We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

IHT409 and SIPP

My father died recently and I am completing form IHT400 as there will be some IHT due.

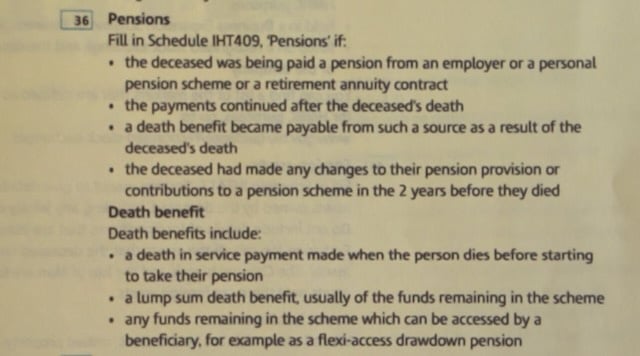

He had a SIPP with Norwich Union. My understanding is that SIPP's remain outside the scope IHT until next year. However, I also thought that HMRC liked to check that the SIPP qualified. When I read the guidance notes on IHT400 at page 15 (see picture below). The answer to all of the circumstances listed is "No". He was not drawing down money from the scheme nor making contributions or changes to it (He died of Alzheimer's in his late 80's). So my conclusion is that I do not need to include the SIPP on IHT409 and thus not on IHT400.

But I would welcome guidance from forum members on the topic.

Thanks in advance.

Comments

-

As long as your father had a beneficiary nomination form in place informing Norwich Union ( now Aviva I believe) of his choice of pension beneficiaries on death, then the Sipp value is outside his estate.

Have you ascertained with Aviva that a nomination does exsist and that they are likely to pay out in accordance with his wishes?

If there is no such nomination, then there is a risk they may opt to pay the pension funds into the estate, to be distributed in accordance with the terms of the will. That outcome would certainly bring the sipp into potential iht charge.

1 -

@poseidon1 Many thanks for your response.

Yes the quarterly valuation reports confirm that an expression of wish has been lodged nominating my sister and I as pension beneficiaries. I am currently waiting for the intermediary fund manager to complete their check on the identity of the beneficiaries. Once that is completed I assume they will confirm that they will pay out in accordance with his expression of wish. (The intermediary still refers to the fund as Norwich Union but the actual investment funds are all badged as Aviva - so you are correct).

One further point has occurred to me. Although my father was not "being paid a pension" (i.e. using regular drawdown) he did apparently drawdown a lump sum which used up the lifetime allowance at some point more than 8 years ago. Does that mean the answer to bullet question 1 on note 36 should actually be "yes".

Thanks

0 -

Just to clarify, despite the fact the Sipp is not an IHT assessable asset ( because of the clear beneficiary nomination in place) you are still required to complete IHT409 because the remaining 'death benefit' pension funds will be accessible to you and other nominated beneficiaries by way of 'flexi access drawdown pensions'. That is the final category under note 36 requiring IHT 409 submission.

That said, your father taking the TFC many years before death does not constitute him '..... being paid a pension from an employer(etc )...' . That question is asked in the present tense and infers a regular payment which was ongoing until his death.

0 -

Thank you again.

I had not sufficiently understood the relevance of the final category under note 36.

I thought that it must have to be reported because otherwise HMRC would have no way of checking that it met the criteria for being outside the scope of IHT. Specifically, the existence of a a valid expression of wish nomination.

And as an observation I do think the notes could be made clearer. And if I as the holder of a couple of undergraduate degrees and a Ph.D (in law!) struggled to understand it then I think others might struggle too. I also acknowledge that my specialism was not in tax law.

1 -

As I have mentioned on this forum in the past, HMRC's tax systems and practices ( especially with regard to IHT) were never designed to be either easily understood or navigated by ordinary members of the public.

The entirety of the legislative system stemming from the origins of death duty as it is now represented by Inheritance Tax, was devised to be understood by trained tax specialists acting on behalf of wealthy middle/upper class clients able to afford their expertise.

The fact that ordinary members of the public are permitted to undertake probate and inheritance tax compliance on an unaided DIY basis ( should they wish ), has not changed the lack of transparency and accessibility one would consider fair to expect of a system in which the untutored have been encouraged to engage.

The regime surrounding probate and IHT remains opaque, hedged with complex legislative anti avoidance provisions and peppered with the residue of archane case law and practices, which even the average non specialist solicitor would find challenging, let alone the layman.

2 -

Thank you for this I have just done my expression of wish online with my SIPP provider Did not realise it was outstanding

21k savings no debt0 -

After a few days break for a little sunshine I am back in the IHT torture chamber! Thank you @poseidon1 for your very succinct explanation of HMRC's approach.

I understand the need for anti avoidance measures and that some (many?) cases will be moderately complex. The case I am dealing with is actually very simple and only complicated by among things poorly designed forms (even the form preambles aren't consistent - some ask for Surname and First Name, other for Surname and First Names as the most basic example).

Some of the commentary on IHT400 is positively misleading. For example at box 43 (debts owed to the estate) it gives the very clear impression that only personal loans or mortgages are relevant - but the guidance note itself makes it clear that other debts are covered too. That's not complicated law it's just bad design.

Add bad design to complicated law and you have the recipe for a dog's breakfast (but not one I would give to my faithful companion!)

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards