We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

IHT Planning

Comments

-

By defintion, if you are living off capital then you do not have excess income.

1 -

See

and note particularly:

Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0

Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0 -

From Marcons link (point 10)

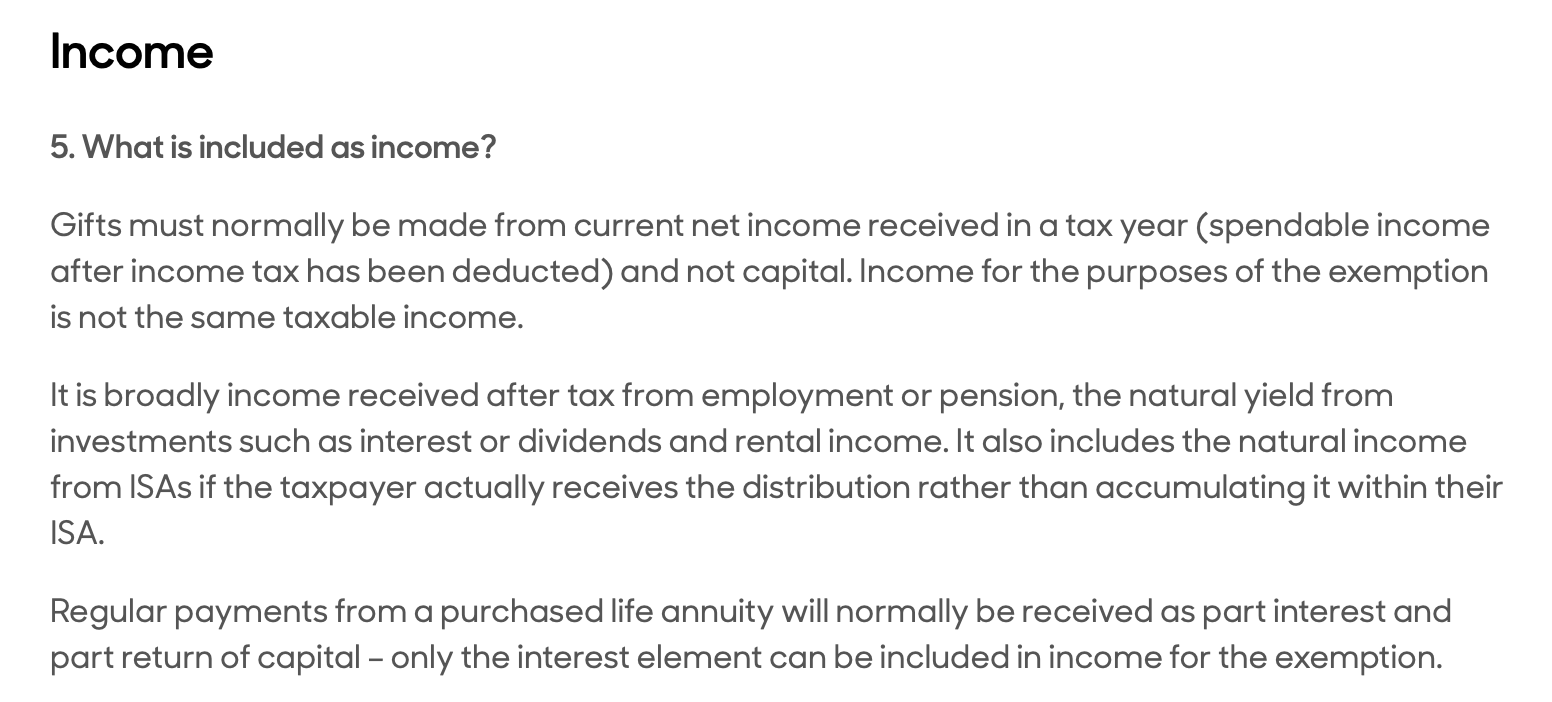

Gifts must be made from surplus income. This is simply the amount by which an individual's income exceeds their usual spending each year. Making a gift from income that is truly surplus should not affect the donor's usual standard of living.

If they have to resort to capital to maintain their lifestyle this is an indication that the surplus is insufficient to cover the gift, and the exemption may be lost or limited. Having calculated income, normal living expenses must be identified to arrive at the surplus.

A lot of people might fall foul of this, by thinking they can gift income then live of ISA savings etc, which will be capital. Especially when now the advice re:pensions seems to be pull out as much as you can each year to live off and fill your ISA.

0 -

That would be swapping 40% (or higher) income tax for 40% IHT.

And so we beat on, boats against the current, borne back ceaselessly into the past.0 -

I just wonder how "capital" is defined when it comes to DC accumulations? Is any withdrawal simply income?…that's how it's taxed.

And so we beat on, boats against the current, borne back ceaselessly into the past.0 -

What about an ISA? That's not taxed as income so I feel that it would be a stretch to have even consistent transfers to relatives classed as "excess income".

And so we beat on, boats against the current, borne back ceaselessly into the past.0 -

My link above relates, but this time see:

Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0

Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0 -

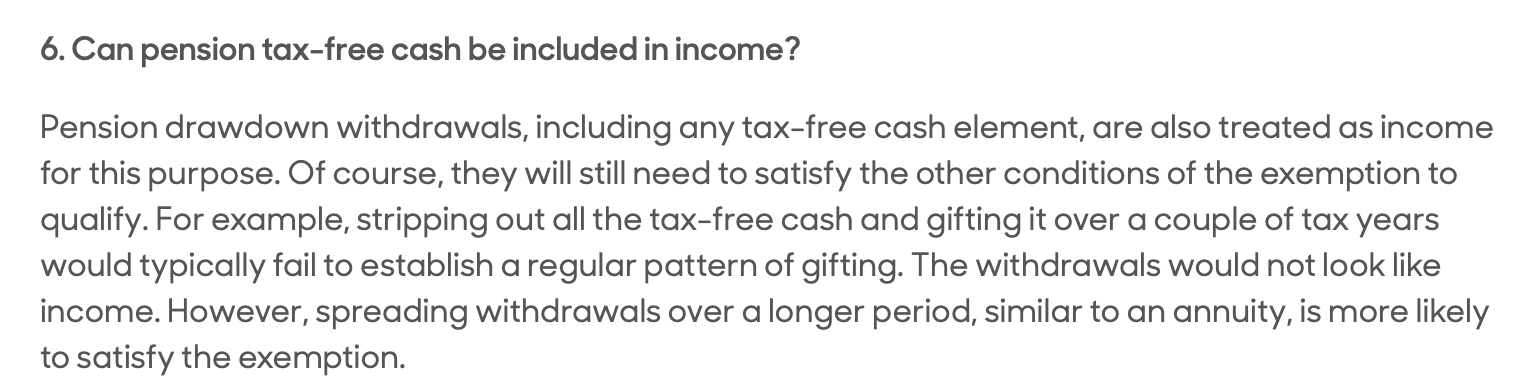

Oops, I had missed that it would be capital taken from a DC pot so would be income (even if assets had been sold within the pension to generate the cash). The tax-free element is interesting because it is questionable as to whether it is "income" or not. I'm not aware of any case law on this yet so probably best to be on the cautious side. As your quote shows, withdrawing a large amount and gifting it over just a couple of years is likely to not satisfy the "normal expenditure" provision and spreading it out over a longer period would fail to satisfy the "taking one year with the next" aspect for the income. Regular UFPLS or simply spreading out the PCLS withdrawals over multiple years would be more likely to qualify.

For taxable withdrawals, there isn't much scope for saving tax given that the IT would end up being at least equal to the IHT for meaningful sums.

0 -

That would be swapping 40% (or higher) income tax for 40% IHT.

If you're into higher-rate income tax you'll be paying 40% on the taxable part of your DC drawdown. Tomahto, tomayto.

N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Kirk Hill Co-op member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

2.72kWp PV facing SSW installed Jan 2012. 11 x 247w panels, 3.6kw inverter. 35 MWh generated, long-term average 2.6 Os.0 -

There's also residence based NRB, but people who are single with no kids or who just want to stiff their spouse or direct descendants don't get that. So they are left with the base allowance of 325k. That seems very low to me...

If your main goal is stiffing your immediate family, giving a healthy chunk of your legacy to the taxman is both an effective and a public-spirited way of reaching that goal, so the lower IHT threshold shouldn't really be a problem.

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards