We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Paying tax on savings interest.

Comments

-

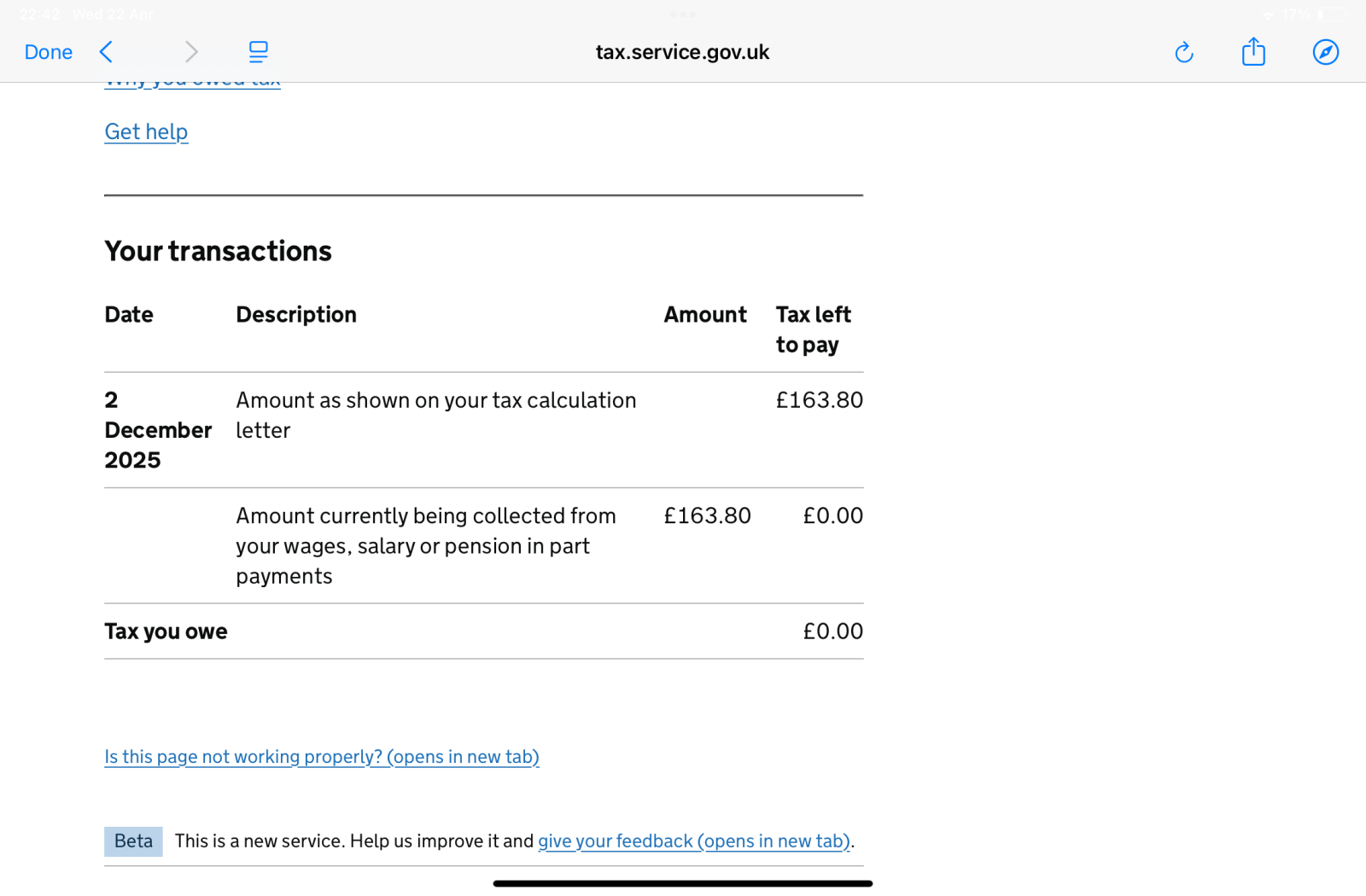

This is what confuses me. Following a letter I got in December 2025 I paid more tax for the next 4 months to cover the £163.80 I apparently owed in tax on the interest over the £1000 tax free limit. But them they say I owe £163 and that will be taken in extra tax for the next tax year 2026/27. But in the 2025/26 they say that extra tax payments had paid it off! Or am I missing something?

1

1 -

It would appear that the £163.80 tax liability arising from 2024/25 was collected via an £819 adjustment to your 2025/26 tax code, but, in the absence of any more accurate information, they'll assume that your savings income will generate the same liability in both 2025/26 and 2026/27 too.

Your coding notice for 2026/27 should clarify whether the adjustment relates to the current year or an earlier one.

1 -

At least it was only £163, they wanted to deduct 7k from me.

Pension payments & interest.

I self assess as interest is over 10k, so after a call they removed it from my calculation.

Pension, wrong again on HMRC’S part.

I received carers allowance for 13 weeks last year, as they don’t have a box for carers allowance, they list pension, jsa, universal credit etc.

After starting work carers stopped, but HMRC want to charge me for it, this year.

After two more calls they removed it.

So my code is 1257L.

0 -

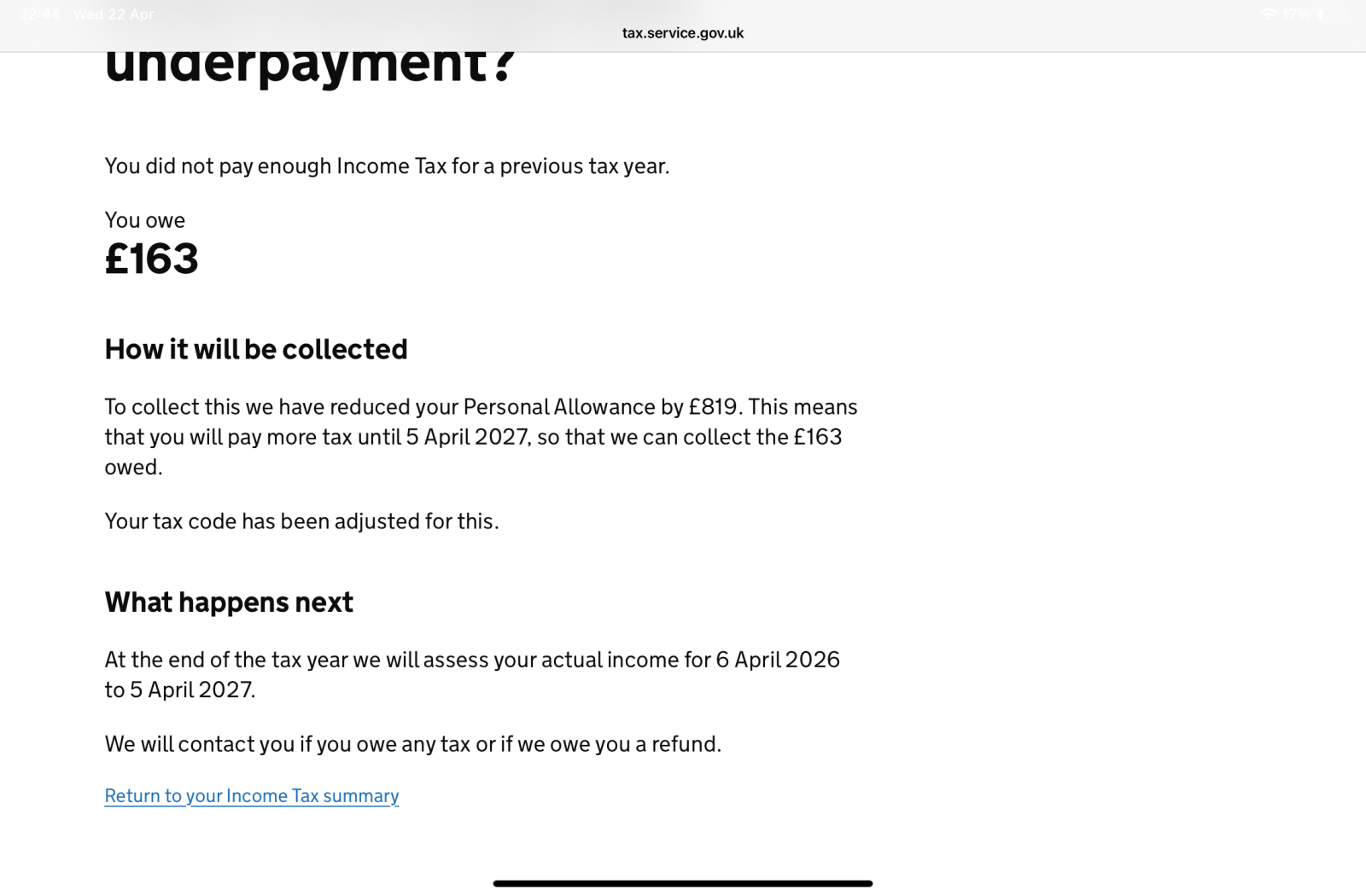

I suspect you have got your tax years mixed up.

What usually happens is that if you owe tax for 2024/25 (which is calculated during 2025/26) then that underpayment will be collected in the next tax year, 2026/27.

But at about the same time the calculation for 2024/25 is issued your 2025/26 tax code will be reviewer and updated, on the assumption that you will receive the same interest in 2025/26 as you did in 2024/25.

Which means the extra tax you were paying in 2025/26 was helping pay the expected tax due for 2025/26, it wasn't paying back the tax owed for 2024/25.

If the interest you actually receive for 2025/26 is less than 2024/25 it may be you will have paid too much in 2025/26 and HMRC will automatically review that later this summer/autumn once they have all the info from banks and building societies and will notify you if there is an overpayment.

3 -

Hello. We have a useful guidance page on our website on the topic of paying tax on savings income: https://www.litrg.org.uk/savings-property/tax-savings-and-investments/tax-savings-income . This includes information on how the tax is paid and checking bank interest figures included on P800 and Simple Assessment calculations by HMRC. You may also be interested to read our new article on this topic: https://www.litrg.org.uk/news/check-savings-interest-figure-included-your-tax-calculation-its-not-always-correct .

“Official Company Representative

I am an official representative of LITRG (Low Incomes Tax Reform Group) part of the Chartered Institute of Taxation who are an educational charity. We are not part of MSE or HMRC. MSE has given permission for me to post on the Forum but this does NOT imply any form of approval of my organisation or its products by MSE. We can’t give individual advice, but if you require further help, we recommend that you contact a tax adviser, HMRC or one of the tax charities where relevant. You can find more information about where to get help with tax here. If you believe I am posting inappropriately please report it to forumteam@moneysavingexpert.com This does NOT imply any form of approval of my company or its products by MSE"0 -

I also reported that.

My savings interest estimate for 25/26 was around £1600 ( based on previous tax year) although it was likely to be more like £1200. So I changed that in my personal tax account in December and subsequently got a letter saying that as I had multiple accounts they needed a breakdown, with provider/account details/interest earned etc

I worked out how much extra tax I would be paying ( also this tax year until it is updated with actual figures) , before it would be corrected

It was about £80 for 9 months, that in theory I could have been earning 4% interest on in a savings account, so a loss of about £3. So I could not be bothered to send the details off.

Another poster was sent a table to fill in rather than just a letter, so some inconsistency with this new development.

1 -

I'm glad HMRC haven't caught up with the fact I don't really need to do SA any more, as to me it seems simpler than all of this.

0 -

Yes, I was blocked from doing SA a few years ago, which was a shame. I think there was a drive at the time to reduce the number of people doing SA.

To rub salt in the wound, the transfer to the main tax assessment system had a glitch, and for a long time I was not in either system…..

0 -

Just keep your taxable savings interest above £10,000 pa and you will be filling in an SA. Other options I believe are BTL property, CGT to report, multiple income streams, or self employment.

1 -

Haha, I like the simplicity of SA. Making my affairs complex to remain in SA would be rather defeating the object. At present, the only income I declare that isn't from my main employment is Untaxed UK Interest (never as high as £10k) and "Gilt etc" interest (the latter I would have to declare in some way to HMRC each year).

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards