We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Should I Delay Buying Gilt Ladder

Comments

-

I take similar approach, gilts at 3+ years to redemption I would be inclined to default to ILGs, but probably nominal at shorter duration; you don’t know which is ‘better’ without hindsight knowledge- but I seek to mitigate the uncertainty over the longer timelines & I’m comfortable with that simple rationale. A solution doesn’t need to the best - just reasonable and workable

1 -

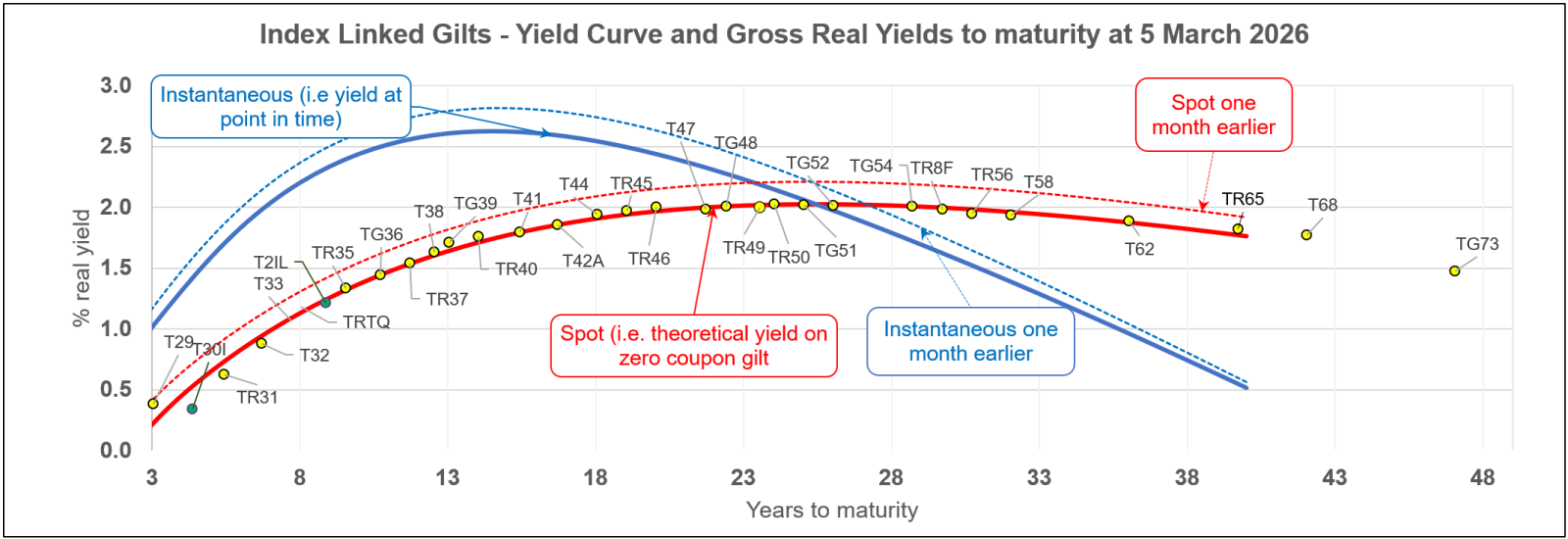

And this is the real yield curve as of the end of 5th March 2026 compared with a month ago. So showing how despite the recent increase in real yields since the Iran war, these real yields are still below the real yields from a month ago

Prices have subsequently fallen again (real yields increased) on 6th March so further slightly narrowing the gap from a month ago.

I came, I saw, I melted1 -

Whilst buying now may well be the right answer for OP, depending on his situation and attitude to risk, I would take issue with saying that delaying the purchase was necessarily market timing. OP is looking at money for between nine and fourteen years from now - well within a sensible time horizon for equity investing. There is a case to be made, particularly for the later years, for getting the money into the stock market and looking to move to gilts nearer the time.

OTOH I don't see any case to delay if you were just going to leave it in a money market fund.

0 -

This rather depends on how you define success and failure here though.......

0 -

I'm not understanding the blue line. I can't see any gilts in the 10-15 year range that return 2.5% real yield…?

0 -

I was intending to setup a 5 year index linked Gilt Ladder in the next couple of weeks with the first year maturing in 2035. The money is currently sitting in a Money market fund.

I have a couple of questions.

Qu’n 1: Seeing as you don’t need the money until 2035-2040 why is your money in a money market fund? With c.14 years to go surely you should have some exposure to equities or at the very least a fund with a higher risk and return profile compared to a money market fund?

Qu’n 2: If the last gilt doesn’t need to mature until 2039/2040 this seems to me to be an extremely risk averse approach to take. Your funds are outside of the equity market for c.14 years. Is there a reason why you are wishing to purchase the gilt ladder now but as others have said if your money is only in a money market fund (i.e. not equities) then you may as well.

In my opinion you seem to be extremely risk averse with your approach. Granted nobody knows what the future will hold but it just seems like you are missing out on a lot of potential growth due to potentially investing in the gilt fund now.

0 -

The spot yield curve is equivalent to the real yield on a theoretical zero coupon gilt of each term, which is why the real return on the actual index linked gilts shown on the chart are close to that line, as the coupon doesn't make that much difference compared to that theoretical non coupon paying index linked gilt.

The blue line is the instantaneous real yield curve, that is the real yield at a single point in time, or the limit of the real yield for the period around that duration as that period tends to zero. The instantaneous real yields are the building blocks for the spot real yields. For example the spot yield at duration 12 is a sort of (geometric) average of all the instantaneous real yields from duration 0 up to duration 12.

I came, I saw, I melted0 -

This may only be one part of the OP's financial plan and if so, it might be reasonable.

I have actually done something similar. I have set up an indexed gilt ladder with yearly maturity dates between 2031 and 2039. This locks in the real value with a little growth on top. But I also have equities as well.

I no longer need significant growth, so value retention is at least as important to me as growth, so I have some of each.

1 -

Your right this is part of a wider retirement strategy and there is plenty in equities too, the ladder is designed as bridge to state pension age.

I decided to take some money out of equities to guarantee the 5 years of state pension equivalent income. It might seem conservative 9 years out from needing it but the dot com crash took best part of 10 years to recover.so who knows.

The MMF was just intended as a temporary measure while I sort out the ladder but with the war kicking off and likely rising interest rates I was just wondering if it might be worth delaying.

1 -

Building an index linked gilt ladder now provides a known inflation adjusted income in the 5 year period from 2035.

Real equity returns over the next 14 years are unknown. As a guide, historically (1872 onwards), in 14 year rolling periods the UK stock market* has seen annualised returns ranging from -4.3% (1st percentile, i.e., worst case) to 0.1% (10th percentile) to 5.4% in the median case (for a more diverse 50/50 UK/US equity portfolio, the values were -2.1%, 0.9%, and 7.1%).

In other words, in roughly 10% of historical cases the equity performance, and hence income, would have been worse than the current real yield of the deferred ladder (about 1.1%). Whether this counts as 'extremely risk averse' will rather depend on personal circumstances (e.g., how important is that 5 year bridge to the SP to your retirement plans) and appetite for risk.

I'd agree that keeping the money in an MMF for that period would likely have a worse performance since 3 month UK treasury bills - a useful proxy for an MMF - over historical 14 year periods had annualised real returns of -5.2%, -2.8%, and 1.6% at the 1st, 10th, and 50th, i.e., median, percentiles. (edited to note that the MMF is a temporary measure)

* I've used return, cpi and exchange rate data from macrohistory.net

5

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards