We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Holding off investing in fixed terms?

Comments

-

That sounds like nonsense to me. The gilt market moves independently of the Bank of England base rate and factors in a number of variables that differ from those considered by the MPC when setting rates.

I'd suggest someone trying to predict the future base rate from changes to gilt yields is not someone who should be listened to.

I'll also be very surprised if the base rate is 4.75% by the end of this year.

Mortgage rates have been rising this past week, so unless that turns out to be a temporary blip, it is likely fixed savings rates will do so too providing there is enough demand from borrowers for the higher cost loans.

2 -

Gilts Do follow BoE rates,

UK government bonds, or gilts, generally follow Bank of England (BoE) interest rates, with yields moving in tandem with expected rate changes. When the BoE raises rates to fight inflation, gilt yields typically rise (prices fall). Conversely, if rates are expected to fall, gilt yields usually decrease

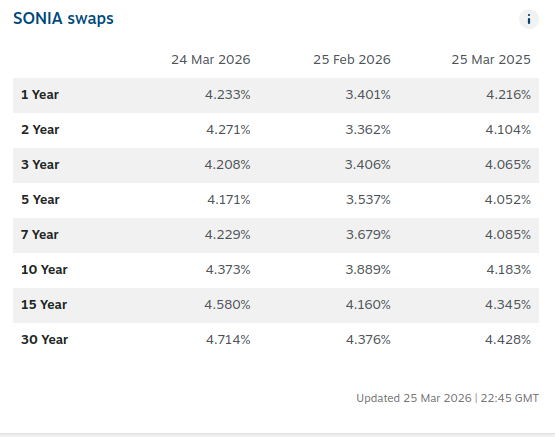

SONIA two year swaps already actually paying 4.5% and that is fact not a “guess”2 -

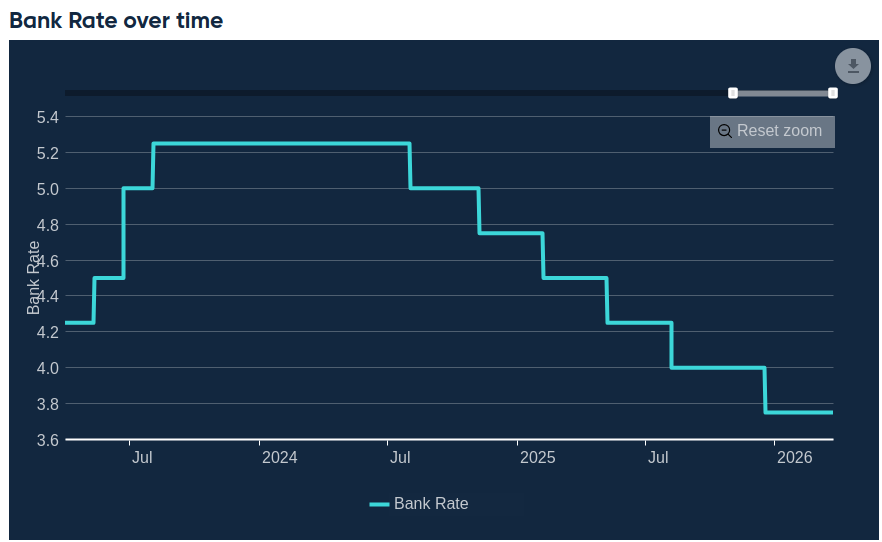

Yes, short-dated gilts do generally follow the base rate. Follow, not lead, and generally not fully. A lot of fluctuation is seen between MPC meetings, and the premium or discount on base rate also varies over longer time periods. The only mention of gilts in the article you linked refers to 10 year gilts, which are not short dated and do not follow or lead base rate. Over the last 3 years, it led the increases in base rate up to 5.25% through to 2023, but the base rate overshot the 10y gilt yield. Then the 10y gilt yield fluctuated a lot over the next period, while the base rate fell smoothly throughout. In October 2025, when the 10y gilt yield was 4.6%, at least 2 rate cuts were predicted in 2026. Then last Friday, when the 10y gilt yield was a little above 4.8%, Goldman Sachs came out predicting a flat base rate over the remainder of 2026. A day earlier, the MPC decided to hold the base rate steady. Today the 10y gilt yield is again a little above 4.8%, about the same as it was in January 2025.

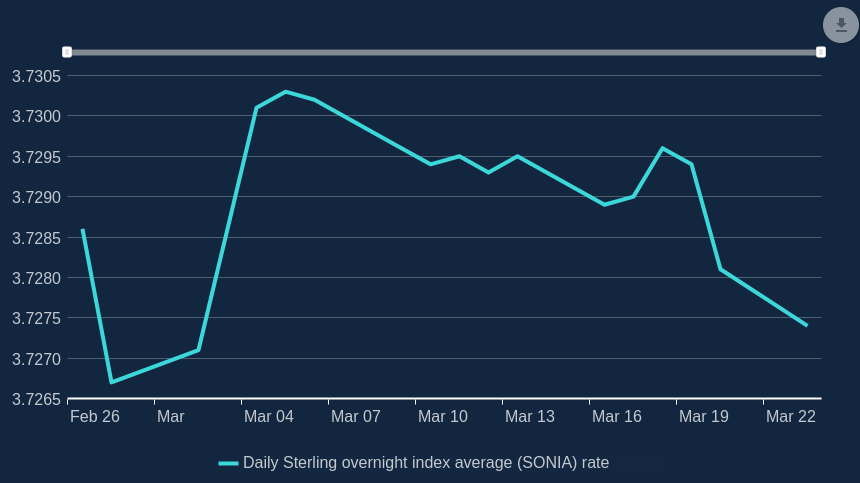

SONIA is the Sterling Overnight Index Average, is an interest rate benchmark, as it is based on actual inter-bank lending rates. This has been decreasing over the past few days:

A SONIA 2 year swap is precisely a "guess" on future rates, whereby one party bets on a fixed rate of interest being worth as much as the variable interest rate they would otherwise received on their cash. As of yesterday, the SONIA 2 year swap was paying 4.1% up from 3.4% last month, with the 1 year swap at 4.2%. This is suggestive of one 0.25% rate hike over the next year (as there is a duration risk premium that needs to be factored in as well), but could all change again before the next MPC meeting. Anyone who took the bet at the 4.5% you have quoted should be pleased with themselves today.

However, the expectation that the base rate or fixed term savings accounts should follow these knee-jerk movements in SONIA swap rates or the 10 year gilt yield will lead one to disappointment. If you wish to benefit from these volatile products then you'll need an investment account, not a savings account.

5 -

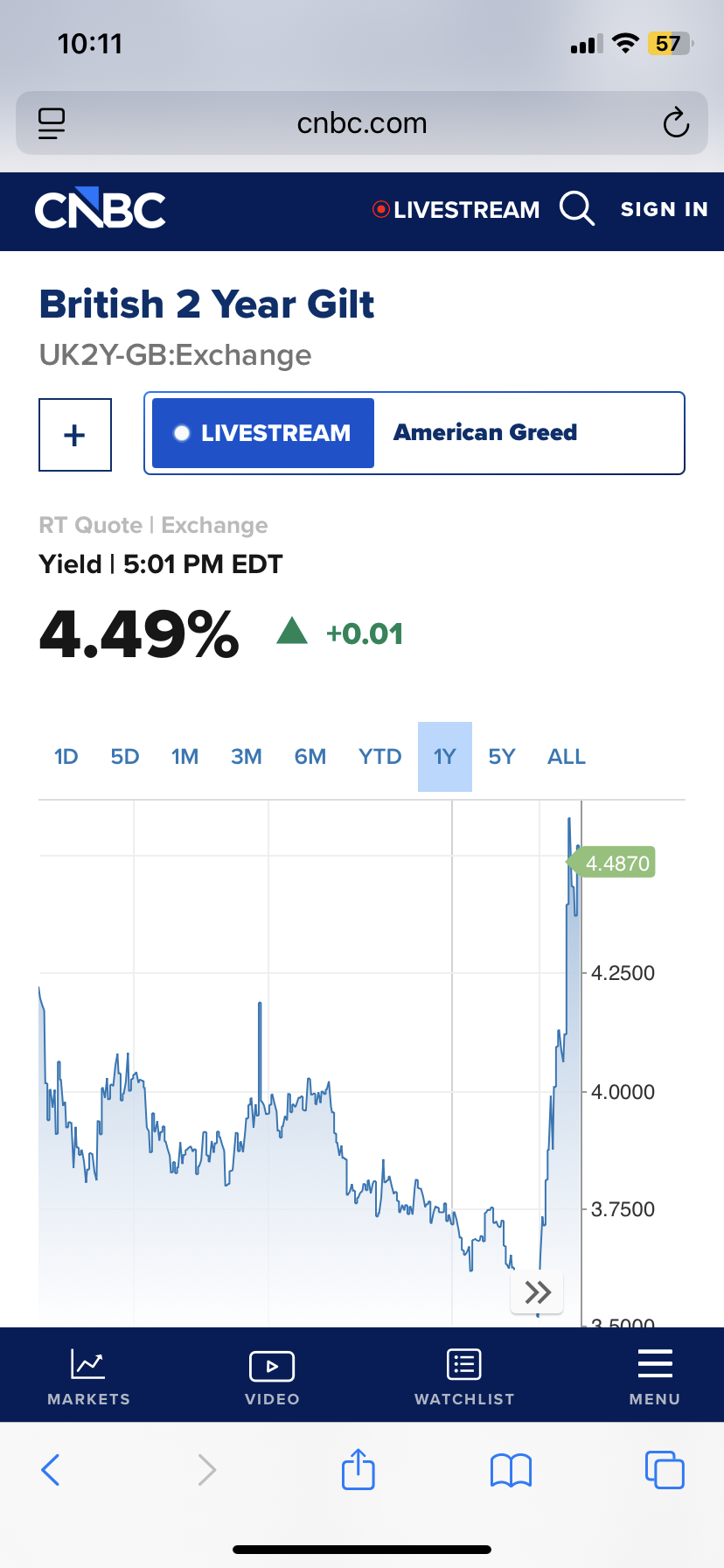

current 2 year guilt rates

1 -

TN28 is currently paying a YTM of 4.26%, only 0.14% of that counts as taxable interest.

TG29 is currently paying a YTM of 4.35%, only 0.56% of that counts as taxable interest.

Gilts (no "u") are looking very attractive to savers at the moment if held to maturity, like a fixed term would be. And very tax efficient if opting for the low coupon variety.

7 -

I don't really understand gilts. Are they like other fixed-interest securities - ie buy at a certain rate, get a fixed return for a while, then have to sell them at the current price (which may have gone down)?

0 -

You buy at a market price that locks in a fixed set of cashflows (YTM) if held to maturity. You don't have to sell them - they'll redeem at par (£100) on their maturity date, but you can sell them in advance of maturity for the market price at that time (which could be higher or lower than par). As they near maturity, they'll tend towards par (pull to par effect). Holding to maturity means you have certainty over the outcome, but it doesn't prevent you from exiting early if an opportunity presents itself or a need arises (unlike conventional fixed savings).

Currently many gilts trade below par, meaning you get a capital gain as part of the YTM. This capital gain is tax exempt.

9

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.7K Spending & Discounts

- 247.8K Work, Benefits & Business

- 604.8K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards