We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Fundsmith again.

I've held Fundsmith for many years and it did very well for me. I sold out of the ISA a some years ago for better options because no sell liabilities, and have slowly brought down the GIA amount in CGT exemption steps. In the days of 12.3k exemptions this was pretty easy, but now with 3k it is more difficult. I've never actually paid any CGT so far, just used exemptions every year… this morning I just sold 3ks worth a gains in the GIA Fundsmith to top up the ISA.

Looking at the recent figures it remains my worst performing holding, I'm not saying it will go bust, but it's beginning to look a bit like Woodford in that the long term record is holding up some very poor shorter term performance, which I don't think they can recover to make performance competitive again with similar high cost competition. Amazingly some brokers still have it in their recommended lists - which reminds me of Hargreaves Lansdown and Woodford!

Opinions please, would you pay CGT to liquidate, and hope another choice would have better performance to pay for the tax lost compared with standing still in lacklustre gains?

Comments

-

After spending working years taking advantage of investment tax breaks - especially for SIPPs if you are a higher rate taxpayer - it is a psychlogical shift to pay tax. It's also a shift to spend from your investments during retirement and watch the balance reduce. Both of those are shifts you have to make (if you have sufficient assets) to enjoy your life rather than hoard assets. I don't know if either/both of those apply to you, but it's a necessary and healthy process to go through. If you hold on to Fundsmith and watch it continue to underperform, will you still think you have made the right choice? If I were you I would bite the bullet, remembering that if Fundsmith had performed the way you wished, you would have more CGT to pay and might be running in ever increasing circles to stay within the £3k allowance.

1 -

If you have any loss making investments in your GIA, don't overlook selling those to realise a loss that can mitigate or counteract your Fundsmith taxable gains on disposal.

Generally, with the much reduced annual CGT exemption, more and more investors will have to contemplate paying CGT on GIA gains not only in respect of declining previous performers ( such as Fundsmith), but also very high performers whose gains have disproportionately unbalanced their portfolios from a diversification point of view.

Important point to appreciate is if one is wealthy enough to accrue sizeable portfolio wealth outside tax free wrappers, tax thereon ( both income and CGT ) should be seen as part of the investing process. Certainly that was the viewpoint of my wealthy clients, even when the CGT exemption was considerably higher than present.

3 -

I would not let short term taxation tactics drive your long term investment strategy. I would also not be looking for another "winner" to replace Fundsmith as who's to say it won't take you on a similar journey.

And so we beat on, boats against the current, borne back ceaselessly into the past.1 -

"Opinions please, would you pay CGT to liquidate, and hope another choice would have better performance to pay for the tax lost compared with standing still in lacklustre gains?"

This is sounding rather like a sunk cost bias. You are asking whether you should incur tax at X% of the valuation of your holding in order to avoid Y% of underperformance over the next Z years. You need to quantify X and then you can begin to figure out if Y*Z might end up being more. If X is quite a low number (remembering that it's based on the value of the holding not just the gain), then the decision may be easy.

1 -

masonic, That is exactly the sort of formula I have been wrestling with.

Unfortunately no losses to offset any gains.

I've done very well from "winners" over the years, but the number of researched long termers available seems to get less and less as time has gone on and my trackers become a larger and larger part of the whole. Nevertheless I have "satellites" apart from the wealth preservation funds which provide a bit of excitement and some great returns, Fundsmith was one of them.

I could still sell a winner for a 3k gain and have >20k in proceeds to transfer to the ISA, but Fundsmith now only gets me 10k tax free so the rest would have to come from savings.

But savings are taxed at 40% and CGT taxed at 24% I suppose is a no brainer for running savers to the minimum required..

aroominyork, you are correct, it is the psychological effect of paying CGT for the first time that offsets the maths saying it's the correct thing to do.

0 -

So about a third of the holding is gain. That means an effective loss of approaching 8% if you liquidated your entire position now. That's well within the noise of equity investments and it's entirely possible you could end the year better off overall by switching fund.

2 -

Looking at the recent figures it remains my worst performing holding, I'm not saying it will go bust, but it's beginning to look a bit like Woodford in that the long term record is holding up some very poor shorter term performance, which I don't think they can recover to make performance competitive again with similar high cost competition. Amazingly some brokers still have it in their recommended lists - which reminds me of Hargreaves Lansdown and Woodford!

Any reference to Woodford's fund is a little silly and emotive here - Fundsmith is simply a fund where the manager's investing style was ideally matched to the market conditions at its launch and for its initial ~10 years, delivering very good returns. Conditions changed, and that same strategy no longer performed as it had previously. At some point, market conditions may once again come to favour the manager's style and performance may again become strong.

The defining characteristic of Woodford's fund is that it had a fundamental mismatch between the liquidity of its holdings and the liquidity offered to fund holders. Fundsmith has no such structural flaw - it's just a fund, like many other active funds, that has periods of outperformance and then periods of underperformance vs some relevant comparator.

Also, your comment, "I don't think they can recover to make performance competitive again with similar high cost competition" doesn't really make much sense to me, since it implies some sort of "catching up" is required. For anyone choosing to hold Fundsmith from today, its past performance is irrelevant - that's history and cannot be banked by today's or tomorrow's holders of the fund. All that matters to them is how it'll perform in the future.

Sorry, but I think you've tied yourself in mental knots here. I suggest you simply assess whether Fundsmith's portfolio of assets, and its well documented approach, represents something that you wish to buy into (or remain bought into, if already hiolding) for the coming period. If so, hold, otherwise sell. Take account of tax in these decisions, but don't be ruled by it.

8 -

I did say its not going to go bust, so the comparison was tongue in cheek and you take it too seriously.

The fact remans that the last years have been diabolical compared to peers with the same charges, let alone cheap trackers, and it is only his 10 year figure which now holds up. I think he's off in Mauritius and now got so much money he's just not as sharp as he once was and lost that edge. I will stick my neck out and say that any recovery can't make up for the loss of these years in the long run, and the chance of a recovery has decreased in the era of high interest rates and now US chaos..

1 -

I dropped Fundsmith about 3 years ago…the worst of the funds I moved into or already held is up over 50% in that time compared to Fundsmith +3%. Shorter term is even worse. I’d dump it..there are numerous better options offering investment in quality companies…

3 -

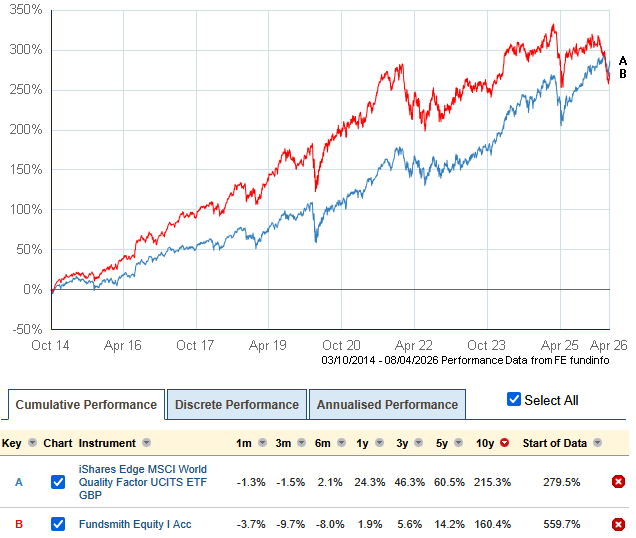

"…numerous better options offering investment in quality companies". The starting option is a world quality ETF like IWFQ, launched in 2014. Up until about five years ago Fundsmith beat it hands down; since then the ETF has been miles ahead. The ETF will select companies using metrics such as profitability and debt. At Fundsmith's annual shareholders' meeting Terry Smith will present his holdings' strong performance against similar metrics, yet investors' bottom line of share performance can be wildly different.

1

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.7K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards