We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Tax on a prepaid card for charity

Comments

-

And they're trying to do so, fee free even though the possible fees represent a tiny proportion of that spend.

Perhaps the OP needs to accept that for what they want to do, a small fee is payable?

1 -

Daily spend can be a lot more than £1000. We need both ATM cash and card spending.

0 -

If you check the rest of this thread you will see that we are a charity and the money is spent on charitable purposes. We need prepaid cards in order to control spending.

0 -

If the OP is an officeholder (e.g. trustee or director of the charity) or an employee of the charity then the normal employment income tax rules will apply.

Assuming the OP genuinely spends all the funds put on their personal prepaid card on charity things and accounts for it all, the issue is likely to be the calculation of the beneficial loan interest (if it ever exceeds £10,000).

If the OP spends anything on the prepaid card on personal things (without having prefunded at least this amount themselves, and even if they later reimburse the charity) then it starts to get quite interesting from a tax perspective. A lot will depend on what is contractually agreed between the individual and the charity, and what happens in practice, but it's easy to see how this could tip into the PAYE/NIC regime (and then claiming income tax relief for the genuine expenses).

If the OP is not an employee or officeholder, the above isn't really relevant unless the OP makes a personal profit on it. Then they'd have to think about the miscellaneous income rules.

Putting tax aside, what would happen if the topped-up prepaid card was lost or stolen? Presumably, the OP would bear the risk of the loss of their personal card here and have to use their own resources to buy the stuff? If so, why would a volunteer want to be exposed to that risk? If it is the charity that takes on that risk, the governance would make me quite reluctant to donate to that kind of charity.

3 -

We are a small charity and I always aim to devote every last penny of our funds towards our charitable purposes. I hate it when corporations swallow any of it in fees. I may well have to accept a fee but £25 per month to Equals is not acceptable. There has to be a more reasonable deal.

0 -

I will cut to the chase as someone who from time to time in the past, was professionally called upon to review charity accounts and practices, albeit charities established by wealthy patrons rather than public donations.

Had I come across the scenario you now propose, this would occasion a big red flag to the trustees as a prima facie failure of governance and prudent financial controls.

The opportunity for fraud is self apparent, and the charity commission would be wholly unimpressed if the charity's Auditors or Independent Examiner failed to identify this as a weakness in the charity's financial systems and operations.

There are clearly ( cheaper) alternatives to the pre paid operator you now have an issue with if you bother to click on the link I sent.

Your desire to access low or zero cash management services on behalf of the charity is laudable, but I suspect were you to put your idea to the Independent Examiner for the charity, their concerns would be the same.

4 -

I agree with the comments made above by poseidon1.

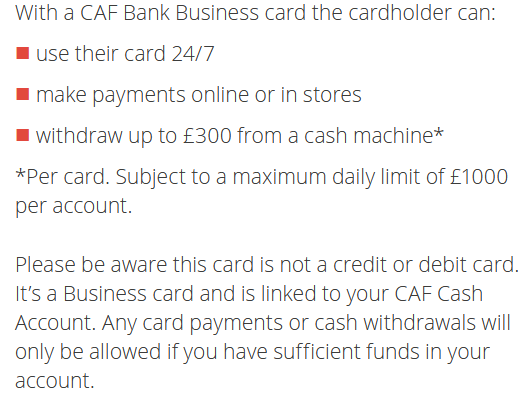

My earlier suggestion of the CAF Bank business card was intended as a helpful suggestion that might well work within a much better controlled framework than you have talked about. I think it has been dismissed too quickly and for faulty reasons.

The £1,000 is NOT an overall daily spend limit. It is only a limit on cash withdrawals. From their bank business card guide:

This also makes quite clear that it is NOT a normal credit or debit card. Spending is restricted to the balance in the account.

One of my suggestions was to use this in addition to whatever bank account you currenly use. Then your charity could transfer into the CAF account, whenever it wished, whatever sum it wanted you to be able to spend at that time. Surely that's just the same as a prepaid card?

So what's the remaining problem? I'm having real difficulty in believing that you need to spend the £20,000-£30,000 in cash. If that really is the case, surely you can say something about why it has to be in cash? Without a realistic answer, that's another red flag.

Often in this sort of situation (seeking a replacement for something) people start their thinking from how they do things now, and look for a direct alternative, rather than being clear about what they need to achieve and therefore open to considering a different approach.

2 -

"I'm having real difficulty in believing that you need to spend the £20,000-£30,000 in cash".

That's not what I said. We spend that combined amount via both card and cash. Our charity work is abroad and we require quite a lot of flexibility. I really don't appreciate what you are hinting at with mention of "red flags".

Thanks for the suggestion of CAF but it does not fit our particular needs at the moment.

0 -

Our charity work is abroad

In what currency is the £30K spend?

1 -

I think the ideas you have about using personal accounts on the other thread, to avoid really very modest fees actually sound quite dodgy from a governance perspective - I appreciate that you want to maximise the value of your donations, but you also need to be accountable to your donors. The fees banks want are just overheads much like advertising your charity / cause, minimise them, but don't lose sight of also needing to be accountable.

I'd be uncomfortable donating to a charity that does questionable things with my donation, which leaves the charity (and you) wide open to accusations of fraud.

3

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.7K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.5K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards