We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Investing / Carry on regardless?

i started investing late - starting my sipp at 50, now at 51 having become comfortable and slightly more informed ive been happy to invest around 80k in HSBC global balanced fund. I realise the best thing is said to be just keep going but the high valuations, potential AI bubble and potential slow recovery with my age in mind have me thinking about if i should be looking at non US / tech related options or other types of investment.

Understanding that the future cant be predicted are other investers ignoring the noise or looking to make changes?

Comments

-

The fund you have is a well diversified multi-asset fund. Exactly the kind of fund for those of us who can't predict the future in fact. If you think you can call the changes better than anyone else by all means narrow down your options and try to beat the market, but I'd really recommend you don't use your pension for that, instead, if you must, keep it to a small fun portfolio while continuing to save into the core.

1 -

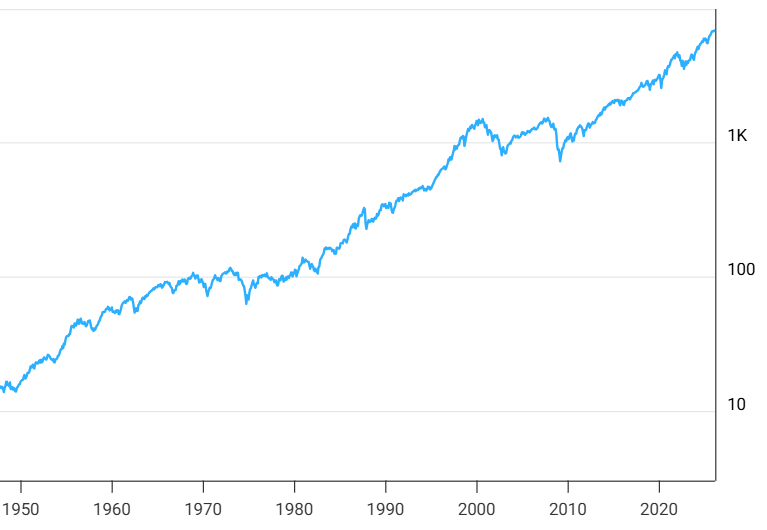

I often have similar concerns, but what gives me some perspective is the following chart:

The chart below shows the S&P 500 from 1950 to 2026, but in a logarithmic format which emphasises the annual percentage increase, not the absolute value, and as a result appears far less "peaky" than the usual charts you see most days.

Just take a look at the graph and cover the right hand side so that it stops at any past date, and ask youself, would you have invested then, because in about 80% of the past 76 years, the same was true and the market looked to be "at an all time high", or within a few percent of it.

• The rich buy assets.

• The rich buy assets.

• The poor only have expenses.

• The middle class buy liabilities they think are assets.0 -

thanks, no i dont, im just curious if more experienced investors weigh up not the every day stuff but if theres an accumulation of signals that might point to an issue with a sector or country - the high valuations and AI issues in this case - or wether whatever happens you carry on regardless

0 -

If you are tracking a highly diversified global index, then it takes care of a lot of the sector shifts for you. As indexes generally contain the best performing companies at that moment in time, if companies or sectors perform poorly, they fall out of the index and are replaced with ones which are on the rise.

A quick AI query gives the following:

Key Historical Sector Shifts:

- Information Technology (1990s–Present): Rose from 6.3% in 1990 to over 34% by March 2000, and is the dominant sector in the 2020s, often comprising >30% of the index.

- Industrials (1960s–1970s): Held a massive 33% weighting in 1969.

- Energy (1980s–2000s): ExxonMobil was consistently a top-ranked company from 1985–2005.

- Financials (Mid-2000s): Reached 22.35% of the index by September 2006 before the 2008 financial crisis.

- Consumer Staples (Pre-1980s): Long-time giants included tobacco and beverage companies.

• The rich buy assets.

• The poor only have expenses.

• The middle class buy liabilities they think are assets.1 -

Problem is by the time you recognise a 'signal' it will have already been acted on by someone else first waiting to make money from people who are late to the game. So I'd leave calls like that to the traders, and instead stick to a well diversified global fund which will take care of things like sector or geographical rotations for you without needing intervention from you.

2 -

The key words are "highly diversified". Blindly using a global index does not guarantee diversification. In the past year the MSCI EM index provided twice the returns of the MSCI World index which has no EM holdings. So choose your index with some care.

3 -

In the long term if you are investing in broad funds rather than cherry picked individual companies I dont believe you can gain from interpreting transient signals in the market. In the short/medium term it is best to carry on regardless. .Feeling that you need to continue tweaking a large portfolio wastes time and could be very stressful.

However this does make it important that your portfolio is well diversified so that if one area falls another is available to take its place. No particular area (country, industry, etc) should be so predominant such that a failure there could lead to a failure to meet your objectives.

Although short term market movements should be ignored, over the long term changes in the world economy may lead you to alter your diversification strategy - eg the changes as EM countries do actually emerge as major powers.

3 -

There have been some regular posters on here, who have eased back on the % equity and % US in their portfolios, thinking that the stock market rises in the last few years just can not go on for ever. Mostly these investors have been in relatively high risk 100% equity index funds, which have done extremely well.

However you are only in a medium risk fund, so you would not want to be over cautious, which is a risk in itself.

You could look at Vanguard Life strategy 60, which is a bit less US and a bit more UK orientated.

You mention that you are 51. Remember that you will not be withdrawing the whole pension on the day you retire and it may well have to last many decades. Only if you are planning to buy an annuity in the next 10 years, should you be really thinking about reducing your investment risk.

2 -

There have been some regular posters on here, who have eased back on the % equity and % US in their portfolios, thinking that the stock market rises in the last few years just can not go on for ever. Mostly these investors have been in relatively high risk 100% equity index funds, which have done extremely well.

We tilted away from the US last year mainly because index investing was increasing in risk due to the big gains in the US. Market cap for the US has almost doubled since 2013, creating concentration in a market dominated by tech.

That has led to market-cap tracking being the place to be for the last 12-13 years. However, we know from history that these things cycle and that the US will go out of favour at some point. It's still too early to say, but with the US being lagging most of the regions/major countries in 2025 for those operating in Sterling, we could be in that next cycle already.

That doesn't mean passive investing will not be the place to be, but rather a case of tilting your passives away from the US and not blindly following market cap.

If US foreign and trade policy becomes more internationally collaborative, the dollar strengthens, and AI turns out to be another industrial revolution, then tilting away from the US would probably not be a good move. However, tilt means just that. It doesn't mean a wholesale swing away, leaving very little.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.10 -

@InvesterJones but when the sector (tech ) is so dominant it sort of feels inevitable that theres going to be a large adjustment. It took me a long time to get on board with investing but it feels like it could be a good time to pause - im still adding 1k to my sipp but i have a lump sum i want to drip feed into it. Just feels like a bad time to do that or at least that I should look at if the fund im investing in is the right one now

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.2K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.8K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards