We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

IHT435

I am finalising my paperwork for submission to HMRC.

My mother died in 2002. My father died in December 2025. He did not remarry. His will leaves everything to my sister and I split 50/50.

I am in the process of claiming a transfer of the Residential Nil Rate Band from my mother for my father's estate. Her estate was less than the taper relief figure (verified by the probate grant) so there should be a transfer of £100,000 relief.

All was straightforward until I got to the section on other Assets - questions 19-24. The proceeds of the sale of my father's property (he moved into care in February 2024) are known to me.

Q19 generates the answer yes because, for example - there are some stocks are shares in estate.

Q20 No

Q21 has me stumped. How do I calculate the value of the other assets passing to direct descendants?

The guidance note at point 17 says the value is after the deduction of any exemptions, or business relief or liabilities that is taken into account for Inheritance Tax purposes on other assets.

At the moment those " reliefs" amount to £600,000 (made up of £325,000 nil rate band and £275,000 residential nil rate band - £175,000 for father and £100,000 transferred from Mother).

So how do I calculate a correct answer to Q21?

Any help much appreciated.

Comments

-

Why you claiming the RNRBs rather than the transferable NRB from your mother’s estate? Assuming this was available it would avoid you doing an IHT return if his estate falls below £650k.

Also what do you mean by “less than the taper relief’? Did he give away more than £325k?0 -

Thanks for your reply.

First, an apology the previous heading read IHT436 and it should have read IHT435.

In answer to your first question the estate is in total close to £800k (I am using round figures here) so there is IHT to pay. Much of that derives from my father's house which was sold in 2024 when he moved into care.

I am applying the following reliefs

Residential nil rate band for my father £175,000. Claimed under the downsizing allowance.

Transferrable residential nil rate band from my mother £100,00. She died in 2002 so could never have claimed the residential nil rate band as that was introduced in 2017. My reference to the taper relief was meant to convey that my mother's estate was less than the £2,000,000 and thus the residential exemption amount of £100,000 was not reduced.

The result of those reliefs the estate is reduced from £800k to £525k.

Apply the nil rate band of £325,000 and the estate is reduced to £200,000. My mother did use her full entitlement to the nil rate band in 2002 to leave money to my sister and I. So £80,000 IHT is due.

But when I reach page 4 of IHT435 it asks about other assets. Should I simply take the total of the estate and deduct the revenue from the sale of the house? The problem is that a significant amount of the proceeds of the house sale were used in payment of care fees.

Or do I simply total the other assets such as shares, Stocks and Shares ISA?

I hope that clarifies matters and any further help gratefully received.

0 -

Thanks for the clarification. First off you have made an error regarding the transferable RNRB, regardless of the date of death of the first spouse, if no RNRB was used at the time the full current allowance is claimable, so you don’t have as much IHT to pay as you thought.

Your question is an interesting one, this is straight forward where you are not claiming under the downsizing rule but less clear where that applies and the proceeds of the sale have been mixed up either all the other assets. I would take the total amount being left to direct descendants less the sale price of the house and use that figure.

0 -

Thank you for this comment.

I am confused by your first observation.

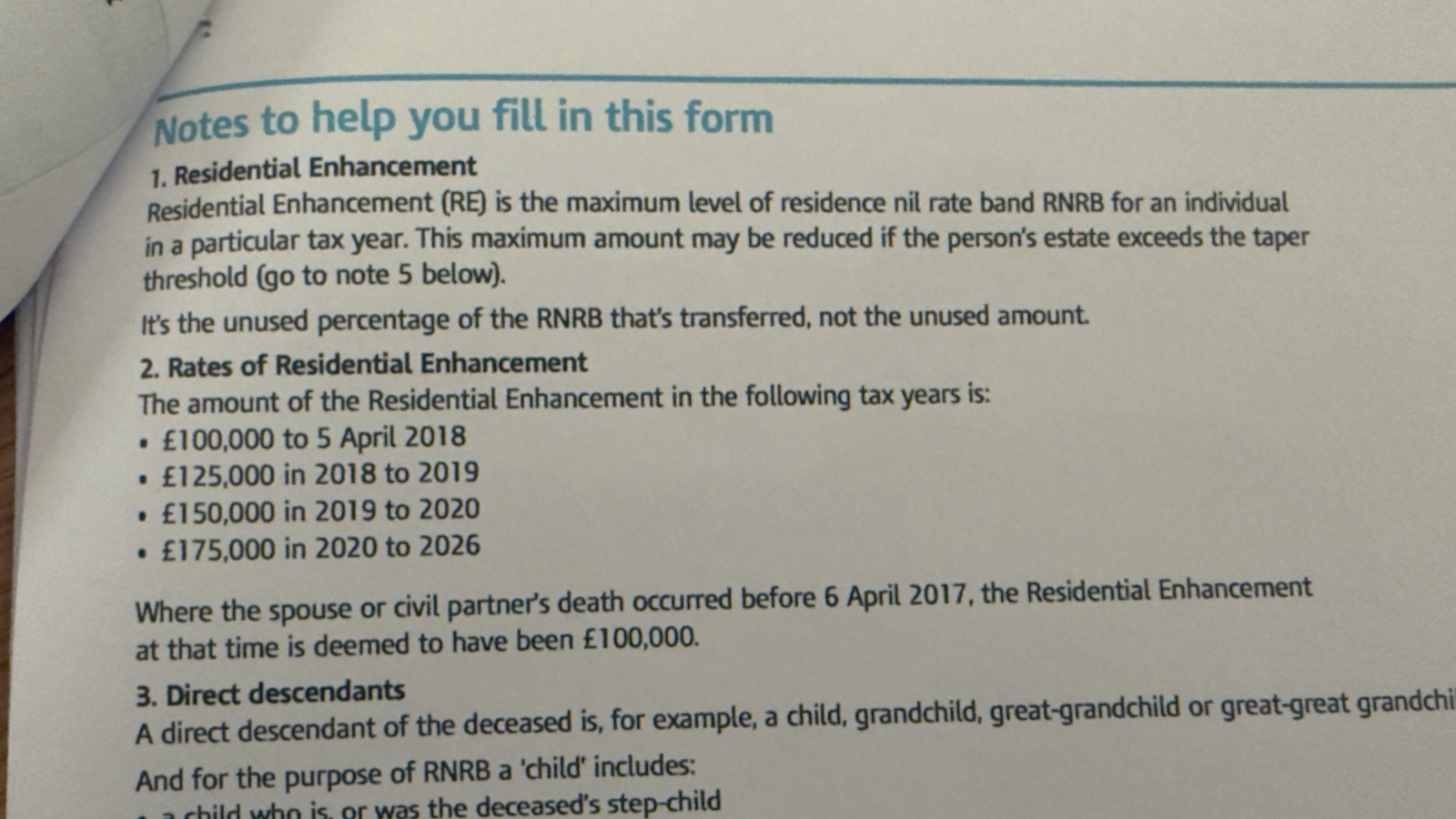

My reading of the notes to IHT436 (photo attached) leads me to conclude that since my mother died before 2017 the maximum residential enhancement which can be claimed is £100,000. I’m struggling to see how a higher transfer of the Residential Nil Rate Band could be claimed. Any further guidance much appreciated.

0

0 -

See paragraph 1 -

'It's the unused percentage of the RNRB that's transferred, not the unused amount'

#2 Saving for Christmas 2024 - £1 a day challenge. £325 of £3661 -

I understand the point in paragraph 1. In this case the unused percentage is 100%, so the next question is 100% of what?

And paragraph 2 (final sentence) says for a death occurring before 6 April 2017 (which is the case) the residential enhancement is deemed to be £100,000.

So I think I can claim 100% of that figure.Apologies if I am missing the point.

0 -

No it's 100% of the residence nil rate band prevailing at the date of the 2nd spouse death, subject of course to the property being worth at least £350k ( ie 2 x £175k) at that time.

0 -

@JGB1955 @poseidon1 @Keep_pedalling

Thank you all for your invaluable assistance. The penny finally dropped (rather a large number of pennies to be honest).

I think that I was being influenced by the voice of my late father who had drilled into me the notion that HMRC would always opt for the most restrictive approach they could get away with. So, I expected the transfer from Mum's RNRB to be deliberately restricted to a lower figure. The blame is, of course, all mine not my father's.

And just to confirm on @poseidon1's point that the property sold for well in excess of £350,000.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards