We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

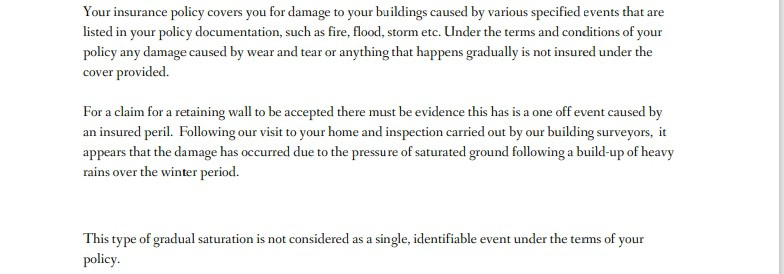

Buildings insurance repudiation letter - this is ambiguous isn't it..?

Our retaining garden wall crashed down in torrential rain during a named storm earlier this year. Just had the insurance company's repudiation letter via their Loss Adjusters - notice the 'appears that the damage has occurred...' line. Surely that's ambiguous and unclear? Worthwhile challenging?

Comments

-

You can certainly challenge it, but you would need evidence to support your challenge.

I guess your challenge could be one of the following…

- The damage was not caused by gradual saturation, it was caused by a one off event (e.g. a specific storm)

Or

- The damage was caused by subsidence (which might then be covered by your policy)

Or

- Damage was caused gradual saturation, but that is covered by your policy

You would probably need to employ a professional loss assessor to give their opinion on this. The insurers probably won't be swayed by your amateur opinion on this.

1 -

One off event will be argued, but it's the ambiguity 'appears' that bothers me - as if they're not absolutely sure.

"I'm ready for my close-up Mr. DeMille...."0 -

I dont think you could ever be absolutely sure....

0 -

One off event will be argued, but it's the ambiguity 'appears' that bothers me - as if they're not absolutely sure.

They don't need to be absolutely sure. The standard of proof in the event if a dispute is balance of probabilities, ie is it more likely than not to be caused by something that's covered by your policy?

1 -

There is no requirement for absolute certainty. Criminal law is based on "beyond reasonable doubt" so accepts some could have doubts and civil law, which covers insurance, is "on the balance of probabilities" which is a much lower standard but works because in most cases you have A -v- B and a judge has to pick a winner as otherwise most cases would end in a draw with neither side being able to prove with total certainty their version of events.

They dont have a way to see how the wall was before it collapsed. They can't say with absolute certainty exactly how much rain fell on that piece of land that day. They can't recreate the wall as it was and do A/B testing to see if it would have fallen with that amount of rain on dry soil or only, as they propose, if the ground was already sodden. They are correct in highlighting that its their experts judgement and not that they have managed to master time travel.

With an insured perils policy, which most Home insurance is, the default is that its not covered unless it can be proven the cause of the damage was one of the insured perils and that none of the exclusions applied. With higher grade policies they are written on an "all risks" basis which means the default is that all damage is covered and its up to the insurer to prove that one of the exclusions apply

1 -

Thanks for your input everyone.

I do think we're getting the brush-off early on as it's a pretty big claim and we're not happy at the insurance companies brief dismissal.

And the event was certainly sudden and during a named storm in a west coast location that was hit hard. The wall was in good condition prior, and we couldn't have known about possible saturated ground or a build up of water as nothing was visible.

We do have a lot of Met Office data - to the hour - on the day concerned.

Will be invoking Contra Preferentum - wish us luck! 😵💫

"I'm ready for my close-up Mr. DeMille...."0 -

Contra proferentem applies to contractual terms, which term do you think is ambiguous? Their investigation is not definitive but that isnt captured by the concept of contra proferentem.

Ultimately you have nothing to lose with a complaint and escalation to the ombudsman but you are better on focusing on what evidence you have that it was the event alone that caused it rather than the contract is ambiguous. A structural engineers report saying it would have fallen with the rain alone will carry much more weight than your latin. That said, the rain this year has not been biblical in nature and so the question will be raised why it fell this time and not previously which naturally points to time being a factor.

0 -

Contract gives storm condition parameters which we believe we can fulfill; as to CP, it can be applied to the company's repudiation of the claim because of the ambiguous 'appears' statement.

Sorry so brief - arthritic fingers.

"I'm ready for my close-up Mr. DeMille...."0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards