We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

GPPP is it Workplace or Personal - limited to 3 cash-ins?

Comments

-

Hi Marcon,

Should have been clearer about my professional advice suggestion.

Yes the OP should gather ALL the information they can about all the different pensions before speaking to an advisor, as this will make things easier for all concerned and mean that the advisor has the minimum amount of work to do.

0 -

Hi DRS1,

Actually, a number of local Legal Practices offer free legal clinics in my hometown. I approached them initially because I considered the issue to be a legal one (and it may still end up that way), but they said they'd refer me to a local IFA they used for their clients and as they say the rest is history.

So some professionals do still practice in the "old" ways and only charge where they provide a distinct and valuable service.

Found out what i needed to and at no cost.

I was pleasantly surprised and would obviously use the IFA if I needed their services in the future (which may also happen with my pension problem) 😀.

0 -

Actually, a number of local Legal Practices offer free legal clinics in my hometown. I approached them initially because I considered the issue to be a legal one (and it may still end up that way), but they said they'd refer me to a local IFA they used for their clients and as they say the rest is history.

So some professionals do still practice in the "old" ways and only charge where they provide a distinct and valuable service.

Found out what i needed to and at no cost.

I was pleasantly surprised and would obviously use the IFA if I needed their services in the future (which may also happen with my pension problem)

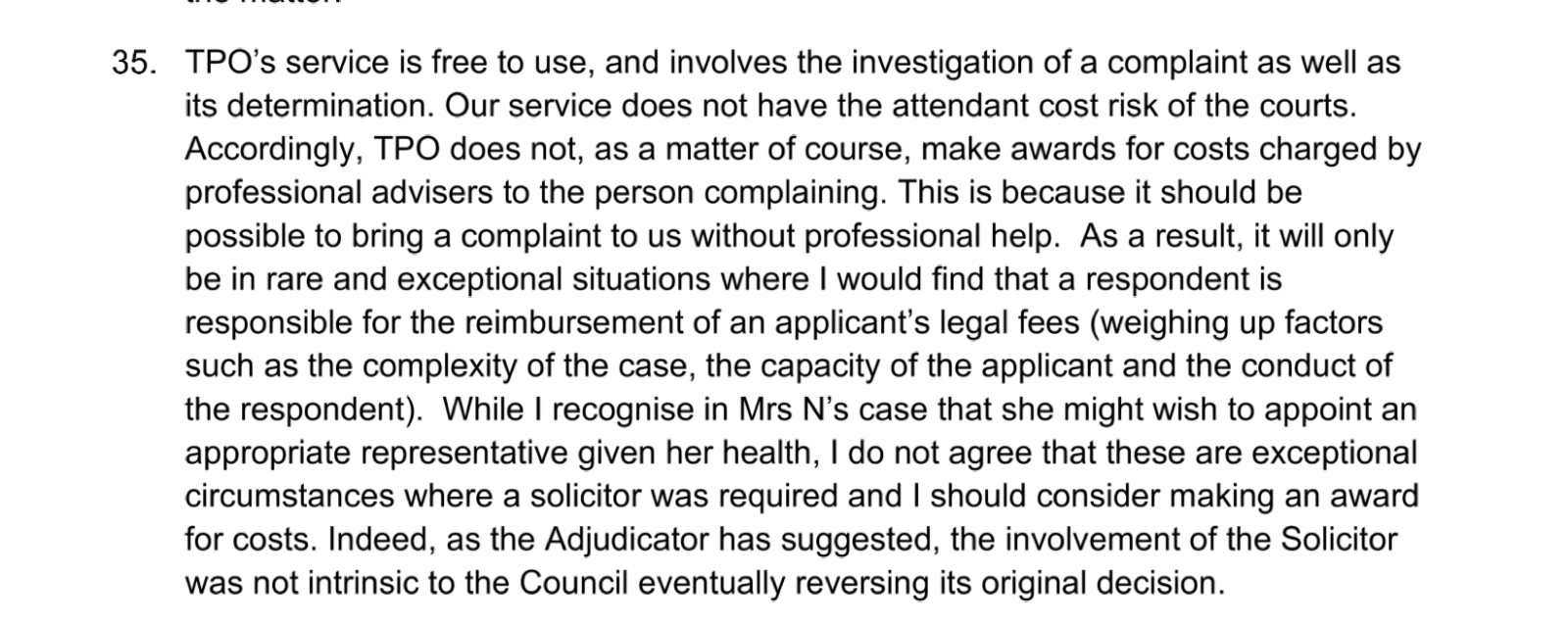

No need to pay for help - and you are unlikely in the extreme to get your costs back if you do, whatever the outcome of any complaint you might make about your 'issue', as the Pensions Ombudsman made particularly clear in a recent determination:

https://www.pensions-ombudsman.org.uk/sites/default/files/decisions/CAS-121348-Z6R0.pdf

Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0 -

If there is no immediate need for money, it's often possible to transfer old DC pensions into a current workplace pension. That would eliminate having so many small ones, and avoid having to choose funds (as she pprobably would in a SIPP), if not withdrawing all the cash.

If she consolidated the small bits into one SIPP, she could consider just taking the TFLS, if that would cover what is needed now, which would also not trigger the MPAA

0 -

she should also not be charged any fees for transferring the tiddlers into either an active workplace pension or a new SIPP

I’m a Senior Forum Ambassador and I support the Forum Team on the Pensions, Annuities & Retirement Planning, Loans

& Credit Cards boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com.

All views are my own and not the official line of MoneySavingExpert.0 -

My educated guess is that if the OP's friend approached an IFA about all these small pots, the reply would be something along the lines of 'very interesting but I am fully booked at the moment'

Most IFA's are quite busy, and are not usually interested in anything where less than £100K is involved. Even if they were, their fees would be excessive compared to the size of the funds ( and the work) being discussed in this thread.

1 -

My educated guess is that if the OP's friend approached an IFA about all these small pots, the reply would be something along the lines of 'very interesting but I am fully booked at the moment'

Especially this time of the year.

Most IFA's are quite busy, and are not usually interested in anything where less than £100K is involved. Even if they were, their fees would be excessive compared to the size of the funds ( and the work) being discussed in this thread.

A trainee or relatively new adviser who may have capacity may offer services but the fees relative to the size are going to be the issue if formal advice is given.

UFPLS and flexi-access drawdown are explicitly treated by the FCA as higher‑risk retirement income solutions that require robust risk profiling and explanations of the sustainability of withdrawals. The use of the small pots / trivial commutation rules is not, in itself, characterised in FCA material as a high‑risk product or strategy in the same way, although there are still important tax and planning risks to consider.

If it were someone with lots of money and an odd stranded pot or similar, it wouldn't be an issue. However, using multiple small pots in your 50s, whilst you have alternative pensions that may not be on track for the retirement period, is higher risk for the adviser as its not the pot itself but the scenario being advised on and it could require modelling and analysis and risk warnings to a higher level that introduces commercial risk for the adviser. Where commercial risk goes up, so does the fee.

Just as I feared, GPPP is a Personal Pension. I do wonder how employees are supposed to get a true workplace pension from their employer when so many employers opt to provide their legally obligated auto-enrolment workplace pension via a GPPP?

You misunderstand. GPPPs became available in 1988. The term "workplace pension" didnt exist then. Auto-enrolment wasnt a thing. These were effectively personal pension plans (the PPP part of GPPP) with some software that allowed them to be used by employers where a single payment would be made to the group and the provider would disperse to the individual plans.

It was mainly Final Salary Schemes, COMPs and CIMPs prior to that. GPPPs were introduced to allow smaller companies to offer a pension to their employees without the higher costs of the alternatives.

Auto-enrolment was introduced much later, and most GPPPs are not compliant with auto-enrolment rules. Many of those that did try to adapt to be compliant did so with software that is not on par with modern auto-enrolment schemes. This is why many of the providers no longer open GPPPs but instead have a modern Auto enrolment scheme instead. However, GPPPs in force can continue but the majority are paid up or on borrowed time until the employer moves to a modern version.

It's quite unusual nowadays to find an employer that is still using a legacy GPPP for auto-enrolment.

Workplace pensions are now dominated by master trust schemes. They didnt exist before AE.

A Pension Wise booklet even said something like "a workplace pension is one your employer set up. A personal pension you set up yourself" I'll have to find it and quote word for word.

You have to be careful about not being a pedant about certain words. And that comes from someone who is often a pedant about certain words.

Modern language use in financial services often involves dumbing down, leading to words that once meant one thing now being used for something else.

For anyone aged under 30, they probably have not experienced anything other than "workplace pension".

Sites, such as moneyhelper/pensionwise, cannot explan the differences of all the pension types as it would be far too long and people won't read it. The Martin Lewis style of explanation needs to be used. i.e. quick, simple to understand but know that it won't be 100% correct all of the time and won't cover nuances.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.2 -

Hi Marcon,

Agreed, but you have to get your complaint to the point where you can refer it to TPO and that takes a level of knowledge about the underlying issue and the best way to proceed, which I didn't have. So I could raise the complaint, get it wrong and TPO could rule on my complaint against me - not because I wasn't adversely affected, but because I raised the wrong complaint.

So clarifying the basis of the complaint and how to make it (and whether I needed any professional assistance) was the purpose of my enquiries with the solicitor and the IFA.

You don't know what you don't know…

0 -

This is why many of the providers no longer open GPPPs but instead have a modern Auto enrolment scheme instead. However, GPPPs in force can continue but the majority are paid up or on borrowed time until the employer moves to a modern version.

My last employer was a very large company and the pension was a GPPP scheme. It existed before auto enrolment I think.

As you know one of the advantages of these schemes is that you take them with you when you leave/retire. This has been good for me as the charges are very low, and I have full access and facility for UFPLS and drawdown if I need it. If the ex employer moves on to a different scheme, then hopefully this would not affect my pension? Maybe it would just convert to an actual personal pension( which it effectively is anyway) ? Hopefully with the same charges !

0 -

Agreed, but you have to get your complaint to the point where you can refer it to TPO and that takes a level of knowledge about the underlying issue and the best way to proceed, which I didn't have. So I could raise the complaint, get it wrong and TPO could rule on my complaint against me - not because I wasn't adversely affected, but because I raised the wrong complaint.

If that were true, it would make a mockery of the PO's statement that people don't need professional advice before taking a complaint to them.

Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards