We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Rebalancing ISA - where to start

Comments

-

Not wishing to make it over-complicated but would it not be cheaper hold ETF's (whether it's 1,2 or 3 etc) than funds(OEIC) due to the capped platform fees on Fidelity?

Downside of ETFs IMO is less flexibility in options in particular multi asset offerings so should be considered too.

0 -

Mulit-asset type funds usually have boards and rules that the managers must work within. VLS type funds have set amounts of each fund owned. Investment trusts do something similar, but maybe with a bit more latitude and then you have more ego and personality driven investments like Woodford, Fundsmith and even Berkshire Hathaway.

And so we beat on, boats against the current, borne back ceaselessly into the past.0 -

Two answers, take your pick.

- The pros know the theory is to take profits and they probably pretend they do it, but in practice probably make the same mistakes the rest of us do.

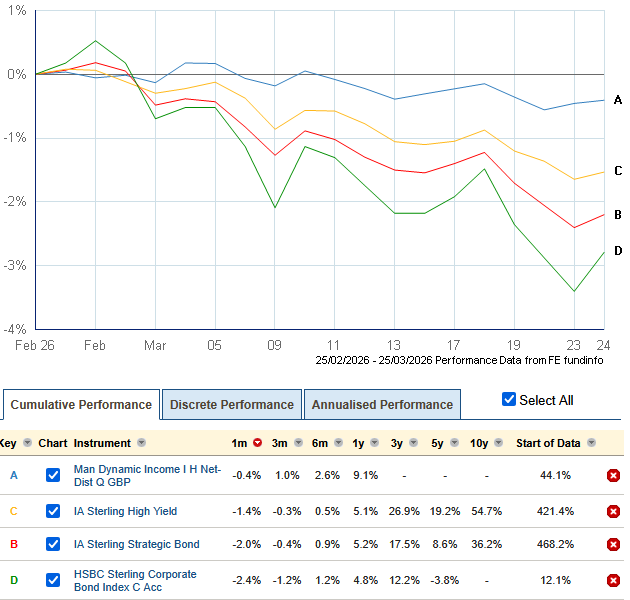

- Equity fund managers tend to have a style they stick to. Fixed interest has strategic bond funds which, in theory, give managers the full govt & corporate, long dated & short dated, developed & emerging, IG & junk sectors to choose from. In practice they are probably as constrained as any other manager. I'm not convinced my Artemis Short-Duration Strategic Bond - with one manager for govt, one for IG and one for high yield - will take any spectacular tilts which will make me rich, even when they see the wind changing course. (btw, masonic, hasn't Man Dynamic Income held up well this month?)

0 -

Your losing me now, but if I’ve got this right:

Sell all the global funds and instead buy into a global tracker- so probably the L&G one as some money is already there. Keep some in a UK tracker if I want a UK bias. And that it’s.

And I don’t lose anything, other than the short time out of market, by making these moves?

So glad I posted. I was thinking of having to balance up with more pick’n’mix.

One more question: I seem to have the ‘acc’ and the ‘inc’ version of the international tracker, which should I go for?

I'm a Forum Ambassador on the housing, mortgages & student money saving boards. I volunteer to help get your forum questions answered and keep the forum running smoothly. Forum Ambassadors are not moderators and don't read every post. If you spot an illegal or inappropriate post then please report it to forumteam@moneysavingexpert.com (it's not part of my role to deal with this). Any views are mine and not the official line of MoneySavingExpert.com.0 -

In the "mandate/style" point, it was actually strategic bond funds I was thinking of as exemplars. We don't see much of this in the equities space, despite there being an undeniable demand from retail investors for funds that can perform across the economic cycle, suggesting it cannot be done effectively in practice.

@aroominyork I think Man Dynamic Income has held up as expected this month. When I compare to my volatile junk bond IT of choice, NCYF, it dipped 5% and then regained half its losses, so this part of the bond market held up pretty well in general.

Yes, but if you want to keep one or two of your pick'n'mix as a small "fun" part of the portfolio, then that is reasonable. For the Acc/Inc question, it comes down to what you intend to do with any dividends (which won't be huge on a fund like this). Acc means they'll get automatically reinvested with no effort from you, whereas Inc gives you more freedom, but you'll need to reinvest yourself or set up an automatic withdrawal.

1 -

Also on Acc/Inc, most people choose Acc for ISA/SIPP where the dividends are automatically invested within the price of the fund, and Inc for GIA (not SIPP/ISA) because it makes calculations of capital gains tax easier. That said, an IFA on this forum recently said he always uses Inc so he can chose which holdings to top up. I don't think that is your situation and is more likely to lead you back down the pick 'n mix route.

@masonic, I think Dynamic Income has done better than "as expected". it has hardly drawn breath.

0

0 -

"I think Dynamic Income has done better than "as expected". it has hardly drawn breath."

Yes, I suppose it does stand out amongst most of its peers, and Golan made the right call to remain short-dated. Fidelity's strategic bond fund achieved something very similar in the short term from quite a different portfolio (mostly intermediate duration US Treasuries). Which is quite interesting.

0 -

The title of your post asks about rebalancing, so do you know how much you want in each of your funds and why? Rebalancing implies that you have a target asset allocation you want to get back to. Your IFA should be doing all this for you, but I get the impression that they have checked out a bit. You need to grasp a bit more about the type of funds you own and why you own them.

And so we beat on, boats against the current, borne back ceaselessly into the past.0 -

Terminology can be confusing and I don't think rebalancing is the right term here. The OP is really talking about simplifying their portfolio by reducing the number of funds.

0 -

Both simplifying and rebalance. So I don’t have over exposure to one sector by having a fund from solely that sector and a more general tracker. Also, the funds that have done well now mean that the sector is taking a greater percentage of the total than originally intended.

I'm a Forum Ambassador on the housing, mortgages & student money saving boards. I volunteer to help get your forum questions answered and keep the forum running smoothly. Forum Ambassadors are not moderators and don't read every post. If you spot an illegal or inappropriate post then please report it to forumteam@moneysavingexpert.com (it's not part of my role to deal with this). Any views are mine and not the official line of MoneySavingExpert.com.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.9K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.7K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards