We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

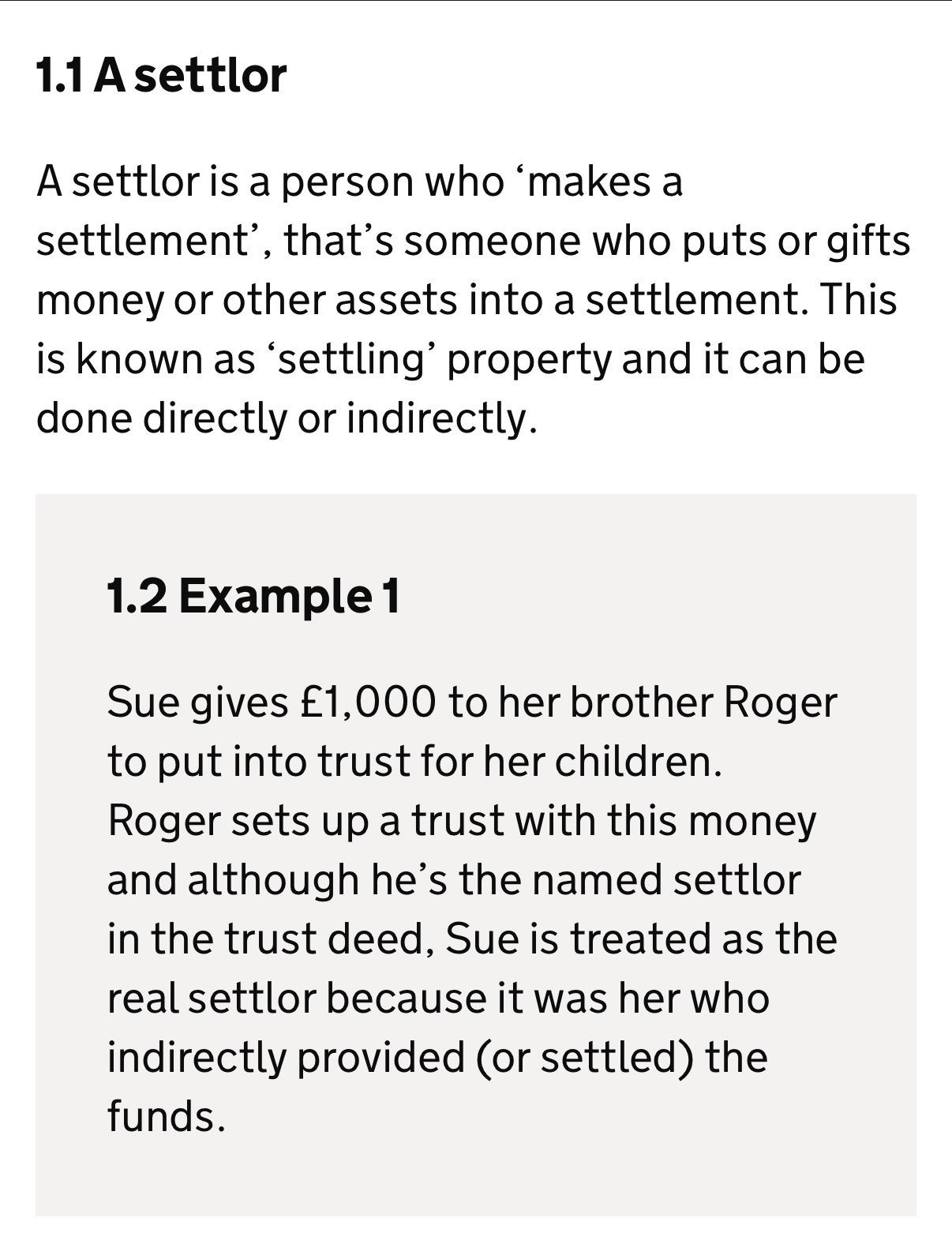

Bare Trust Investment Account - For Minor's Own Assets

My child is beneficiary of an IIP trust settled by my late father. From this trust my child receives mandated income and, if income is sufficient, pays tax. The income is his absolute property.

The primary intent of the IIP trust was to generate income to contribute towards education; initially building up a surplus which is now eroding as fees outstrip income. While the surplus has, until now, sat in a bank account, we now wish to invest some of this surplus in gilts / funds via a trading account, in order to retain the ability to draw down before he is 18 to cover fees if necessary.

I tried to setup a bare trust investment account at AJBell. I say tried, as we have hit an issue in that I registered the trust with TRS stating the child as Settlor and Beneficiary, as the settled funds are their absolute property and hence it is their property settled into trust.

AJB state a minor can't be the settlor as they lack capacity to sign a contract/deed and that the settlor is the person who put the assets into trust by signing the trust deed, not the person who owns the assets that were put there.

Their interpretation would make us, as parents, settlers as the deed is signed by us, on behalf of the child. However, I am aware of the tax treatment when a parent puts their own assets into trust for their child, hence it is important to ensure it is recorded correctly that the assets were already owned by the beneficiary!

HMRC shrugged their shoulders and said to seek tax and/or legal advice as they didn't know! I plan to do this, but thought I would throw this out there in case someone else has sought such advice.

Comments

-

AJB state a minor can't be the settlor as they lack capacity to sign a contract/deed and that the settlor is the person who put the assets into trust by signing the trust deed, not the person who owns the assets that were put there.

Their interpretation …………

It isn't "their interpretation". The settler is the person putting the money in the trust, and your child is the beneficiary of the trust set up by your father.

A child cannot execute a deed, so cannot set up a trust and so cannot be a settlor. Only an adult with mental capacity can do that.

That's not a matter for "interpretation".

2 -

Is there perhaps another grandparent who could set up the bare trust with say £1 and go on whatever documents and forms you need to do as the settlor? Then could you arrange for the income payments from the IIP trust to go direct to the bare trust as payment "to the child"?

0 -

If I understand your post correctly, you are not querying what to do about the primary IIP trust fund by way of investment ( which I assume is invested in a mix of assets for income and growth), but how to invest the income accumulated from the trust investments, which you say is your child's absolute income under the terms of the trust.

You say this 'surplus' income is sat in a bank account. Is that account in the name of the trust or the child? If its in the name of the trust, its no surprise AJ Bell do not consider those funds qualify as 'bare trust' monies.

If the account is in name of the child, I see no reason why you could not use junior ISAs with platforms like AJ Bell to access gilts that way

However, i have a more fundamental question. You describe the trust as an IIP trust, but this category of trust became very limited in scope after March 2006 - as set out in the article below -

What I am staying is if this trust was set up long after 2006 for a child who is currently under 18 it is most unlikely to be an IIP especially if it was established under the terms of your late father's Will. If set up during his lifetime ( after 2006) the trust capital also falls under the discretionary trust IHT regime even if the trust clauses gives your child an outright entitlement to the underlying trust income.

So need to be clear exactly what type of trust was settled for the child, and if it was via your father's Will was the right to income expressed to be for the child's lifetime, or was there a vesting age at 21 or 25 at which point the trust capital then belongs outright to the child.

Supplying the exact wording of the trust clauses ( personal details redacted ), should answer these points.

1 -

I appreciate the time to read and reply, but HMRC have explicitly told me that I’m not the settlor if the assets put into trust are not mine!

However, they can’t tell me who is and literally said it’s down to interpretation of the relevant legislation which does not explicitly provide for this scenario. Their words, not mine!

Hence, per HMRC, it is AJB’s interpretation of who the settlor is in this scenario and their interpretation does not agree with explicit verbal advice from HMRC.

I’m not arguing that a minor can’t create a trust and sign a contract. However, it comes down to whether, when the person signing the deed is not the owner of the assets, who is the settlor? Is the settlor is the person who signs a deed or the person whose property is put into the trust.

HMRC has a something relevant in HS270:

AJ Bell appear to what the Settlor as named in the deed, not the real settlor!

0 -

Interesting idea, will run that by my adviser when I speak to him next week

0 -

https://forums.moneysavingexpert.com/discussion/comment/81967576#Comment_81967576

Yes, it is the investment of the income from the original IIP trust, held in a bank account in the child’s name.

Use of a JISA is not preferable due to locking it in until they are 18.

Trust was established during my father’s lifetime, but was after 2006 (was 2011 ish from memory, would have to dig out the deeds). Deed is pretty lengthy and was created by a lawyer and chartered tax advisor.

There are actually 8 trusts (Rysaffe) and the beneficiaries are all defined as classes (descendants of …) etc.

I’d have to go back to my notes from the adviser from when I took over as Trustee when my father passed away 6 years ago, but I do know there is provision to withdraw capital.

0 -

I appreciate the time to read and reply, but HMRC have explicitly told me that I’m not the settlor if the assets put into trust are not mine!

Of course you're not the settlor of the money of which your child is the beneficiary. I didn't say that you were.

My point is that your child cannot be a settlor of a trust because he is a minor. He cannot put the money into a trust.

It is not your money so you cannot be the settlor either. You can't create a trust and settle the money.

However, it comes down to whether, when the person signing the deed is not the owner of the assets, who is the settlor?

There isn't a settlor and there isn't a trust. If the person executing the deed is not the owner of the money then they can't settle money in the trust, and no money is settled in the trust. The person executing the deed isn't a settlor, and the deed is ineffective. No trust is created. The whole thing is a nullity.

In relation to @DRS1 's idea, you wouldn't be able to pay the income into a trust ( the legal term for which is settling money) for the reason given above - you can't settle money in any trust when the money isn't yours. That includes your son's money into a trust for his own benefit. And he can't do it himself.

1 -

This make more sense, but if it’s not possible then why would HMRC not say that to me, or in their own example.

Lawyers also set up trusts ‘as agent’ for people without the capacity; there is precedent there.

My intent was to use my fiduciary responsibility for the child to place their assets into trust - purely to allow me to invest them on their behalf.

It’s not really any different to managing his money in his JISA or JSIPP (ignoring the obvious tax implications on income/gains).

0 -

There is a trust. Your child is the beneficiary. Income arises on trust assets and this income (which is high enough to be liable to tax, presumably paid by the Trustees on his behalf) is owned by the child absolutely.

This income (or part thereof) has been accumulating in a bank account which is in the child's name and wholly owned by the child but presumably with you named a "bare trustee" as here.

In such an account, the money could have been gifts to the child from a parent but could have been from a grandparent or indeed from "Uncle Tom Cobley and all" with nothing at all from the parent .

You now wish to open a dealing account which will receive the child's money and be used to buy investments (so requiring registration).

This money has been derived from a trust the settlor of which was your father.

Can your late father be named as settlor (the settlor does not have to be a trustee) and you and your child's other parent as Trustees?

https://www.hl.co.uk/investment-services/investing-for-children/bare-trust-account

0 -

If the grandfather were alive, there would be no question that the income paid out from the trust was not his. As you say, it is owned by the child absolutely.

Even setting that aside, it would be difficult to argue a deceased person has capacity, and presumably has not specified any such instructions in a will.

I'm a bit confused by "The primary intent of the IIP trust was to generate income to contribute towards education; initially building up a surplus which is now eroding as fees outstrip income." Given the money is in a bank account "fees" must refer to school fees. If school fees now exceed the ongoing income, then won't the surplus be gradually consumed from this point forward? Is it not possible to earn interest at a rate comparable to what could be achieved in gilts/funds, in an increasingly tax efficient manner, given the child's lack of other income (my assumption)? Whereas if the school fees are to be funded some other way and this money used for university, then that would align with JISA access (although it would require the child to go along with this when they gain access).

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards