines that show the different returns over the last hundred years. The one labelled 1 in purple is inflation. That is the one that is vital to exceed. The green one labelled 2 is Cash Savings. The gold-coloured one at 5 is unsurprisingly gold. The orange one at seven is where many pension default funds are it's made up of 60% global stock market with 10% emerging markets and 30% global bonds. The pale blue, number nine is 100% global stock market, excluding emerging markets.

So your behaviour is leaning you towards number two near the bottom. Whereas your head should be leading you towards the top end.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.5 -

Great idea , I used to do the same every year for increasing my Pension contributions , been retired for 18 months now, retired the weekend of my 60th.

0 -

Thankyou everybody for all your expert advice and has definitely got me thinking I’ve asked to increase my contribution but the person who does payroll is off until the 2nd of June when they start doing payroll to be paid on 15th so will see if they can do it, I think in regards to pension right now I don’t want to contribute too much out of my wage as I am not on a big salary so don’t want to leave myself short for living now, I’ve always contributed what employers have just taken from my wage to my work pensions since I got put in them just probably not to the percentage I should. The fear of putting too much in a pension or stocks and shares is locking money away that I could potentially need if I found myself out of a job. I am definitely doing some research into it when I feel more in a position to lock some money away

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.9K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.7K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards