We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

State Pension taxable

Comments

-

Quoting the marginal rate also makes it sound as if people are paying more tax than they are - it's a valid and useful data point when looking at the incentives to earn an extra £1, but for overall tax and NI paid, someone on £30k would be paying about £3300 tax and £1400 NI which is under 16% of their salary. The employee pension contributions are just semi-enforced savings and still belong to the person paying them ( plus the tax relief bonus)

2 -

But they are all costs of employment, and most or all will passed through into wages. That is the centre of the discussion about the decision increase to employer NI and whether it will reduce employment, wage growth, or both.

Ultimately, a sum of money is required from the employer to employ an individual, and some of that money ends up in the employee's bank account. In between, various deductions are taken. It doesn't really matter where those deductions are taken from or whether they are before or after tax, the responsibility of the individual or the employer, etc, there is a cost to employment for the employer, and a benefit from employment for the individual. The difference between the two is the deduction imposed through regulation.

If you only look at employee deductions, then there is an implicit assumption that raising employer NICs or statutory employer pension contributions do not have an effect on employee pay levels, which is not correct. Hence my point that all deductions imposed by legislation should be considered, regardless of which entity they fall upon. That shows how much is being taken from the amount the employer has to part with to employ the individual, and how much the individual actually receives.

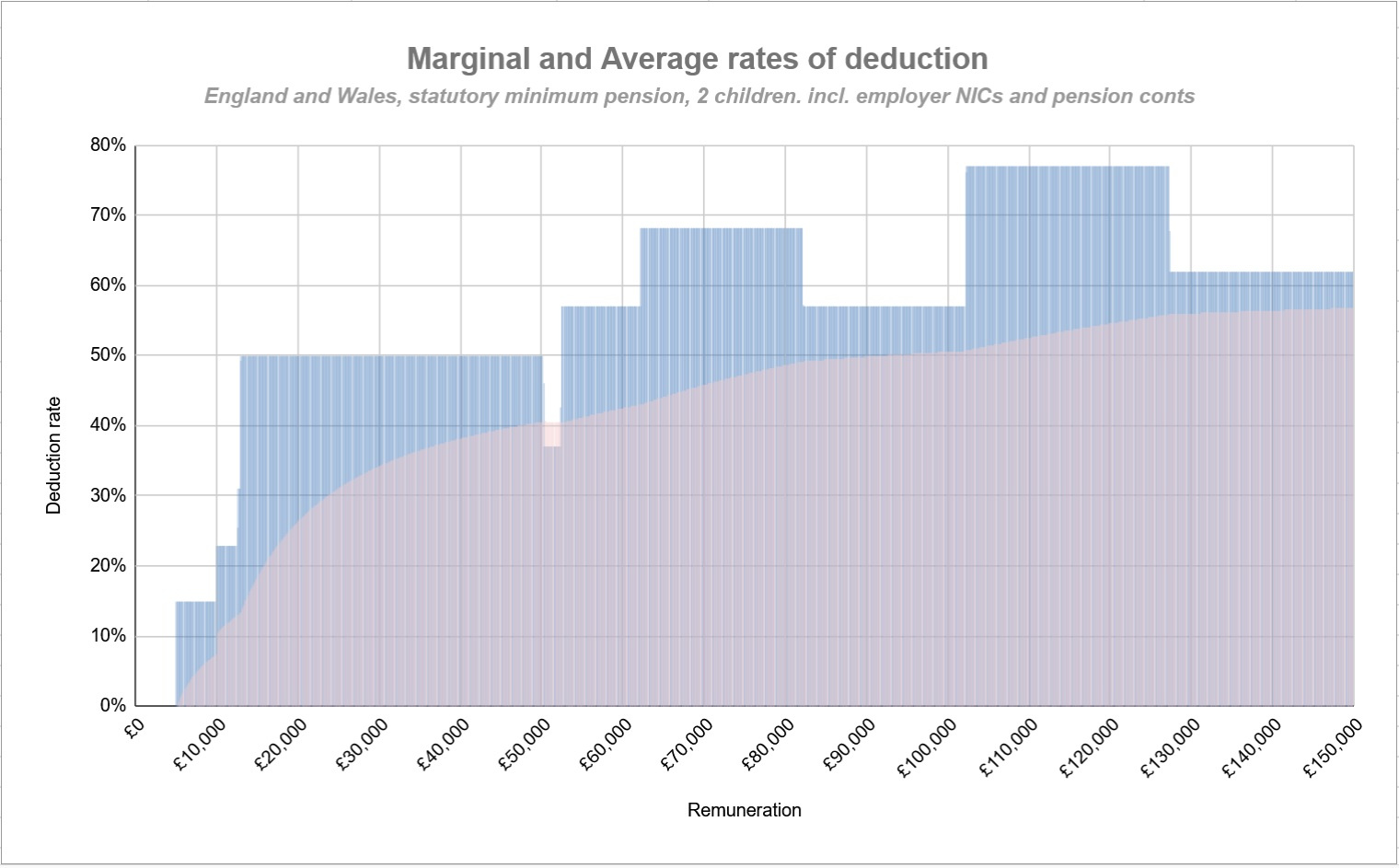

The chart is from a spreadsheet I have that can be parameterised for various scenarios. That particular one was for a student loan and 2 children, not all have loans, not all have children, and some have more children. Assumptions on these are necessary to produce the chart to take into account things that affect the deduction rate. Here is a chart without Student Loan repayments, it just moves the deduction rates downwards. It is instructive however, as you see how impactful the 9% repayment is when it is in addition to already very significant employment-related deductions. It also demonstrates the power of salary sacrifice, as it removes all the deductions and replaces them with only a 25% tax free and 75% taxable benefit for future years, with no employee NI, no employer NI, no Child Benefit reduction, nor Student Loan.

1

1 -

Their employer would also be paying about £3,750 in employer NI. There is an accounting justification to exclude that from the average deduction rate, but is there an economic justification?

0 -

If the government abolished employers NI tomorrow, some employers might hire more staff, but none would give their employees a pay rise. Salaries are set by market forces. Only if the stimulus created a shortage of suitable staff would employers be forced to offer higher salaries to attract employees.

0 -

Looking back to SnowMan's post re. the Treasury Select Committee, there's (still) nothing in Cerys McDonald's quoted replies to say that state pensioners won't be required to pay tax, just that they won't receive a tax bill after the end of the year.

N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Kirk Hill Co-op member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

2.72kWp PV facing SSW installed Jan 2012. 11 x 247w panels, 3.6kw inverter. 35 MWh generated, long-term average 2.6 Os.0 -

Which begs the question - if HMRC don't ask, how will they get (the tax)

0 -

It's always possible DWP will deduct it, like an employer or pension payer would.

They already do it for pre 6 April 2016 State Pension deferrals so it's not entirely a new concept to them.

1 -

If you want to include that in the "tax taken" amount, you'd also need to include it in the "total earned" amount that you're dividing by.

But although it's part of the cost of employing someone, so are office space, IT provision, admin overheads like HR, management costs, etc, and nobody's arguing that those are part of individuals' remuneration. For me, when talking about taxation rates on individuals, employer NI isn't part of the calculation.

(That doesn't mean that it doesn't have an indirect effect on the money available for pay.)

0 -

If you want to include that in the "tax taken" amount, you'd also need to include it in the "total earned" amount that you're dividing by.

The charts do that, the x axis is labelled remuneration, and is the total cash allocation for the employee from the employer. From that, all deductions (including employer NI) is taken to produce the net figure the individual receives.

But although it's part of the cost of employing someone, so are office space, IT provision, admin overheads like HR, management costs, etc, and nobody's arguing that those are part of individuals' remuneration. For me, when talking about taxation rates on individuals, employer NI isn't part of the calculation.

Those are costs of employment, but they are not statutory deductions dictated by legislation.

The correct measure to consider will depend upon the purpose. For individual incentives, employer NI is irrelevant unless the employer returns part or all of the saving within salary sacrifice pension contributions.

I find it interesting to explore the total statutory deductions that apply between the employer's bank account and the employee's bank account. They really are rather high, and it is interesting to see how policies on employer NI, Student Loan parameters, Child Benefit taper etc, come together.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards