We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Car insurance

I've just switched car insurance for the first time in a long time. My policy was £80 cheaper with Churchill comprehensive plus than staying with LV.

I now have the fear of what if LV is a better insurer and it would have been worth sticking with them? My insurance doesn't change for another week although I have paid churchill already.

Looking at it the protected no claims may be better with LV?

I'm a little burnt out & perimenopausal so everything feels like a huge decision. I just wondered if anyone has any advice

Comments

-

You would need to compare the cover to make sure you are comparing like with like. Why do you think the protected no claims may be better with LV? I don't think there should be any difference.

1 -

Don't sweat it. Double check your old vs new policy to make sure youre getting all the cover you need (legal, personal accident, courtesy car etc), but tother than that theyre probably almost identical.

1 -

Thankyou. Looking online i noticed this after I had purchase the Churchill insurance

0

0 -

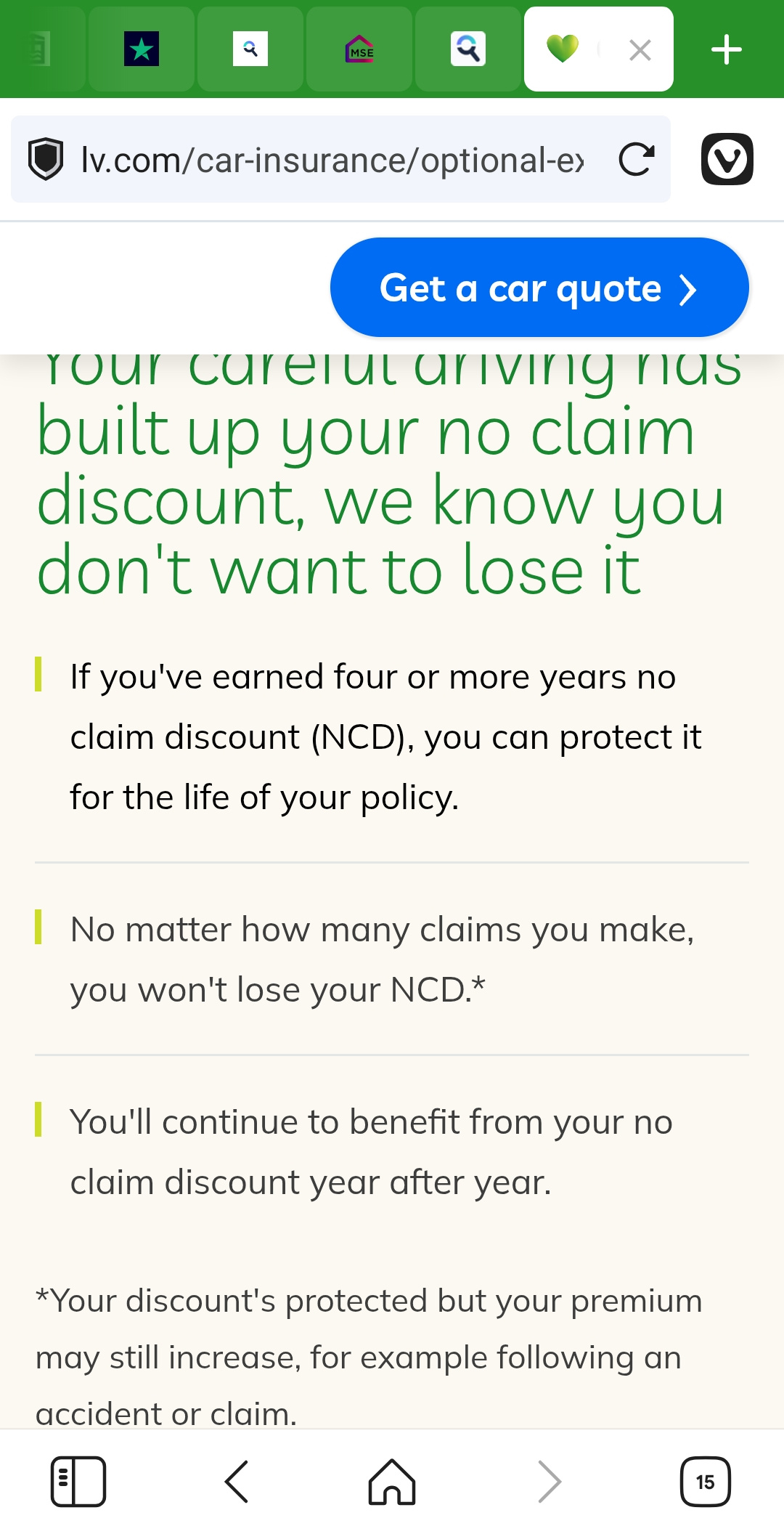

If youve got 4+ years ncd, youre unlikely to have multiple accidents suddenly, but knly you can say how much you value that certainty.

also NCD may not have as big an impact as you think. Use a different laptop/pc/browser and get a new identical quote with 0 years ncd and you can see how much its saving you.

1 -

Reading that, they look identical to me. The only difference is that Churchill has highlighted what would happen if you made a claim. LV will have very similar terms. You can find their terms by reading their policy wording.

1 -

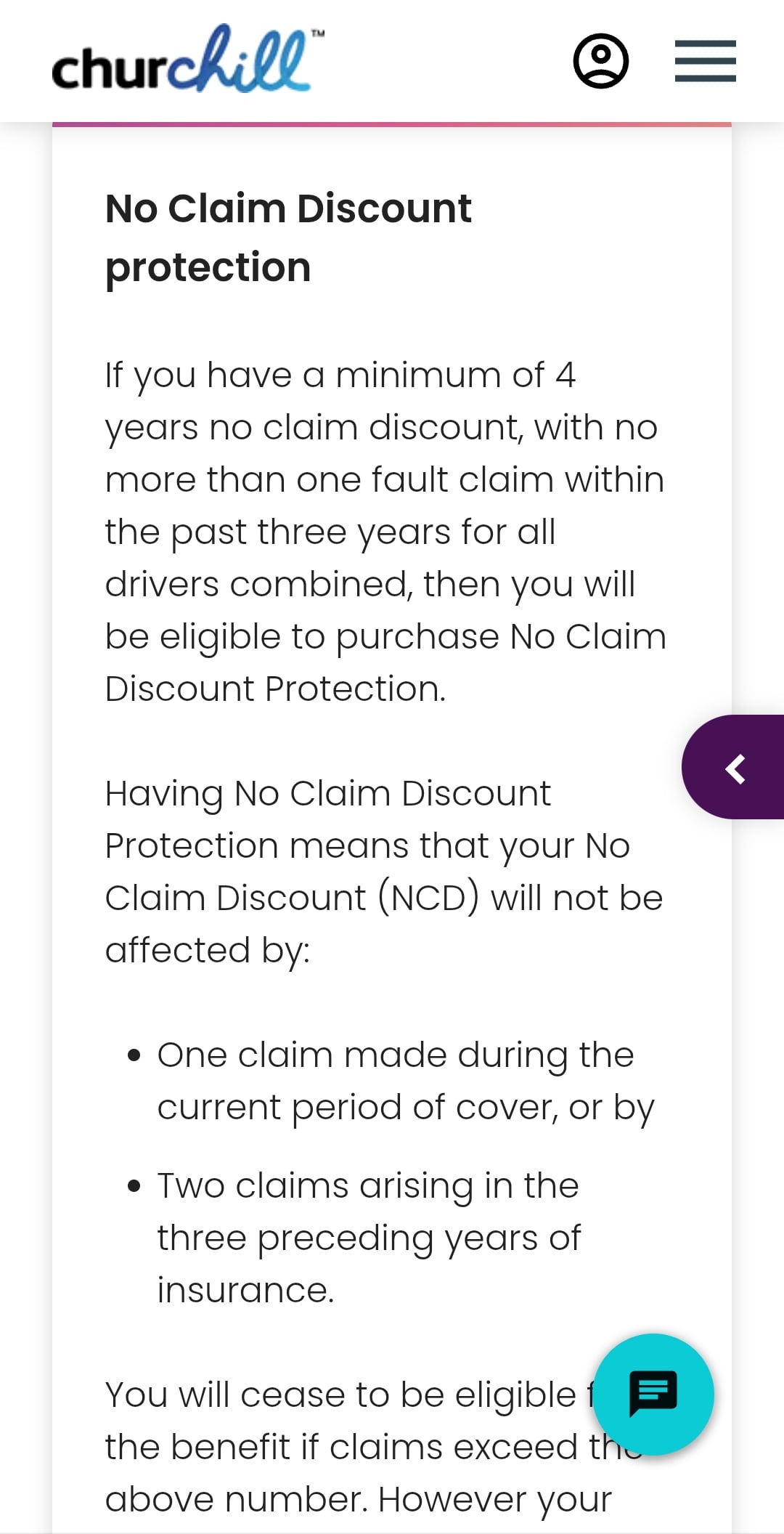

LV has unlimited claims, Churchill only protects your ncd for one claim per year, and 2 claims in three years.

2 -

For what it's worth, I've just done the reverse. I was with Churchill last year but got a far better quote from LV than my renewal quote from Churchill which was significantly higher than last year . I did call Churchill but, although they managed to reduce it a bit, they couldn't match the LV quote. The policies are comparable.

Of course I probably have a different car, driving history, NCD etc from you but I think it just shows it can pay to shop around.

1 -

I missed that on the screenshots. Thanks for pointing it out.

0 -

Churchill's NCDP is inline with how most insurers write it. LV= is the outlier allowing a theoretically unlimited number of claims. What can't be predicted however is if LV= would actually offer you renewal terms if you did make 6 claims in a year.

How many claims have you been making? What percentage is £80 of the lower premiums? It's certainly possible for someone to have no claims in 20 years then suddenly have two claims in one year but it's fairly unusual unless the local kids decide vandalising your car is their new favourite hobby. Even then you'd need to see if Churchill still has its "vandalism promise" which would mean its not considered a fault claim anyway.

Insurance is ultimately a risk transfer mechanism, you trade the risk of a big loss for a certain small loss (aka the premiums). It's up to you to decide how much risk you feel your NCD is under and if £80 is a reasonable premium to offset that risk.

1 -

Thank you so much everyone, it is really appreciated and really helpful

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards