We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Interest added monthly or annually.

Comments

-

Interest cannot compound until it's been added

I consider myself to be a male feminist. Is that allowed?0 -

2 accounts - same AER. The gross rate for the annual will be the same as the AER and the gross rate for the monthly will be a little less. If the monthly payments are retained in the account it will have the same interest as the annual account after 1 year due to compounding

If the accounts are closed before a year you will have accrued x number of months at gross interest rate (same as AER) in the annual account while the monthly will have accrued x months at a lower gross as it has not had enough time for compounding to equalise the return expected after 12 months

The critical point is that the accounts have been closed early. Had the accounts run for a whole year the interest would be the same

5 -

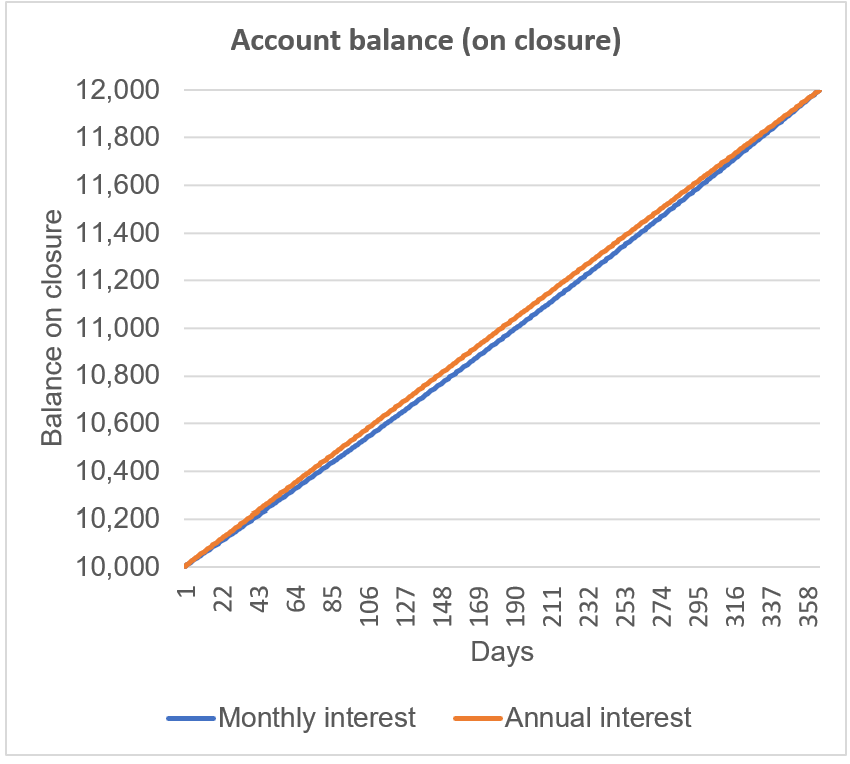

Masonic is correct that the account balance on closure is usually higher on closure with annual interest rather than monthly interest in circumstances where the AER is the same for both options.

If we take a £10,000 single lump sum deposit the figures look like this if the AER is say 20% and annual interest is paid after 12 months. Note it's necessary to choose an artificially high interest rate to see the affect on a chart.

What is happening is under the n/365 method used by most savings institutions (daily compounding is very rarely used), the interest is accruing uniformly under the annual approach. Under the monthly interest scenario it curves up slightly over the year (or more accurately it's 12 straight lines that joined together curve upwards). So after 12 months the closing balance is the same but at 6 months in this example the closing balance is higher under the annual approach.

For a more realistic example of a single payment of 50K invested over 6 months at an AER of 4% the annual interest option wins by about £10 on closure after 6 months.

I came, I saw, I melted6 -

The way most accounts work is that they accrue interest daily at 1/365 of the gross rate based on the closing balance on that day. Most monthly accounts will state they pay and compound interest monthly. On leap years some give an extra day while others use 1/366.

Compounding takes place as a result of interest being credited to the account and increasing the balance accordingly.

Taking, for example Charter Savings Bank's 4.01% AER Easy Access Issue 73 account, the monthly option pays 3.94% gross pa, whereas the annual option pays 4.01%. This gives daily gross rates of 0.010795% and 0.010986% respectively.

In the extreme case of opening such an account on 1st April and closing it before the end of 30th April (29 days interest), you would earn on a £10k balance: £31.30 in the monthly case and £31.86 in the annual case. The closer to the 1 year mark you hold the account, the closer the interest will become due to compounding in the monthly case.

There are some exceptional cases where interest compounds daily, but this is very rare. They can be identified by the difference between gross rate and AER, which adheres to the following formula:

AER = (1 + gross/n)^n - 1 (where n is the number of compounding periods (1 for annual (AER=gross), 12 for monthly, 365 for daily))

At 4% AER, the corresponding gross rates would be: 4.0000% for annual, 3.9285% for monthly, and 3.9222% for daily ( which is close to the continuous value given by ln(1+AER) = 3.9221 )

4 -

Thank you, everyone - and SnowMan's graph helps a lot - maximum relative advantage about midway.

For a long time I had thought that annual interest was being internally compounded, rather than a "same increment each day" approach, and had forgotten that again.

1 -

Thanks, I'll stand corrected…

ps I should add that at least one OakNorth account I've had accrued interest daily (but was not actually available for withdrawal until the end of each month) - obviously fairly unusual.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.9K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.7K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards